概要

マルチ指標加重スマート取引戦略は、複数のテクニカル指標からのシグナルを統合し、それぞれに異なる重みを割り当てて取引判断を生成する総合的な定量取引システムです。この戦略は、MACD、ストキャスティックRSI、EMA、スーパートレンド、移動平均線クロスなど、複数のテクニカル分析ツールを組み合わせ、包括的な取引フレームワークを形成します。システムは複数段階の利食いと動的ストップロス機構をサポートするだけでなく、市場状況に応じて取引パラメータを自動調整し、様々な市場環境で高い適応性を維持します。この戦略は特に中長期のトレーダーに適しており、重み配分システムにより取引判断がより堅牢で信頼性の高いものになります。

戦略原理

本戦略の中核はその加重シグナルシステムにあり、5つの異なるサブ戦略を通じて取引シグナルを生成します。

-

MACD戦略:MACDラインとシグナルラインのクロスを利用して市場トレンドの方向性を判断します。MACDラインがシグナルラインを上抜けた場合に買いシグナル、下抜けた場合に売りシグナルが発生します。

-

ストキャスティックRSI戦略:RSIとストキャスティクスの利点を組み合わせ、市場の買われすぎ・売られすぎ状態を監視します。ストキャスティックRSIが設定された売られすぎ閾値を下回った場合に買いシグナル、買われすぎ閾値を上回った場合に売りシグナルが発生します。

-

EMA買われすぎ・売られすぎ戦略:EMAを使用して価格の平均からの乖離度を識別し、RSIが設定された売られすぎ閾値を下回った場合に買いシグナル、買われすぎ閾値を上回った場合に売りシグナルが発生します。

-

スーパートレンド戦略:ATR倍数に基づいて価格チャネルを設定し、トレンドの変化によって取引方向を決定します。スーパートレンド指標が負から正に転じた場合に買いシグナル、正から負に転じた場合に売りシグナルが発生します。

-

移動平均線クロス戦略:異なる期間の2本の移動平均線のクロスを利用して市場トレンドを判断します。短期線が長期線を上抜けた場合に買いシグナル、下抜けた場合に売りシグナルが発生します。

戦略はカスタマイズ可能な重みシステムにより各サブ戦略のシグナルを加重計算し、加重合計が設定された閾値を超えた場合にのみ取引がトリガーされます。さらに、戦略には潜在的な天底識別メカニズムも含まれており、市場が反転する可能性がある場合にポジションを調整します。

この多層的なシグナル確認メカニズムにより、偽シグナルが効果的に減少し、取引システムの信頼性が向上します。同時に、柔軟なパラメータ設定により、様々な取引銘柄や時間足に適応することができます。

戦略の優位性

-

シグナルの多重確認:5つの独立したテクニカル指標からのシグナルを加重計算することで、単一指標による誤った方向性のリスクを低減し、取引シグナルの品質と信頼性を高めます。

-

適応型重みシステム:各サブ戦略に異なる重みを割り当てることができ、トレーダーは各指標への信頼度や過去のパフォーマンスに基づいて戦略の重点を調整でき、柔軟性が向上します。

-

充実したリスク管理:戦略にはストップロス、複数段階の利食い、動的なストップロス調整機能など、多層的なリスク管理体制が組み込まれており、市場が不利な方向に動いた場合でも迅速にリスクをコントロールできます。

-

自動化された潜在天底識別:RSI、出来高、価格動向を総合的に分析することで、潜在的な市場の天井や底を識別し、適切なタイミングでポジションの一部を決済して利益を確定したり損失を軽減したりします。

-

高度なカスタマイズ性:各指標の計算期間、重み値、利食い・ストップロスのパーセンテージなど、ほぼすべてのパラメータを調整可能であり、トレーダーは自身のスタイルや市場条件に合わせて戦略を最適化できます。

-

内蔵ディレイメカニズム:早すぎるエントリーやノイズシグナルに基づく取引を避けるため、戦略はディレイ確認メカニズムを採用しており、持続的なシグナルのみが取引をトリガーするため、短期的な変動の影響を軽減します。

-

時間フィルター機能:戦略では取引の開始日と終了日を設定でき、トレーダーは過去のデータで特定の期間のパフォーマンスをバックテストしたり、既知の異常な市場変動期間を回避したりできます。

戦略のリスク

-

パラメータの過剰最適化リスク:パラメータが多いため、過去のデータへの過学習リスクが存在し、実取引でのパフォーマンス低下につながる可能性があります。解決策は、複数の時間足や銘柄でバックテストを行い、比較的堅牢なパラメータ設定を採用し、特定の過去データに過度に最適化しないことです。

-

市場環境変化リスク:トレンド相場とレンジ相場での戦略パフォーマンスに差が生じる可能性があり、市場状態の急変により戦略の効果が低下する恐れがあります。解決策は、市場環境認識メカニズムを導入し、異なる市場状態に応じてパラメータを調整したり取引を一時停止したりすることです。

-

シグナル競合リスク:複数の指標を同時に使用することで矛盾したシグナルが発生し、判断が混乱する可能性があります。解決策は、各指標の重みを合理的に設定し、より信頼性の高い指標を重視し、シグナル閾値を適切に設定して競合確率を低減することです。

-

不適切な資金管理リスク:戦略にストップロス機構が含まれているものの、不合理な資金管理により資金が急速に枯渇する可能性があります。解決策は、各取引の資金比率を厳格に管理し、単一取引の最大リスクが許容範囲内に収まるようにすることです。

-

技術的障害リスク:自動取引システムはネットワーク断絶、データ遅延などの技術的問題に直面する可能性があります。解決策は、手動介入メカニズムを設定し、システムの稼働状態を定期的に監視し、異常時に迅速に対処することです。

