2

Follow

502

Followers

概要

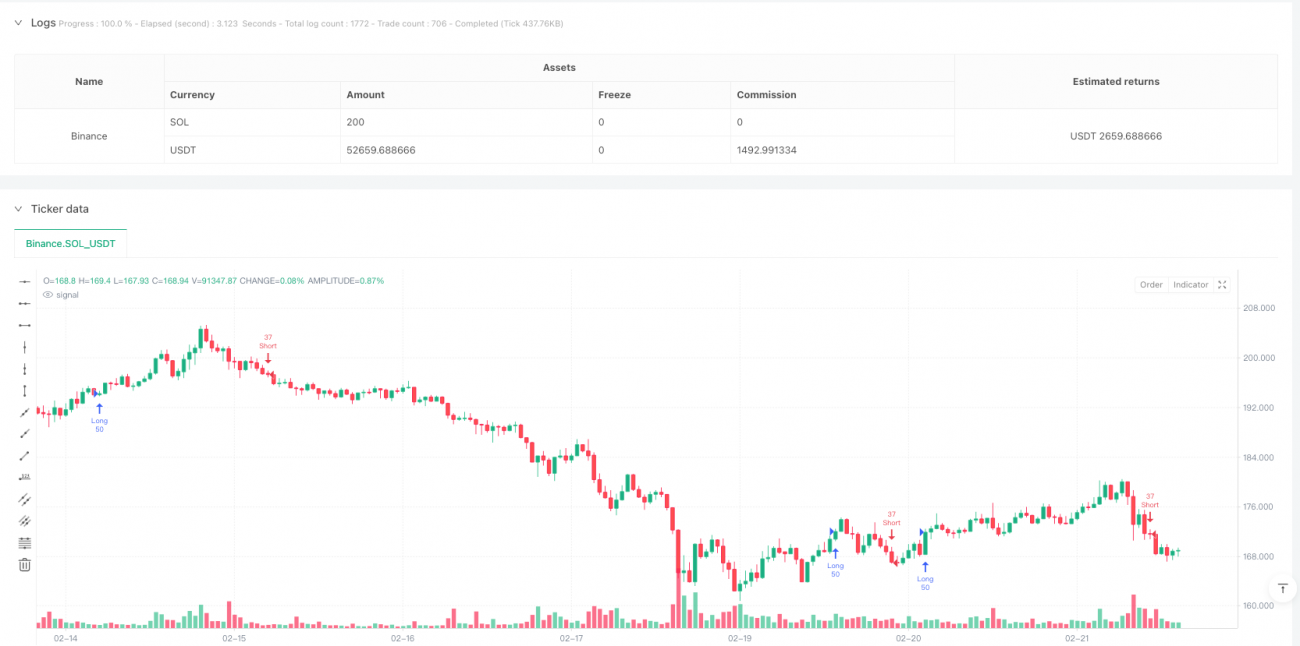

これはナスダック100ミニ先物向けに設計されたデイトレード戦略です。戦略の核は、二重移動平均線システムと出来高加重平均価格(VWAP)をトレンド確認に用い、真の変動幅(ATR)で損切り位置を動的に調整することです。この戦略は資金の安全性を保ちながら、厳格なリスク管理と動的なポジション管理により市場トレンドを捉えます。

戦略の原理

戦略は主に以下の核となる要素に基づいています:

- シグナルシステムは、9期間と21期間の指数移動平均線(EMA)のクロスを使用してトレンド方向を識別します。短期移動平均線が長期移動平均線を上抜けたときにロングシグナル、下抜けたときにショートシグナルが発生します。

