概要

マルチタイムフレーム・モメンタム・コラボレーション取引戦略は、テクニカル指標と複数時間枠分析を組み合わせた定量取引システムです。この戦略の核心は、短期(15分)と長期(4時間)の両方の時間枠における市場の動きを同時に監視し、EMA(指数移動平均)、MA(移動平均)、およびRSI(相対力指数)による協調確認を通じて偽シグナルをフィルタリングし、複数の時間枠が同じ方向を指している場合にのみ取引を行う点にあります。戦略は、EMAクロス、価格ブレイクアウト、RSIモメンタム確認などの複数条件に加え、出来高確認を組み合わせることで、高品質なエントリーシグナルを提供します。さらに、ATR(平均真のレンジ)に基づく動的ストップロス、固定パーセンテージによる利確・損切り、トレーリングストップなどのリスク管理機能も統合し、完全な取引システムを構成しています。

戦略の原理

本戦略の核心原理は、複数のテクニカル指標を複数の時間枠で総合的に分析することにあり、主に以下の部分に分かれます。

-

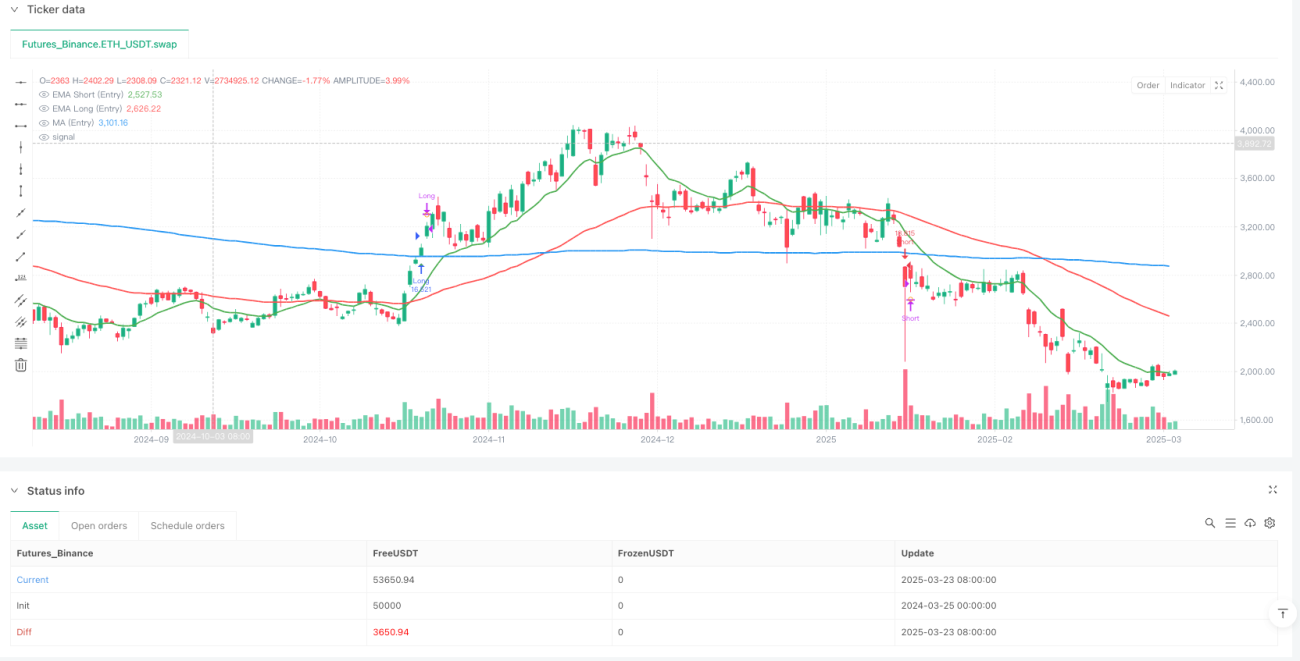

マルチタイムフレーム分析: 戦略は同時に15分(エントリー用)と4時間(トレンド確認用)の2つの時間枠を分析し、取引方向がより大きな市場トレンドと一致していることを確保します。