戦略の最適化方向

-

市場環境フィルターの追加:現在の市場がトレンド相場かレンジ相場かを識別する指標を開発し、市場状態に応じて各サブ戦略の重みを動的に調整します。トレンド相場ではトレンドフォロー戦略を強化し、レンジ相場ではスイング戦略を強化します。

-

機械学習の導入:機械学習技術を利用して各指標のパラメータや重みを自動調整し、戦略が最新の市場データから継続的に学習・適応できるようにし、動的な適応力を向上させます。

-

出来高分析の追加:出来高の変化を追加の確認シグナルとして利用し、期待される出来高の裏付けがある場合にのみ取引を実行し、シグナルの信頼性を高めます。

-

潜在天底識別アルゴリズムの最適化:既存の天底識別ロジックを改良し、価格パターンやマルチ時間足確認など、より多くの確認要素を追加して識別精度を向上させます。

-

センチメント指標の追加:恐怖指数(VIX)やコール・プット比率などの市場センチメント指標を統合し、極端な市場センチメント時に取引戦略を調整したり取引を一時停止したりすることで、高ボラティリティ期間中の過剰な取引を回避します。

-

動的な利食い・ストップロス機構の開発:市場のボラティリティに応じて利食い・ストップロス水準を自動調整し、高ボラティリティ時には損失幅を広げ、低ボラティリティ時には狭めることで、リスク管理をより柔軟かつ効果的にします。

-

時間足の最適化:マルチ時間足分析機能を追加し、より上位および下位の時間足が同時にシグナルを確認することを要求し、フェイクアウトや偽シグナルを減少させます。

まとめ

マルチ指標加重スマート取引戦略は、複数のテクニカル分析ツールを統合し、それぞれに異なる重みを割り当てることで、包括的かつ柔軟な取引システムを構築しています。この戦略は、シグナルの多重確認、適応型重みシステム、充実したリスク管理機能に加え、自動化された潜在天底識別メカニズムを備えており、複雑で変化の激しい市場環境において高い適応力を発揮します。

パラメータの過剰最適化、市場環境の変化、シグナル競合などの潜在的なリスクは存在するものの、適切なパラメータ設定、市場環境の認識、厳格な資金管理により、これらのリスクは効果的にコントロール可能です。今後の最適化の方向性としては、市場環境フィルターの追加、機械学習技術の導入、出来高分析の強化、潜在天底識別アルゴリズムの最適化などが挙げられ、これらの改良により戦略の安定性と収益性がさらに向上するでしょう。

体系的な取引方法を求める投資家にとって、このマルチ指標加重スマート取引戦略は検討に値するフレームワークを提供します。感情的要因が取引判断に与える影響を低減できるだけでなく、データ駆動型の方法で継続的に取引パフォーマンスを最適化することが可能です。本戦略を実装する際は、保守的なパラメータ設定から始め、徐々に調整しながら戦略のパフォーマンスを注意深く監視し、自身のリスク選好と市場条件に最も適した設定を見つけることをお勧めします。

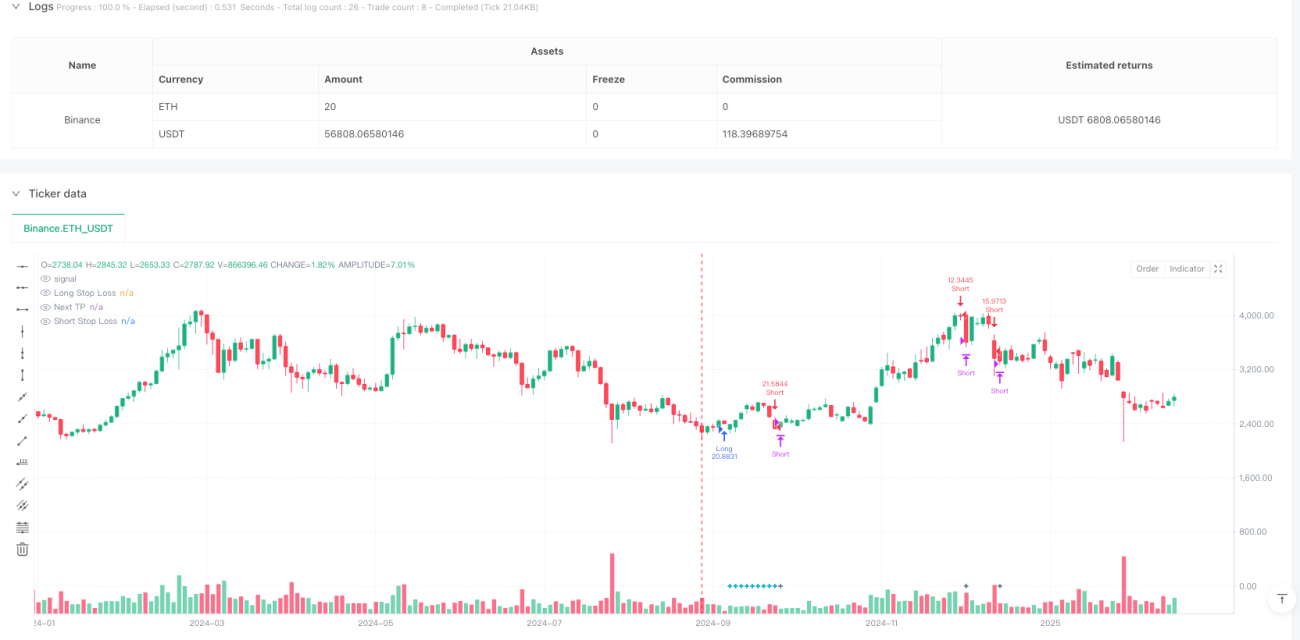

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1