- VWAPをトレンド確認指標として使用し、価格がVWAPを上回っている場合にのみロング、下回っている場合にのみショートのエントリーを行います。

- リスク管理システムはATRベースの動的ストップロスを使用し、ロングのストップロスはATRの2倍、ショートは1.5倍に設定します。

- 利益目標は非対称設計で、ロングはリスクリワード比3:1、ショートは2:1とします。

- トレーリングストップと損益分岐点ストップの仕組みを導入し、価格が目標利益の50%に達した時点でストップロスをコストラインに引き上げます。

戦略の利点

- 動的適応性が高い - ATRを用いてストップロスやトレーリングストップのパラメータを調整するため、様々な市場変動環境に自動適応できます。

- リスク管理が充実 - 1トレードあたりのリスクを1500ドル以内に制限し、週間最大損失2500ドルの上限を設定しています。

- 非対称な収益設計 - 市場特性を考慮し、ロングとショートで異なるリスクリワード比とポジションサイズを採用し、実市場により適合しています。

- 多重確認メカニズム - EMAクロスとVWAP確認を組み合わせることで、偽のブレイクアウトシグナルを効果的に低減します。

- 完全なストップロス体系 - 固定ストップロス、トレーリングストップ、損益分岐点ストップの三重の保護を備えています。

戦略のリスク

- レンジ相場のリスク - 横ばいのレンジ相場では、移動平均線のクロスシグナルが多くの偽シグナルを生む可能性があります。

- スリッページリスク - 急激な相場変動時には、約定価格がシグナル価格と大きく乖離する可能性があります。

- システムリスク - 重大なイベント発生時にはストップロスが機能しない可能性があります。

- 過剰取引リスク - 頻繁なシグナルにより取引コストが増加する可能性があります。

- 資金管理リスク - 初期資金が少ない場合、完全なポジション管理計画を有効に実行できない可能性があります。

戦略の最適化方向

- 出来高フィルターの導入 - 出来高確認メカニズムを追加し、出来高が条件を満たした場合のみ取引を実行します。

- 時間フィルターの最適化 - 具体的な取引時間枠を設け、変動の大きい寄り付きや引けの時間帯を避けます。

- パラメータの動的調整 - 市場環境に応じて移動平均線の期間やATR倍率を自動調整します。

- 市場心理指標の追加 - VIXなどのボラティリティ指標を導入し、取引頻度やポジションサイズを調整します。

- トレーリングストップの改善 - より柔軟なトレーリングストップアルゴリズムを設計し、トレンド捕捉能力を向上させます。

まとめ

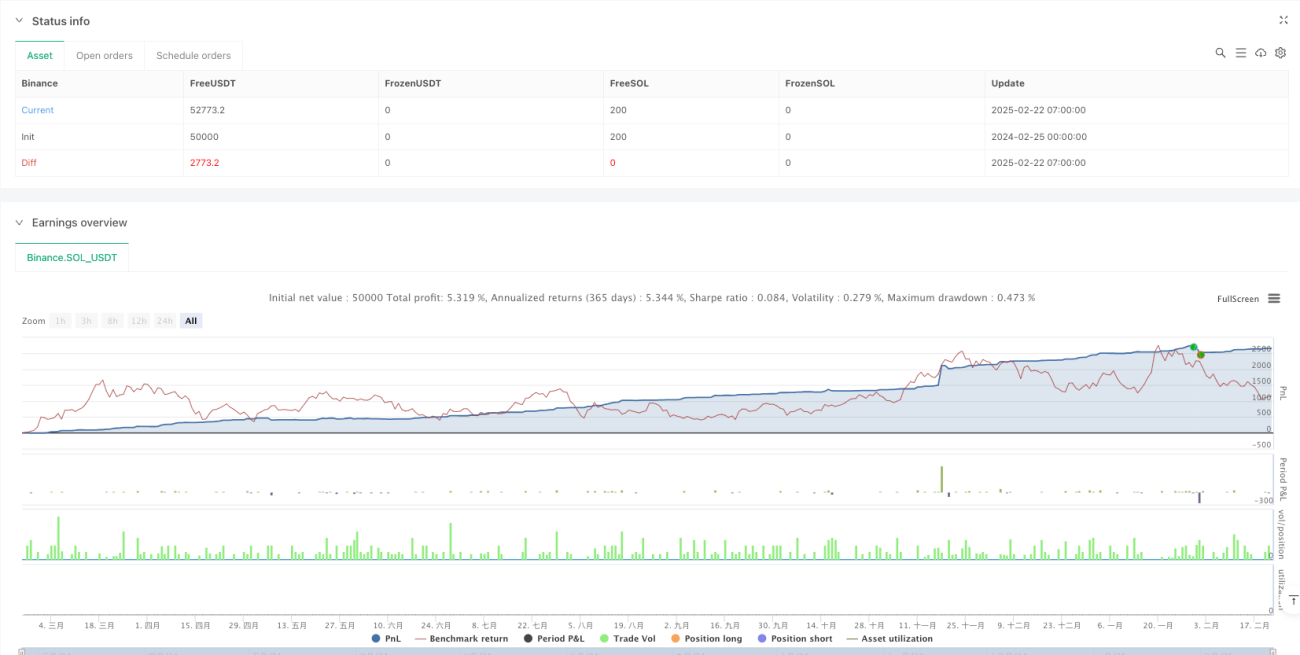

本戦略は、移動平均線システムとVWAPの組み合わせにより堅牢なトレンドフォローシステムを構築し、多層的なリスク管理メカニズムで資金の安全性を確保します。戦略の最大の特徴は適応性とリスク管理能力であり、ATRを用いて各種パラメータを動的に調整することで、様々な市場環境で安定したパフォーマンスを発揮できます。本戦略はナスダック100ミニ先物のデイトレードに特に適していますが、トレーダーはリスク管理ルールを厳守し、市場の変化に応じて適宜パラメータを調整する必要があります。

Source

Pine

/*backtest

start: 2024-02-25 00:00:00

end: 2025-02-22 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("Nasdaq 100 Micro - Optimized Risk Management", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// === INPUTS ===Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1