-

エントリー条件(15分足):

- ロングエントリー: EMA13 > EMA62(短期モメンタムが強気)、終値 > MA200(価格が主要トレンドラインの上)、短期RSI(7) > 長期RSI(28)(モメンタム増加)、短期RSI > 50(モメンタムが強気寄り)、出来高が20期間平均より大きい。

- ショートエントリー: ロング条件とは逆に、EMA13 < EMA62、終値 < MA200、短期RSI(7) < 長期RSI(28)、短期RSI < 50、同様に出来高の増加が必要。

-

トレンド確認(4時間足):

- ロング確認: 15分足の条件と類似しているが、RSI要件が若干異なり、長期RSI > 40を要求。

- ショート確認: 同様に15分足条件とは逆で、長期RSI < 60。

-

精密エントリー条件: 戦略は、EMA13がちょうどEMA62をクロスした(クロス形成)か、価格がちょうどMA200をブレイクしたことを要求します。これにより、すでに長期間継続しているトレンドに盲目でエントリーすることを避け、より正確なエントリーポイントを提供します。

-

エグジットメカニズム: テクニカル指標の逆転(EMA関係の変化やRSIが買われすぎ/売られすぎに達する)、ATR動的ストップロス、固定パーセンテージによる損切り・利確、トレーリングストップなど、複数のエグジットオプションを提供。

戦略の優位性

-

体系化されたマルチタイムフレーム分析: 異なる時間枠の市場状況を総合的に分析することで、短期的な市場ノイズをフィルタリングし、トレンドが明確かつ一致している場合にのみエントリーするため、偽シグナルの可能性を大幅に低減します。

-

多重確認メカニズム: EMA、MA、RSIなどの複数指標による協調確認により、取引シグナルの信頼性が向上します。特に、EMAクロスや価格ブレイクをトリガー条件とすることで、エントリータイミングの精度が高まります。

-

柔軟なリスク管理: ATRベースの動的ストップロス、固定パーセンテージによる利確・損切り、トレーリングストップなど、複数のリスクコントロールオプションを提供しており、トレーダーは自身のリスク選好や市場状況に応じてリスクパラメータを柔軟に調整できます。

-

出来高確認: 出来高増加の条件を追加することで、偽のブレイクアウトの可能性をさらにフィルタリングします。実際の価格変動には通常、出来高の増加が伴うためです。

-

視覚化インターフェース: 各指標の状態やシグナルを表示する直感的なビジュアルパネルを提供し、トレーダーが現在の市場状況や戦略判断を一目で把握できるようにします。

-

高度なカスタマイズ可能性: EMAの長さ、MAの種類、RSIパラメータ、リスク管理倍率など、ほぼすべてのパラメータを入力設定から調整可能であり、トレーダーは異なる市場環境に応じて戦略を最適化できます。

戦略のリスク

-

レンジ相場リスク: 横ばいのレンジ相場では、EMAやMAが頻繁にクロスし、誤ったシグナルの増加や頻繁な取引につながり、連続損失を生む可能性があります。解決策としては、ボラティリティ判断やトレンド強度確認などの追加フィルターを導入し、レンジ相場と明確に識別した場合に取引を停止することが挙げられます。

-

パラメータ最適化のオーバーフィッティング: 指標パラメータを過度に最適化すると、過去のデータでは優れたパフォーマンスを示すが、将来の市場では機能しなくなるリスクがあります。ウォークフォワード分析を用いて戦略のロバスト性を検証し、複数の取引銘柄で固定パラメータをテストすることを推奨します。

-

大幅なギャップリスク: 重要なニュースや突発的なイベント後、市場に大きなギャップが生じ、ストップロスが設定レベルで執行されない可能性があります。より保守的なポジション管理や、ボラティリティに基づくポジション調整メカニズムの導入を検討できます。

