概要

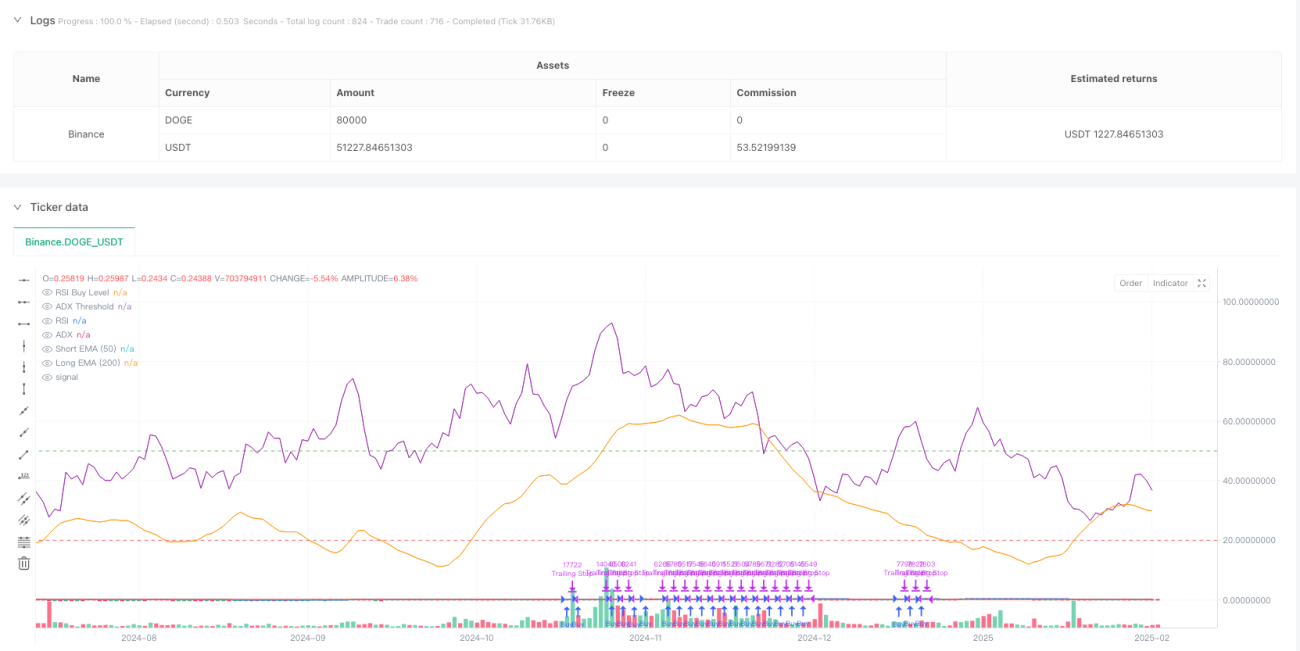

本戦略は、複数の移動平均線、モメンタム指標、動的リスク管理を組み合わせたトレンドフォローシステムです。価格トレンド、市場モメンタム、ボラティリティを分析して取引機会を特定し、厳格なポジション管理とストップロス機構でリスクを制御します。中核ロジックは、長期・短期の指数移動平均線(EMA)のクロスと相対力指数(RSI)の併用に基づき、平均真実レンジ(ATR)を用いてストップロス位置を動的に調整します。

