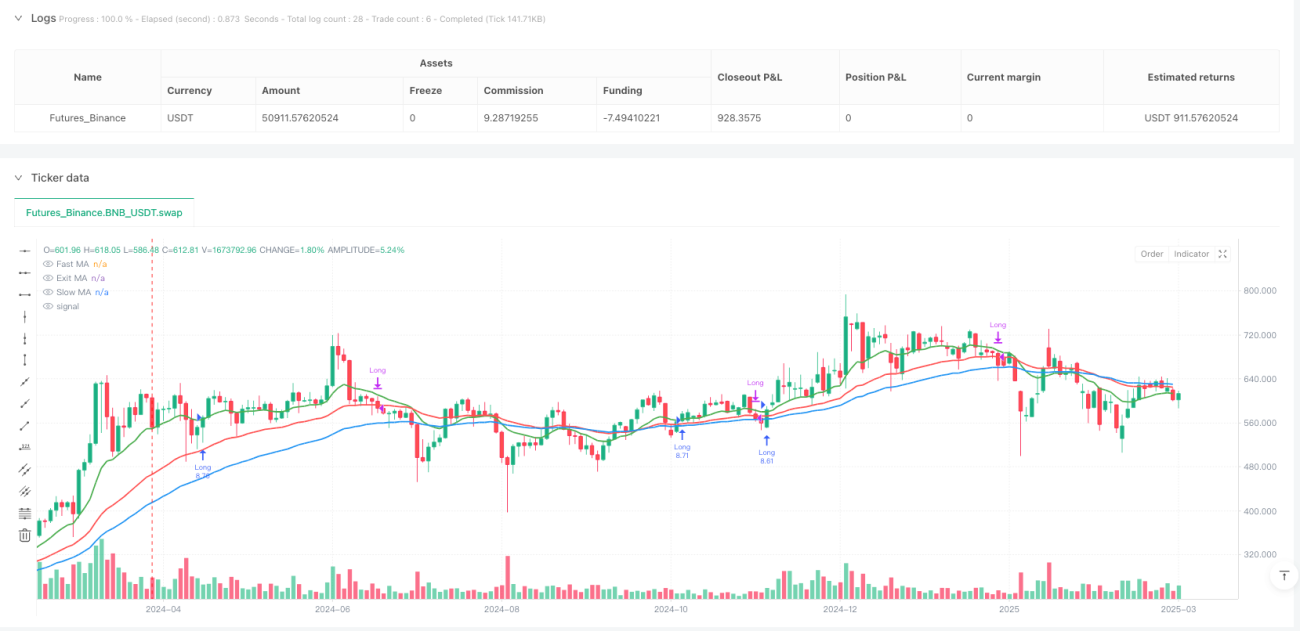

設定可能な移動平均線クロス戦略

2

Follow

502

Followers

概要

本稿では、市場の状況に応じて移動平均線のパラメータや種類をカスタマイズできる、柔軟かつ強力な移動平均線クロス取引戦略を紹介します。この戦略の核心は、異なる期間と種類の移動平均線を利用してトレンドを追跡し、シグナルを生成することにあります。

戦略の原理

この戦略は、3つの異なる期間の移動平均線(ファストライン、スローライン、エグジットライン)を計算し、取引シグナルを生成します。主な原理は以下の通りです。

- 移動平均線の種類選択:単純移動平均線(SMA)、指数平滑移動平均線(EMA)、加重移動平均線(WMA)、ヘル移動平均線(HMA)をサポートしています。

- エントリー条件:

- ロングエントリー:終値がファストラインより高く、ファストラインがスローラインより高く、かつ終値がエグジットラインより高い

- ショートエントリー:終値がファストラインより低く、ファストラインがスローラインより低く、かつ終値がエグジットラインより低い

- エグジット条件:

