RSIモメンタム指標に基づく適応型取引戦略

2

Follow

502

Followers

概要

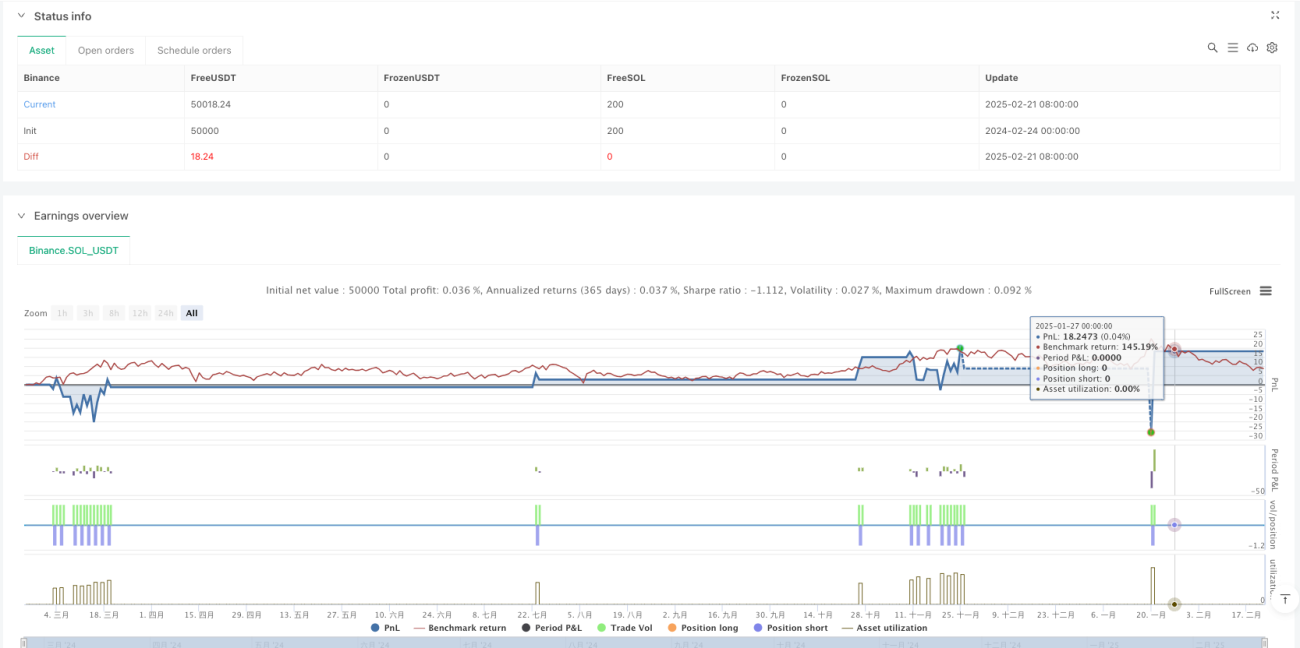

本戦略は、相対力指数(RSI)に基づくモメンタム取引システムであり、市場の買われ過ぎ・売られ過ぎ状態を識別して取引を行います。戦略は固定パーセンテージのストップロスと利確目標を採用し、リスク・リターンの自動管理を実現します。システムは15分足で動作し、流動性の高い取引銘柄に適しています。

戦略の原理

戦略の核はRSI指標を用いて市場の買われ過ぎ・売られ過ぎ状態を識別することです。RSIが30を下回ると市場が売られ過ぎの可能性があると判断し、ロングポジションを建てます。RSIが70を超えると買われ過ぎの可能性があると判断し、ショートポジションを建てます。各取引には、エントリー価格に基づく固定パーセンテージのストップロス(0.2%)と利確目標(0.6%)が設定され、リスク管理の自動化を図ります。

戦略の優位性

- 操作ルールが明確:広く認知されたRSI指標を使用し、取引シグナルが明確で、理解・実行が容易

- リスク管理が充実:固定比率のストップロスと利確設定により、各取引のリスクを効果的にコントロール

- 自動化の程度が高い:エントリーからエグジットまでの取引プロセス全体が自動化され、人的介入を低減

- 適応性が高い:異なる取引銘柄にも適用可能で、汎用性に優れる

- 計算効率が高い:基本的なテクニカル指標を使用するため、計算負荷が小さく、リアルタイム取引に適している

戦略のリスク

- レンジ相場のリスク:横ばいのレンジ相場では、頻繁に誤ったシグナルが発生する可能性がある

- トレンド突破リスク:固定ストップロスが強いトレンドの中で容易にヒットされる可能性がある

- パラメータ感応度:RSIの期間と閾値の設定が戦略のパフォーマンスに大きく影響する

- スリッページリスク:市場の変動が大きい場合、実際の約定価格が想定から乖離する可能性がある

- システミックリスク:市場が急激に変動する場合、大きな損失を被る可能性がある

戦略の最適化方向

- トレンドフィルターの導入:移動平均線などのトレンド指標を組み合わせ、誤シグナルを低減

- 動的ストップロス設定:市場のボラティリティに応じてストップロス幅を自動調整

- エントリータイミングの最適化:出来高などの補助指標を追加し、エントリー精度を向上

- 資金管理の最適化:動的なポジション管理を導入し、口座残高と市場変動に応じて取引規模を調整

- 時間フィルターの追加:重要な経済指標発表など高ボラティリティ時間帯の取引を回避

まとめ

本戦略は、構造がしっかりしており、論理的に明確な自動取引システムです。RSI指標により市場の買われ過ぎ・売られ過ぎの機会を捉え、固定比率のリスク管理手法と組み合わせることで、取引プロセスの完全自動化を実現しています。主な利点は操作ルールの明確さとリスクのコントロール性にありますが、市場環境が戦略のパフォーマンスに与える影響にも注意が必要です。提案された最適化方向により、戦略にはさらなる改善の余地があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1