戦略原理

本戦略は、取引シグナルを確認するための多層検証メカニズムを採用します。

- トレンド確認:50日と200日の2本の指数移動平均線を用いて中長期トレンドを判断し、短期線が長期線を10期間以上上回っていることを要求します。

- モメンタム検証:RSI指標で価格モメンタムを確認し、RSIが設定閾値(デフォルト50)を超えた場合に上昇モメンタムを確定します。

- トレンド強度:平均方向性指数(ADX)を導入してトレンド強度を測定し、ADXが20を超えると有意なトレンドとみなします。

- 動的リスク管理:ATRに基づき動的ストップロスを設計し、ストップロス距離はATRの2.5倍とし、トレーリングストップロス機構も組み込みます。

- スマートポジション管理:口座残高と事前設定リスク比率に応じて、ATRと組み合わせて動的に建玉数量を計算します。

戦略の利点

- 複数シグナル検証:移動平均線、モメンタム、トレンド強度など複数の次元で検証することで、シグナルの信頼性を高めます。

- 動的リスク管理:ボラティリティに基づく動的ストップロスとトレーリングストップロスを採用し、市場状況に適応します。

- スマートポジション管理:口座規模と市場ボラティリティに応じてポジションを動的に調整し、1取引あたりのリスクを効果的に制御します。

- トレンド持続性要件:トレンド継続期間の要件を設定することで、偽のブレイクアウトを回避します。

- システム化取引通知:取引シグナル通知機能を統合し、リアルタイム操作を容易にします。

戦略のリスク

- トレンド反転リスク:強いトレンド終了時に大きなドローダウンが発生する可能性があり、マクロ市場環境を考慮した調整が推奨されます。

- レンジ相場でのパフォーマンス:横ばいのレンジ相場では頻繁な取引が発生し、取引コストが増加する可能性があります。

- パラメータ感応度:複数の指標パラメータの設定が戦略パフォーマンスに影響するため、バックテストによる最適化が必要です。

- スリッページの影響:流動性が低い市場では大きなスリッページに直面する可能性があり、戦略収益に影響を与えます。

戦略の最適化方向性

- 市場環境への適応:ボラティリティ指標(例:VIX)を導入して戦略パラメータを動的に調整し、異なる市場環境での適応性を高めます。

- シグナルフィルタリング:出来高指標を追加して検証し、シグナル品質を向上させることを検討します。

- 利益確定メカニズム:価格変動に基づく動的利確メカニズムを設計し、収益対ドローダウン比率を最適化します。

- 時間枠最適化:異なる時間枠でシグナルの一貫性を検証し、取引安定性を向上させることを検討します。

- 機械学習による最適化:機械学習アルゴリズムを導入してパラメータを動的最適化し、戦略の適応性を高めます。

まとめ

本戦略は、複数のテクニカル指標を総合的に活用することで、完全なトレンドフォロー取引システムを構築しています。リスク管理面で優れており、動的ストップロスとポジション管理によりドローダウンを効果的に抑制します。拡張性が高く、複数の最適化方向性が用意されています。実運用時には、具体的な市場特性や自身のリスク選好に応じてパラメータを調整することを推奨します。

Overview

This strategy is a trend following system that combines multiple moving averages, momentum indicators, and dynamic risk control. It identifies trading opportunities by analyzing price trends, market momentum, and volatility while implementing strict position management and stop-loss mechanisms. The core logic revolves around the crossover of long and short-term exponential moving averages (EMA) combined with the Relative Strength Index (RSI), using Average True Range (ATR) for dynamic stop-loss positioning.

Strategy Principles

The strategy employs a multi-layer verification mechanism to confirm trading signals:

- Trend Confirmation: Uses 50-day and 200-day EMAs to judge medium and long-term trends, requiring the short-term average to remain above the long-term average for more than 10 periods.

- Momentum Verification: Uses RSI to verify price momentum, confirming upward momentum when RSI exceeds the set threshold (default 50).

- Trend Strength: Incorporates Average Directional Index (ADX) to measure trend strength, with ADX above 20 indicating significant trend.

- Dynamic Risk Control: Designs dynamic stop-loss based on ATR, with stop-loss distance set at 2.5 times ATR, including trailing stop mechanism.

- Intelligent Position Management: Dynamically calculates position size based on account equity and preset risk ratio in combination with ATR.

Strategy Advantages

- Multiple Signal Verification: Improves signal reliability through validation across multiple dimensions including moving averages, momentum, and trend strength.

- Dynamic Risk Management: Employs volatility-based dynamic and trailing stops that adapt to market conditions.

- Intelligent Position Control: Dynamically adjusts positions based on account size and market volatility, effectively controlling single trade risk.

- Trend Persistence Requirement: Avoids false breakouts by setting trend duration requirements.

- Systematic Trading Alerts: Integrates trading signal notifications for real-time operation.

Strategy Risks

- Trend Reversal Risk: May experience significant drawdowns at trend endings, suggesting adjustment based on macro market conditions.

- Sideways Market Performance: May generate frequent trades in range-bound markets, increasing transaction costs.

- Parameter Sensitivity: Strategy performance affected by multiple indicator parameters, requiring backtest optimization.

- Slippage Impact: May face significant slippage in low liquidity conditions, affecting strategy returns.

最適化の方向性

- 市場環境への適応:ボラティリティ指標(VIXなど)を導入し、動的にパラメータを調整することで、異なる市場環境への適応性を向上させることを検討する。

- シグナルフィルタリング:出来高指標による検証を追加し、シグナルの質を高めることを検討する。

- 利確メカニズム:市場のボラティリティに基づく動的な利確メカニズムを設計し、リターン対ドローダウン比率を最適化する。

- 時間枠の最適化:異なる時間枠でのシグナルの一貫性を検証し、トレーディングの安定性を向上させることを検討する。

- 機械学習による最適化:機械学習アルゴリズムを導入し、動的にパラメータを最適化することで、戦略の適応性を高めることを検討する。

まとめ

本戦略は、複数のテクニカル指標を総合的に活用することで、完全なトレンドフォロー型トレーディングシステムを構築している。動的なストップロスとポジション管理により、リスク管理において優れたパフォーマンスを示す。また、複数の最適化の方向性を残しており、拡張性が高い。トレーダーは、実際の取引で実装する際には、特定の市場特性と自身のリスク選好に応じてパラメータを調整することを推奨する。

- 1