2

Follow

502

Followers

概要

これは、市場のボラティリティ、トレンド、モメンタムを総合的に分析し、高い確率で取引機会を特定することを目的とした、複数のテクニカル指標に基づく動的なオプション取引戦略です。本戦略は、ATR(平均真のレンジ)、ボリンジャーバンド(BB)、RSI(相対力指数)、VWAP(出来高加重平均価格)などの複数のテクニカル指標を組み合わせ、包括的な取引判断フレームワークを形成します。

戦略の原理

戦略の核となる原理は、複数の市場シグナルを活用して取引判断を構築することです。主な手順は以下の通りです。

- ボリンジャーバンドの上限・下限を価格のブレイクアウトシグナルとして使用

- RSIを組み合わせて市場の買われすぎ・売られすぎの状態を判断

- 出来高の異常を検出してトレンドを確認

- ATRを使用して動的なストップロスと利益確定目標を計算

- 最大保有時間を設定してリスクを制限

戦略のメリット

- 複数因子の分析により取引シグナルの精度が向上

- 動的なストップロスと利益確定メカニズムによりリスクを効果的に管理

- 柔軟なパラメータ設定により様々な市場環境に適応可能

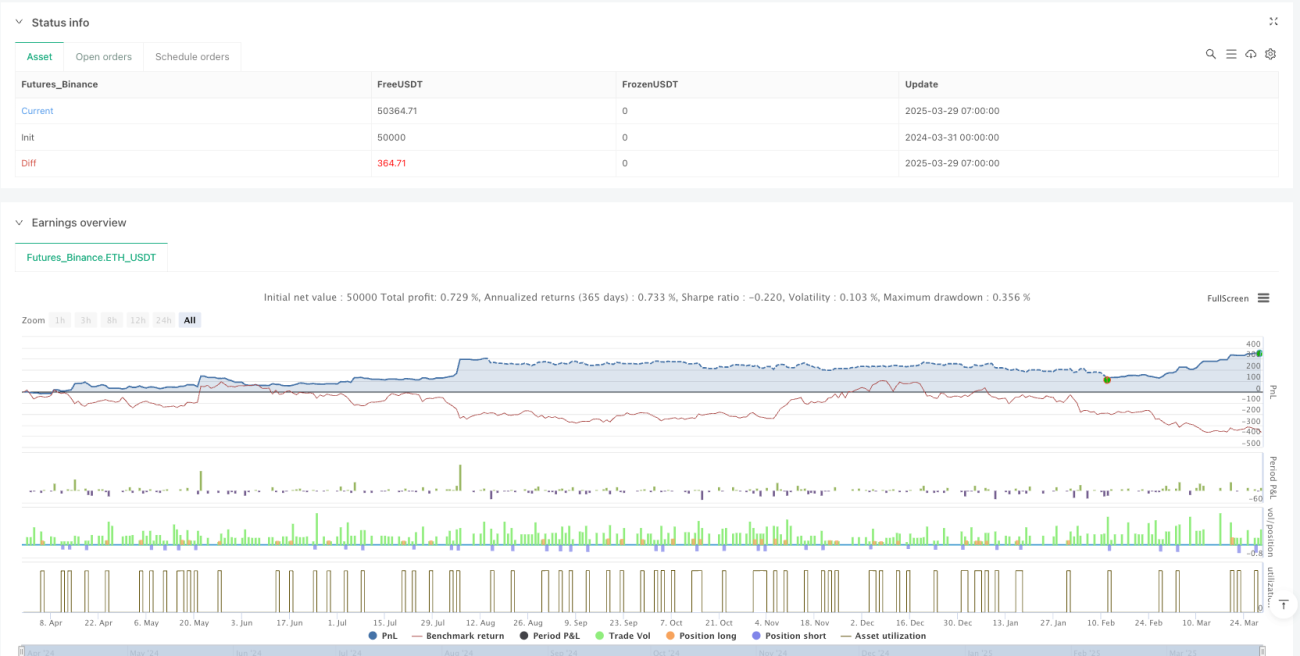

- バックテストの結果、高い勝率とプロフィットファクターを示す

- 時間ベースのエグジット戦略により過度な保有を防止

戦略のリスク

- テクニカル指標の遅延により誤ったシグナルが発生する可能性

- 高いボラティリティの市場では取引の複雑性が増す可能性

- パラメータの選択が戦略のパフォーマンスに大きな影響を与える

- 取引コストとスリッページが実際の収益に影響を与える可能性

