セッションVWMAに基づく日内合成オプション戦略:ロング・ショートシグナル適応型トレーディングシステム

2

Follow

502

Followers

概要

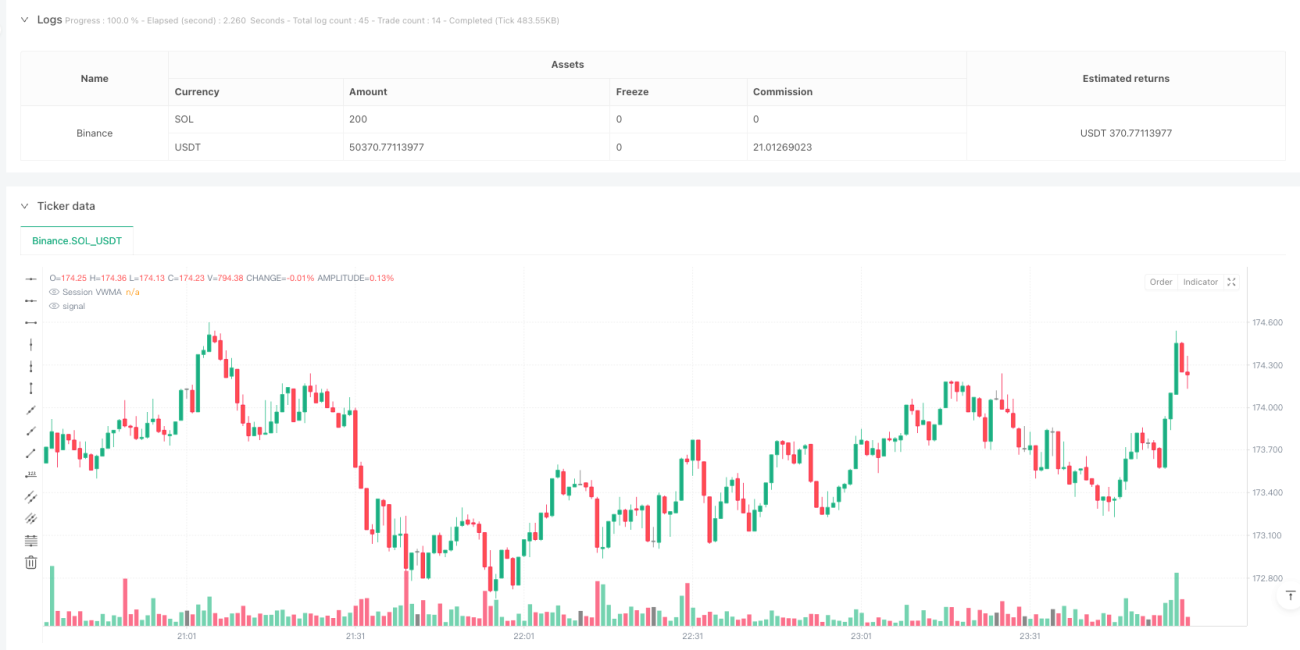

これは出来高加重移動平均線(VWMA)に基づくデイトレード戦略であり、合成オプション・コンビネーションを用いてロングとショートの両方向の取引を実現します。戦略の核は、各取引日に再計算されるVWMA指標であり、価格とVWMAの相対位置に応じて取引シグナルを生成し、取引終了前に自動的に全ポジションを決済します。本戦略はポジション管理や取引頻度制限など、優れたリスク管理メカニズムを備えています。

戦略の原理

戦略の核となるロジックは以下の通りです:

- 毎日リセットされるVWMAを動的なトレンド指標として使用

- 価格がVWMAを上抜けた場合、強気コンビネーション(コール買い+プット売り)を構築

- 価格がVWMAを下抜けた場合、弱気コンビネーション(プット買い+コール売り)を構築

- 15:29(IST)に全ポジションを強制決済

- hasExited変数を導入して追加ポジションの頻度を制御し、過剰な取引を防止

- 同一方向のブレイクアウト時にはピラミッディング方式での追加ポジションをサポート

戦略の利点

- 動的適応性が高い – VWMAを毎日リセットすることで、指標が常に現在の市場状況を反映

- リスクとリターンのバランス – 合成オプション・コンビネーションによりリスクを抑制しつつ、利益の可能性を維持

- 厳格な取引規律 – 明確なエントリー、追加ポジション、強制決済のメカニズム

- ポジションサイジングが柔軟 – パーセンテージによるポジション管理が可能

- 操作ロジックが明確 – シグナル発生条件はシンプルで直感的

戦略のリスク

- レンジ相場リスク – 横ばい市場でのVWMAブレイクアウトにより、頻繁な擬似シグナルが発生する可能性

- ギャップリスク – 翌営業日の大きな価格変動により大きな損失が発生する可能性

- オプション・コンビネーションのリスク – 合成オプションにはデルタ・ニュートラルの偏りが存在

- 執行スリッページ – 高頻度取引では大きなスリッページに直面する可能性

- 資金効率 – 毎日の強制決済により取引コストが増加

戦略の最適化方向性

- ボラティリティ・フィルターを導入し、高ボラティリティ環境下で戦略パラメータを調整

- トレンド確認指標を追加し、擬似ブレイクアウトによる損失を軽減

- オプション・コンビネーション構造の最適化(例:垂直スプレッド戦略の検討)

- 適応型VWMA期間の実装により、市場状態に応じた動的調整

- 最大ドローダウン制限など、より多くのリスク管理指標の追加

まとめ

これは構造が整っており、ロジックが緻密なデイトレード戦略です。VWMA指標で短期トレンドを捉え、合成オプション・コンビネーションを用いて取引を行い、優れたリスク管理メカニズムを備えています。戦略の最適化余地としては、擬似シグナルの削減、執行効率の向上、リスク管理体系の充実が挙げられます。一定の制約はあるものの、全体として実践的な価値のある取引システムです。

Source

Pine

/*backtest

start: 2025-02-16 00:00:00

end: 2025-02-23 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Session VWMA Synthetic Options Strategy", overlay=true, initial_capital=100000,

default_qty_type=strategy.percent_of_equity, default_qty_value=10, pyramiding=10, calc_on_every_tick=true)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1