RSIとストキャスティックRSIに基づくダブルモメンタムトレンドリバーサル戦略

2

Follow

502

Followers

概要

これは、相対力指数(RSI)と確率的相対力指数(Stochastic RSI)を組み合わせたトレンド反転取引戦略です。本戦略は、市場の買われ過ぎ・売られ過ぎの状態やモメンタムの変化を識別することで、潜在的な反転ポイントを捉え、取引を行います。核となる考え方は、RSI指標を基本的なモメンタム指標とし、その上でStochastic RSIを計算して価格モメンタムの変化方向をさらに確認することです。

戦略の原理

戦略の主なロジックは、以下の重要なステップで構成されています。

- まず、終値のRSI値を計算し、全体的な買われ過ぎ・売られ過ぎの状態を判断します。

- RSI値を基に、Stochastic RSIの%K線と%D線を計算します。

- RSIが売られ過ぎ領域(デフォルトでは30未満)にあり、かつStochastic RSIの%K線が下から上に%D線をクロスした場合に、買いシグナルが発生します。

- RSIが買われ過ぎ領域(デフォルトでは70超)にあり、かつStochastic RSIの%K線が上から下に%D線をクロスした場合に、売りシグナルが発生します。

- 逆のRSI条件が発生した場合、またはStochastic RSIが逆方向にクロスした場合に、ポジションをクローズします。

戦略の利点

- 二重確認メカニズム – RSIとStochastic RSIの組み合わせにより、偽のブレイクアウトのリスクを効果的に低減できます。

- カスタマイズ可能なパラメータ – RSI期間や買われ過ぎ・売られ過ぎの閾値など、主要なパラメータは様々な市場状況に応じて調整可能です。

- 動的可視化 – RSIとStochastic RSIのリアルタイムチャート表示を提供し、トレーダーが監視しやすくなっています。

- リスク管理の統合 – 完全なストップロスおよび利益確定メカニズムが含まれています。

- 適応性の高さ – 異なる時間足や市場環境に適用できます。

戦略のリスク

- レンジ相場リスク – 横ばいのレンジ相場では、頻繁な偽シグナルが発生する可能性があります。

- 遅延リスク – 複数の移動平均平滑化を使用するため、シグナルにある程度の遅れが生じる可能性があります。

- パラメータ感応度 – パラメータ設定の違いにより、取引結果が大きく異なる可能性があります。

- 市場環境依存 – 強いトレンド相場では、一部の値動きを取り逃す可能性があります。

- 資金管理リスク – リスクを管理するために、適切なポジションサイズを設定する必要があります。

戦略の最適化方向性

- トレンドフィルターの追加 – 長期移動平均線をトレンドフィルターとして追加し、トレンド方向にのみポジションを持つことが考えられます。

- ストップロスメカニズムの最適化 – トレーリングストップやATRストップなどの動的ストップロスを導入できます。

- 出来高指標の導入 – 出来高分析と組み合わせることで、シグナルの信頼性を高めることができます。

- 時間フィルターの追加 – 重要なニュース発表時間や流動性の低い時間帯を避けることができます。

- 適応型パラメータの開発 – 市場のボラティリティに応じて、戦略パラメータを自動調整します。

まとめ

本戦略は、モメンタムとトレンド反転を組み合わせた総合戦略であり、RSIとStochastic RSIの相乗効果により潜在的な取引機会を識別します。戦略の設計は合理的であり、調整可能性と適応性に優れています。ただし、実際の適用にあたっては市場環境の選択とリスク管理に注意が必要であり、実取引に使用する前に十分なバックテストとパラメータ最適化を行うことを推奨します。

Source

Pine

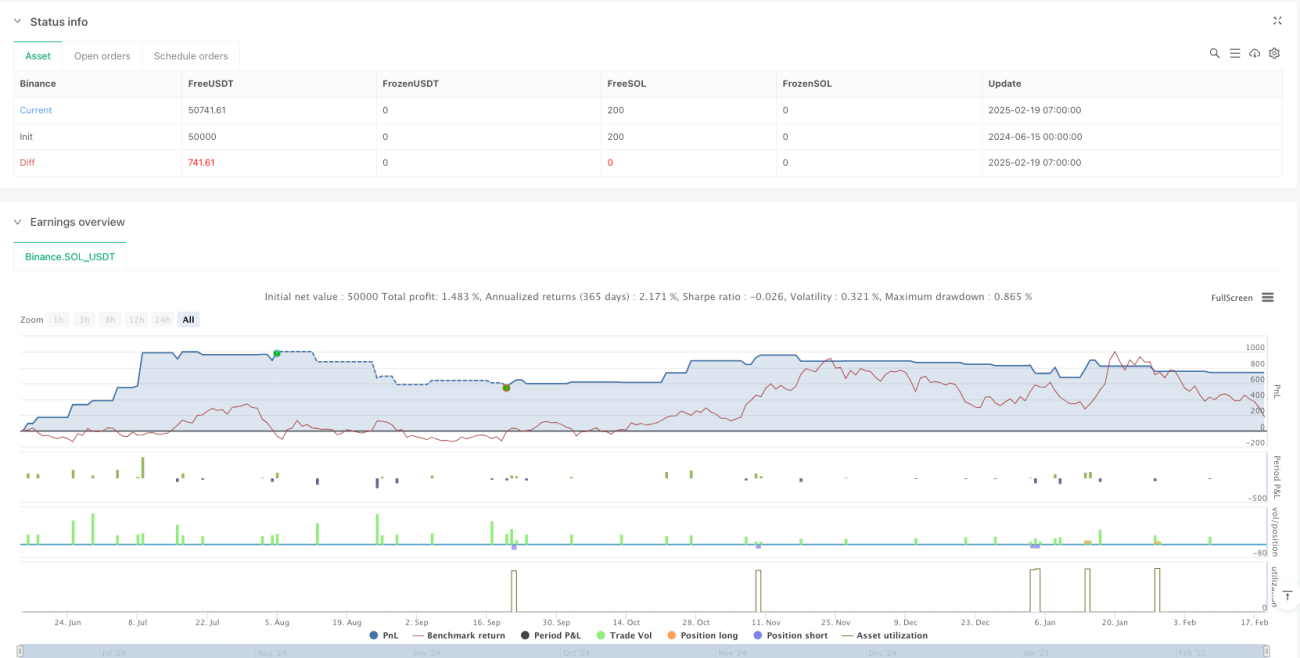

/*backtest

start: 2024-06-15 00:00:00

end: 2025-02-19 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("RSI + Stochastic RSI Strategy", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// INPUTSStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1