2

Follow

502

Followers

概要

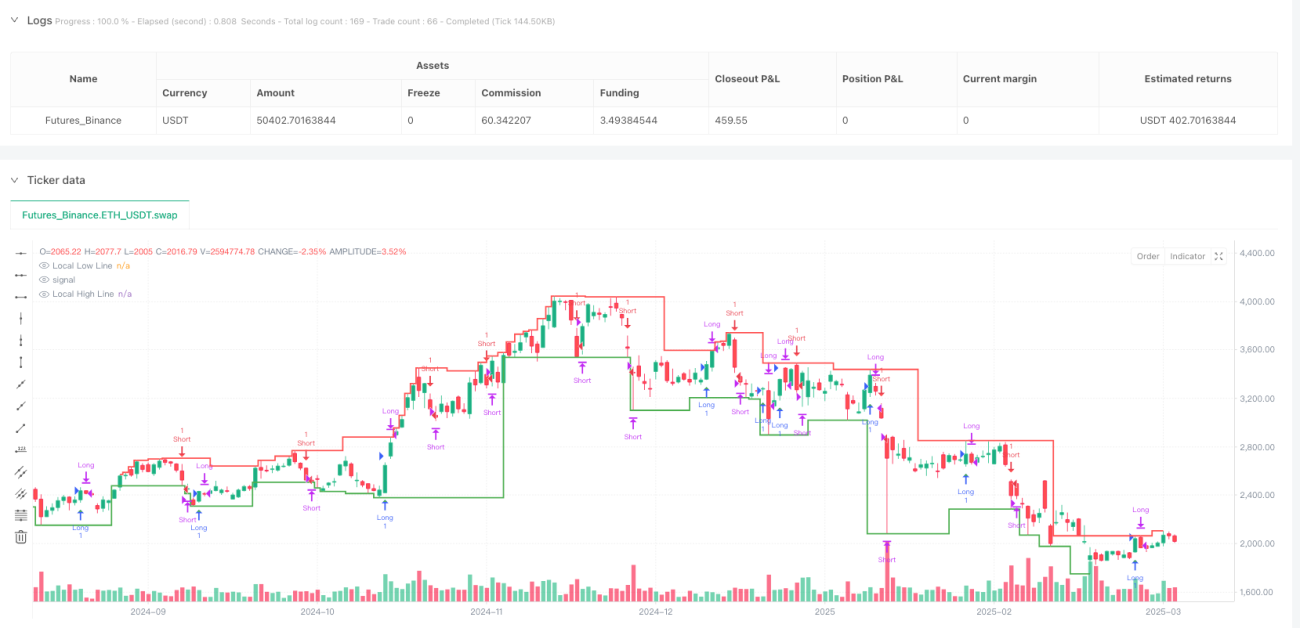

これは、流動性ゾーン分析と内部市場構造のダイナミクスを組み合わせ、高確率のエントリーポイントを特定することを目的とした革新的な取引戦略です。価格と主要な市場レベルの相互作用を追跡し、内部市場の転換を利用して取引をトリガーすることで、トレーダーに柔軟かつ正確な市場参入方法を提供します。

戦略の原理

戦略の核となるロジックは、流動性ゾーンの特定と内部市場の転換という2つの主要コンポーネントに基づいています。流動性ゾーンは局所的な高値と安値を分析することで動的に決定され、内部市場の転換は価格が以前の強気または弱気の水準を突破したかどうかに基づいて市場の方向性の変化を判断します。

戦略には以下の主要な特徴があります:

- 内部市場転換ロジック:従来のローソク足パターンに依存せず、価格が主要水準を突破したことに基づく

- 流動性ゾーンの追跡:重要な流動性ゾーンを動的に特定し、弱い市場条件下での取引を防止

- モードの柔軟性:「Both」「Bullish Only」「Bearish Only」の3つの取引モードを提供

- リスク管理:ストップロスとテイクプロフィットの水準をカスタマイズ可能

- 時間範囲制御:取引時間帯を正確に制御可能

戦略の利点

- 動的適応性:戦略は市場構造の変化に迅速に対応可能

- 正確なエントリー:流動性ゾーンと内部市場の転換を組み合わせることで、エントリーの精度を向上

- リスク管理可能:内蔵されたストップロスとテイクプロフィットのメカニズム

- 柔軟性が高い:市場の状況に応じて取引モードを選択可能

- 多次元分析:価格行動、流動性、市場構造を同時に考慮

戦略のリスク

- 市場の激しい変動により、ストップロスが発動される可能性がある

- レンジ相場では、頻繁なシグナルが取引コストを増加させる可能性がある

- パラメータ設定が不適切な場合、戦略のパフォーマンスに影響を与える可能性がある

- バックテストの結果は実取引と差異が生じる可能性がある

戦略の最適化方向

- 機械学習アルゴリズムを導入し、パラメータの自己適応最適化を実施

- 出来高やボラティリティ指標などの追加フィルター条件を増やす

- マルチタイムフレーム検証メカニズムの開発

- ストップロスとテイクプロフィットのアルゴリズムを最適化し、市場ボラティリティに応じた動的調整を考慮

まとめ

これは、流動性分析と市場構造のダイナミクスを融合した革新的な取引戦略です。柔軟な内部市場転換ロジックと正確な流動性ゾーントラッキングにより、トレーダーに強力な取引ツールを提供します。戦略の鍵はその適応性と多次元分析能力にあり、さまざまな市場条件下で高い実行効率を維持できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1