2

Follow

502

Followers

概要

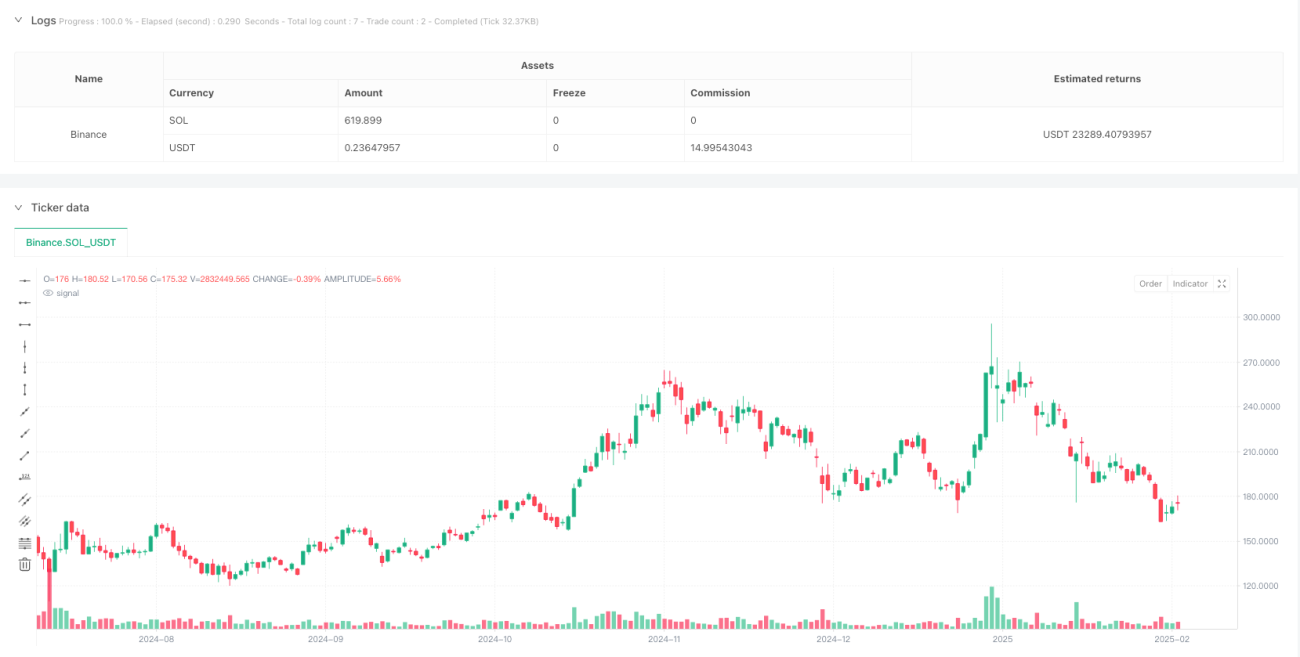

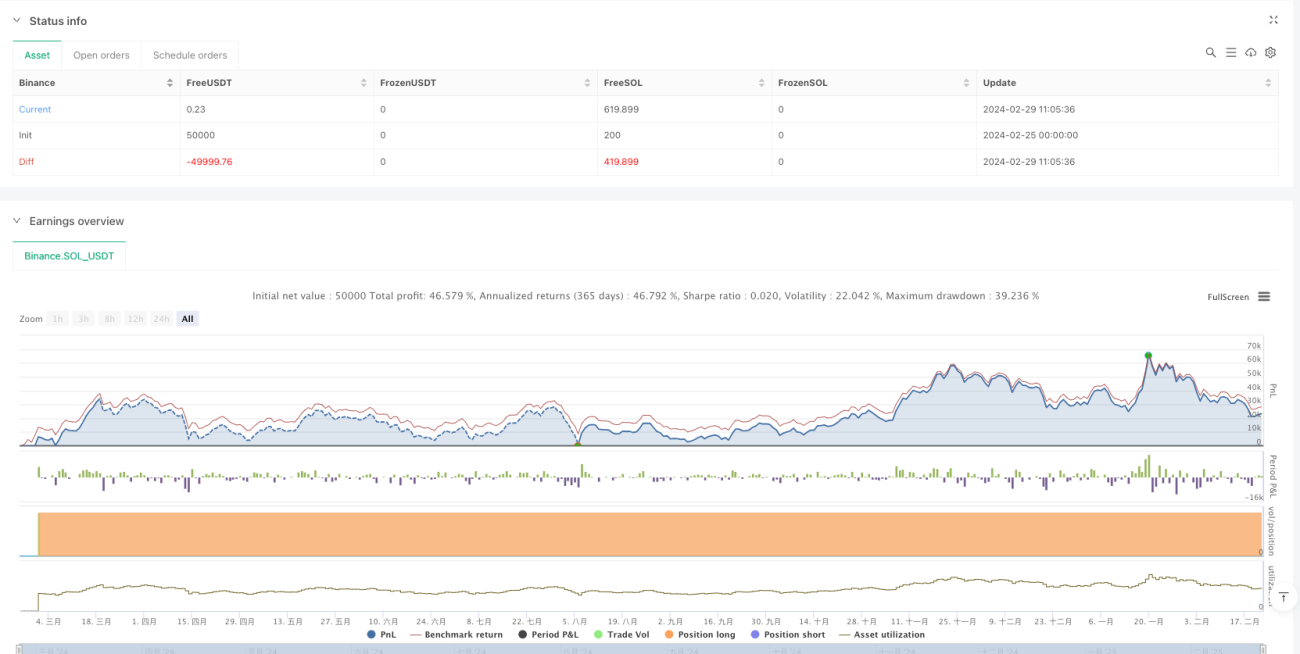

本戦略はモメンタムベースの取引システムであり、主にバランス・オブ・パワー(Balance of Power)指標を4時間足で使用して取引を行います。買い手と売り手の勢力比較を測定し、指標が設定した閾値を超えたときに取引シグナルを発生させます。本戦略は動的なポジション管理、調整可能なレバレッジ、視覚的な取引追跡機能などを備えており、市場のトレンド転換点を効果的に捉えることができます。

戦略の原理

戦略の核は、(終値-始値)/(高値-安値)を計算して市場の売買勢力バランスを測定することです。この値が1に近い場合は強い買いのモメンタムを示し、-1に近い場合は強い売りのプレッシャーを示します。具体的な取引ロジックは以下の通りです。

- エントリー条件:バランス・オブ・パワー指標が0.8を上抜けたとき、買い手の勢力が強く上昇トレンドと判断してロングエントリー

- エグジット条件:バランス・オブ・パワー指標が-0.8を下抜けたとき、売り手のプレッシャーが増大したとしてポジションをクローズ

- ポジション管理:口座残高に基づいて動的に調整し、レバレッジ倍率を設定可能

戦略の優位性

- シグナルが明確:固定閾値によるトリガーで、頻繁な取引を避け、確信度の高いシグナルに集中

- リスク管理が可能:動的なポジションサイズと調整可能なレバレッジにより柔軟なリスク管理を実現

- 可視性が高い:取引マークや履歴を提供し、バックテストや最適化が容易

- 適応性が良好:ボラティリティの高い市場環境に適しており、トレンド転換を迅速に捉えられる

戦略のリスク

- スリッページリスク:急激な変動時に大きなスリッページが発生する可能性

- フェイクブレイクアウトのリスク:偽のブレイクアウトシグナルが発生し損失につながる可能性