-

定量的指標への依存の限界: 戦略は完全にテクニカル指標に依存しており、ファンダメンタル要因を無視しています。重要な経済データの発表や中央銀行の政策変更前には、ポジションを減らすか取引を停止し、突発的なニュースによるリスクを回避することを検討できます。

-

シグナルの遅延性: EMAやMAなどの指標は本質的に遅延性を持っており、トレンドがすでに終盤に差し掛かってからシグナルが発生する可能性があります。EMA期間の調整や、価格パターンやボラティリティ変化などの先行指標と組み合わせることで改善できます。

戦略の最適化方向性

-

市場環境フィルターの追加: 適応型指標や市場構造の判断を導入し、戦略実行前に現在の市場がトレンド相場かレンジ相場かを識別し、それに基づいて取引パラメータを調整または取引を停止します。例えば、ADX(平均方向性指数)を使用してトレンド強度を定量化し、トレンドが明確な場合のみ取引を行うことが考えられます。

-

動的パラメータ調整メカニズム: 現在の戦略は固定のテクニカル指標パラメータを使用していますが、市場のボラティリティに基づいて自動的にパラメータを調整することを検討できます。例えば、低ボラティリティ環境では短期EMAを使用して変動を素早く捉え、高ボラティリティ環境では長期EMAを使用してノイズを低減します。

-

ポジション管理の最適化: 現在の戦略は固定パーセンテージの資金管理を使用していますが、ボラティリティ、勝率予想、またはケリー基準に基づく動的ポジション管理に改善することで、リスク調整後リターンを最大化できます。

-

機械学習要素の追加: 決定木やランダムフォレストなどの機械学習アルゴリズムを導入し、各指標への重み付けを最適化したり、どの市場環境で戦略がより良いパフォーマンスを発揮するかを予測します。

-

ファンダメンタルフィルターの追加: 重要な経済データの発表前に自動的にストップロス範囲を調整したり取引を停止し、潜在的な高ボラティリティイベントに対応します。

-

マルチタイムフレーム重みの最適化: 現在の戦略は単純に2つの時間枠が同じ方向であることを要求していますが、より複雑なマルチタイムフレーム加重システムを導入し、異なる時間枠に異なる重みを与えて総合スコアを算出し、エントリーのタイミングを判断することも考えられます。

-

季節性分析の追加: 一部の取引銘柄には時間的な季節性パターンが存在する可能性があり、過去データを分析してこれらのパターンを発見し、それに基づいて戦略パラメータや取引時間帯を調整します。

まとめ

マルチタイムフレーム・モメンタム・コラボレーション取引戦略は、構造が整い論理が明確な定量取引システムであり、複数時間枠分析と複数指標の協調確認により、市場ノイズを効果的にフィルタリングし、高確率の取引機会を捉えます。戦略はテクニカル分析の古典的指標であるEMA、MA、RSIを統合し、正確なエントリー要件と充実したリスク管理システムにより取引の質を高めています。

本戦略の最大の強みは、その多重確認メカニズムとマルチタイムフレーム協調分析にあり、これにより偽シグナルを減らし、取引が主要トレンドと一致することを保証します。同時に、完備されたリスク管理オプションにより、トレーダーはリスクエクスポージャーを柔軟にコントロールできます。しかし、戦略にはレンジ相場でのパフォーマンス低下、パラメータ最適化のオーバーフィッティング、テクニカル指標の遅延性などのリスクも存在します。

今後の最適化方向性は、主に市場環境の分類、パラメータの動的調整、機械学習の応用、より多くの時間次元分析の統合などにあります。これらの最適化を通じて、戦略は様々な市場環境で安定したパフォーマンスを維持し、勝率とリスク調整後リターンをさらに向上させることが期待されます。

体系的かつ規律ある取引方法を求めるトレーダーにとって、本戦略は強固なフレームワークを提供します。そのまま適用することも、個人の取引システムの基礎としてカスタマイズし拡張することも可能です。

- 1