- 市場環境の急激な変化により戦略の効果が低下する可能性

戦略の最適化の方向性

- 機械学習アルゴリズムを導入してパラメータ選択を最適化

- より多くの市場センチメント指標を追加

- 動的パラメータ調整メカニズムの開発

- リスク管理モジュールの最適化

- クロスマーケット相関分析の導入

まとめ

本戦略は、複数因子分析により比較的堅牢なオプション取引フレームワークを構築しています。テクニカル指標、リスク管理、動的エグジットメカニズムを総合的に活用することで、トレーダーに体系化された取引手法を提供します。ただし、どの取引戦略も継続的な検証と最適化が必要です。

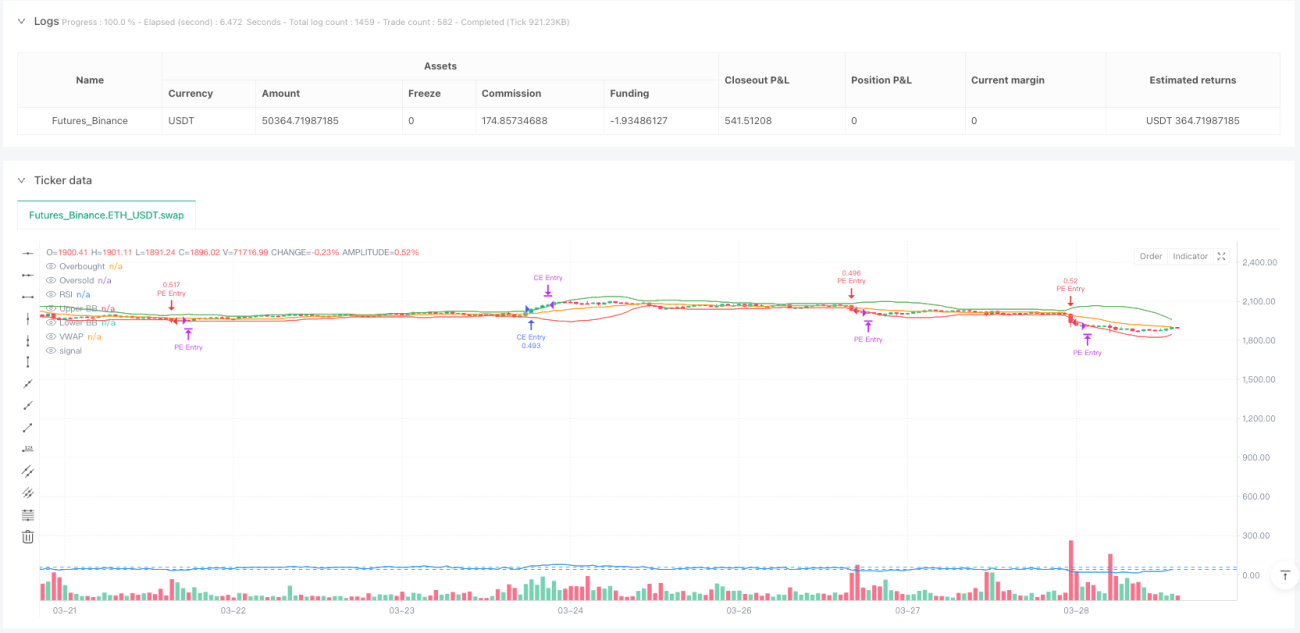

パフォーマンス指標

-

5分足:

- 勝率:77.6%

- プロフィットファクター:3.52

- 最大ドローダウン:-8.1%

- 平均取引保有時間:2.7時間

-

15分足:

- 勝率:75.9%

- プロフィットファクター:3.09

- 最大ドローダウン:-9.4%

- 平均取引保有時間:3.1時間

Source

Pine

/*backtest

start: 2024-03-31 00:00:00

end: 2025-03-29 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Vinayz Options Stratergy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=2)

// ---- Input Parameters ----Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1