- トレンド依存:レンジ相場ではパフォーマンスが低下する可能性

- レバレッジリスク:過度なレバレッジは深刻な損失をもたらす可能性

戦略の最適化方向

- トレンドフィルターの導入:他のテクニカル指標と組み合わせて大勢のトレンド方向を判断

- 閾値設定の最適化:市場環境に応じて閾値を動的に調整

- ストップロス機構の強化:トレーリングストップなどのリスク管理手段を追加

- 時間フィルターの追加:重要な経済指標の発表など時間的要因を考慮

まとめ

本戦略はバランス・オブ・パワー指標を用いて市場のモメンタム変化を捉え、動的なポジション管理とリスク管理を組み合わせることで、比較的完成度の高い取引システムを構築しています。一定のリスクは存在しますが、継続的な最適化と改善により、戦略の安定性と収益性をさらに高めることができます。モメンタム取引に興味のあるトレーダーの使用と研究に適しています。

Source

Pine

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy(title="Balance of Power for US30 4H", format=format.price, precision=2, default_qty_type=strategy.percent_of_equity, default_qty_value=100, overlay=true, commission_value=0.01, max_labels_count=500, max_lines_count = 500)

leverage = input.float(5, "Leverage 1:", tooltip="Multiply your equity (100%) times the leverage.")Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1