2

Follow

502

Followers

概要

これは革新的な量化取引戦略であり、流動性ゾーンエントリー、ATR変動閾値、および動的リスク管理を統合することで、トレーダーに構造化された取引手法を提供します。本戦略は複数のテクニカル分析指標を組み合わせ、高確率の取引機会を特定し、自動で利益確定および損切り水準を計算することを目的としています。

戦略の原理

戦略の核心原理は、以下の重要な要素に基づいています。

- 流動性ゾーン分析:特定の期間内の最安値と最高値を計算し、潜在的なサポートおよびレジスタンスゾーンを特定します。

- ATR変動率フィルター:平均真実範囲(ATR)をエントリーおよびリスク管理の動的閾値として使用します。

- トレンドフィルター:50期間指数移動平均線(EMA)と相対力指数(RSI)を組み合わせて、市場トレンドとモメンタムを確認します。

- 動的リスク管理:ATRに基づいて自動的に利益確定および損切り水準を計算し、リスク/リワード比率を柔軟に調整できます。

戦略の利点

- 多次元シグナル生成:流動性、変動率、トレンドフィルターを組み合わせることで、シグナルの品質を向上させます。

- 適応型リスク管理:損切り・利益確定を動的に調整し、取引リスクを効果的に制御します。

- 柔軟なパラメータ設定:ATR期間、流動性周期、取引時間帯をカスタマイズ可能です。

- 可視化サポート:流動性ラインおよび最初のローソク足水準の可視化表示を提供します。

- パフォーマンス追跡:チャート上に直接勝率や勝敗状況を表示する取引統計テーブルを内蔵しています。

戦略のリスク

- パラメータ敏感性:戦略のパフォーマンスはパラメータ選択に大きく依存するため、継続的なバックテストと最適化が必要です。

- 市場適応性:トレンドが不明瞭または変動の激しい市場では、パフォーマンスが不安定になる可能性があります。

- フェイクブレイクアウトのリスク:流動性ゾーンのブレイクアウトに誤ったシグナルが含まれる可能性があります。

- 取引頻度:セッションフィルターと複数の条件により、取引機会が減少する可能性があります。

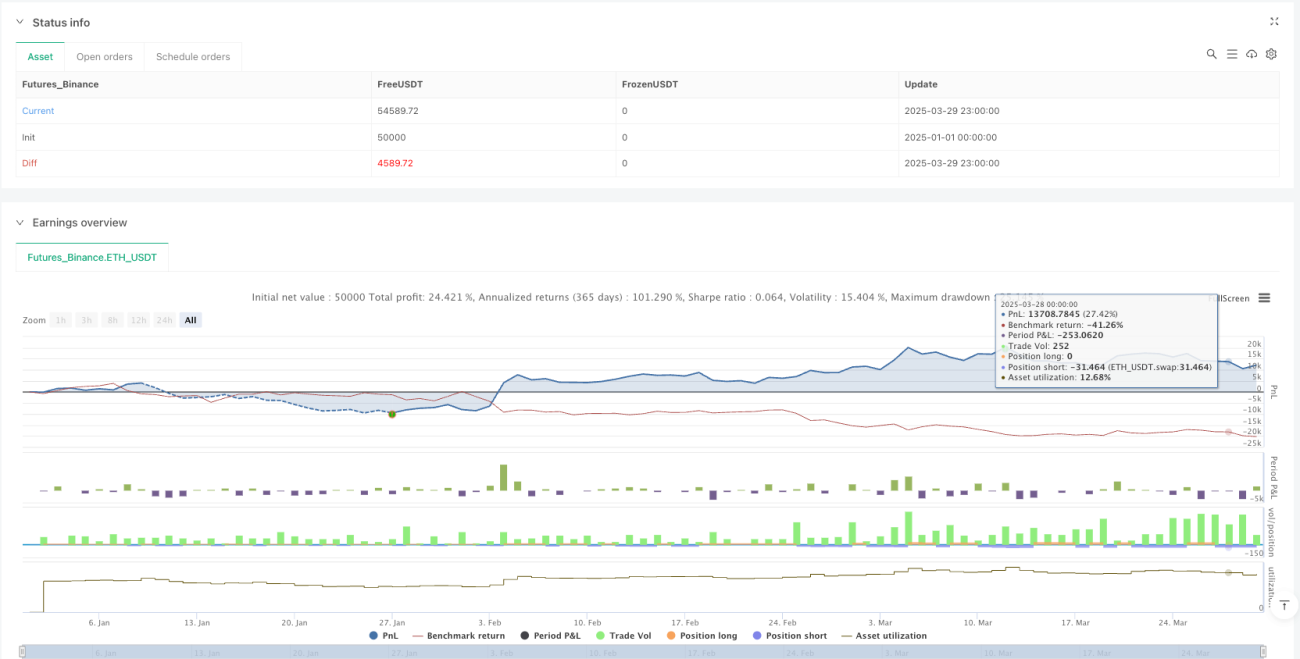

- バックテストバイアス:過去データでの64%の勝率は、将来のパフォーマンスを完全に示すものではありません。

戦略の最適化方向

- 機械学習の統合:機械学習アルゴリズムを導入し、パラメータとシグナル生成を動的に調整します。

- マルチ市場適応性:異なる市場や商品に適用可能な、より汎用的なパラメータ設定を開発します。

- 高度なリスク管理:より複雑なポジションサイジングとリスク配分アルゴリズムを導入します。

- シグナル確認メカニズム:出来高やその他のテクニカル指標など、追加の確認指標を導入します。

- リアルタイムパフォーマンス監視:リアルタイムのパフォーマンス評価と適応調整モジュールを開発します。

まとめ

ThinkTech AI取引戦略は、革新的な多因子アプローチにより、トレーダーに強力な量化取引ツールを提供します。流動性分析、変動率フィルター、動的リスク管理を通じて、本戦略は高品質な取引機会を特定することを目指しています。しかし、トレーダーは戦略の潜在能力を最大限に引き出すために、継続的なバックテスト、最適化、および慎重な適用が必要です。

Source

Pine

/*backtest

start: 2025-01-01 00:00:00

end: 2025-03-30 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

if high > ta.highest(high[1], 5)

strategy.entry("Enter Long", strategy.long)

else if low < ta.lowest(low[1], 5)

strategy.entry("Enter Short", strategy.short)//@version=6Strategy parameters

Comment

All comments (0)

No data

- 1