- ロングエグジット:エントリー後最低2本のローソク足が経過した後、終値がエグジットラインより低い

- ショートエグジット:エントリー後最低2本のローソク足が経過した後、終値がエグジットラインより高い

戦略の利点

- 高度な設定自由度:トレーダーは移動平均線の期間や種類を柔軟に調整可能

- 多市場への適応性:パラメータ調整により、さまざまな流動性の取引銘柄に適用できる

- 強いトレンドフォロー能力:複数の移動平均線で偽シグナルをフィルタリング

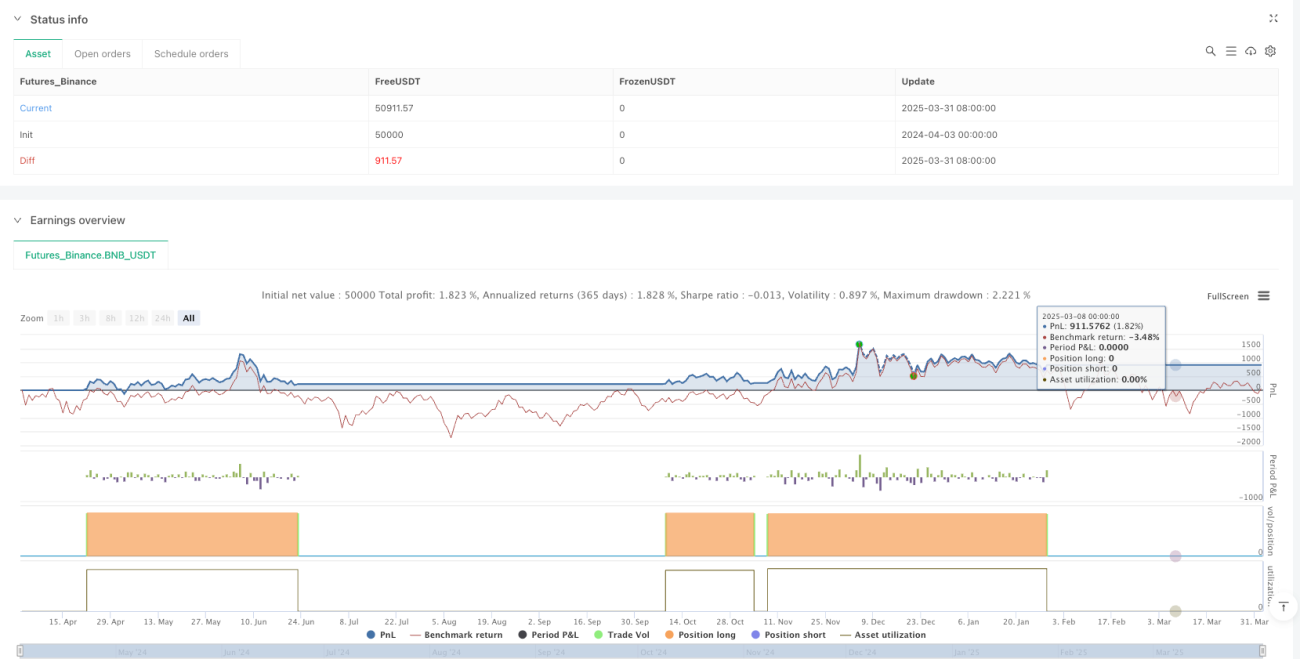

- リスク管理:デフォルト設定で口座残高の10%をポジション管理に使用

- 柔軟な取引方向:ショート取引の有効/無効を選択可能

戦略のリスク

- パラメータ敏感性:市場によって最適な移動平均線パラメータが異なる可能性がある

- トレンド相場でのパフォーマンスが良好:レンジ相場では無効なシグナルが増える可能性がある

- 取引コスト:戦略のデフォルト設定では0.06%の取引手数料を想定。実際の取引では考慮が必要

- バックテストの限界:現時点では一部の銘柄(BTCUSDやNIFTYなど)でのみ初期的な検証を行っている

戦略の最適化方向

- 動的パラメータ調整:適応型移動平均線期間の導入

- 他のテクニカル指標との組み合わせ:RSIやMACDなどの指標を追加してシグナルをフィルタリング

- ストップロス機構:ボラティリティに基づくストップロス戦略の追加

- マルチタイムフレーム検証:異なる時間軸での総合的なバックテスト

- 機械学習による最適化:アルゴリズムを使用して最適なパラメータ組み合わせを自動探索

まとめ

設定可能な移動平均線クロス戦略(MA-X)は、柔軟なトレンドフォローのフレームワークを提供します。適切な設定と継続的な最適化により、この戦略は定量取引ツールボックスにおいて強力なツールとなり得ます。トレーダーは各市場の特性に応じて個別に調整し、十分なバックテストと検証を行う必要があります。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1