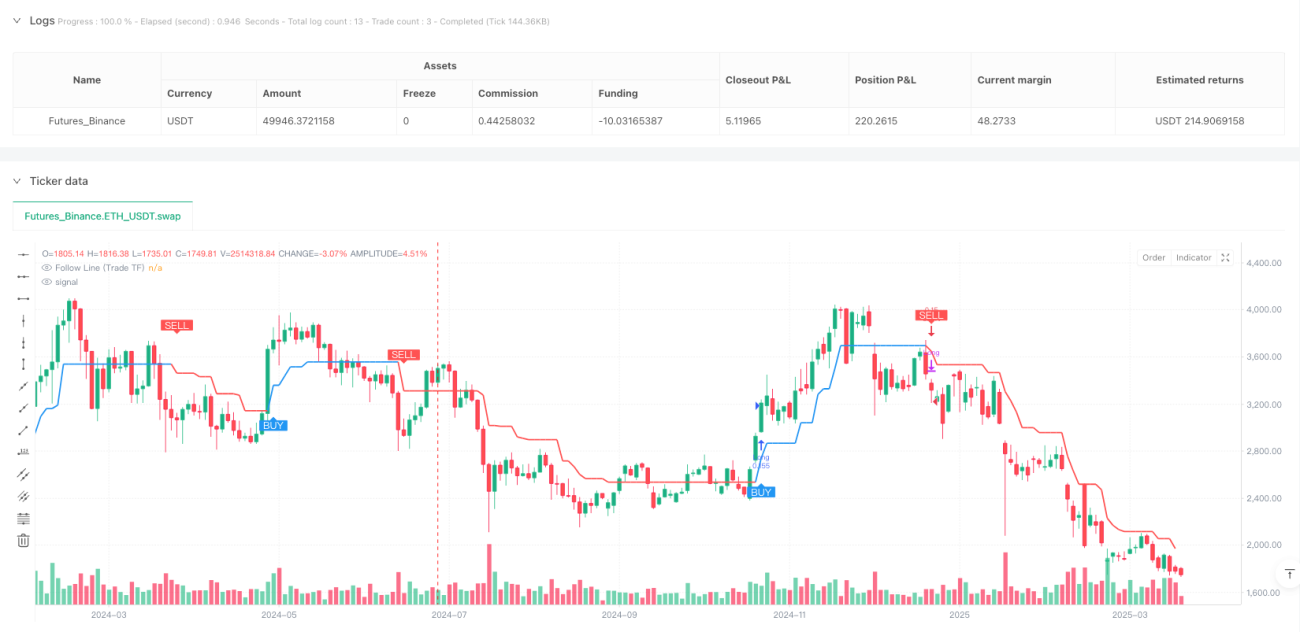

戦略概要

ボリンジャーバンドとATR動的トレンド追跡戦略は、ボリンジャーバンドのブレイクシグナルと平均真実レンジ(ATR)の動的調整機能を組み合わせ、『追跡線(フォローライン)』メカニズムを通じて市場トレンドを識別・追跡する高度な定量取引システムです。本戦略は特にマルチタイムフレーム(HTF)確認メカニズムを導入しており、より高次の時間枠のトレンド方向に基づいて取引シグナルをフィルタリングし、戦略の安定性と収益性を大幅に向上させます。また、システムにはオプションの取引時間フィルター、ATRボラティリティ適応調整、HTFトレンド変化へのリアルタイム反応メカニズムなど、複数の高度な機能が含まれており、包括的で柔軟な定量取引ソリューションを提供します。

戦略原理

本戦略の中核は『追跡線』メカニズムであり、以下の手順で市場トレンドを動的に識別・適応します。

-

ボリンジャーバンドシグナル生成:システムはまず標準的なボリンジャーバンドを計算し、価格が上限バンドを突破した場合に強気シグナル(1)、下限バンドを突破した場合に弱気シグナル(-1)、バンド内の場合は中立シグナル(0)を生成します。

-

追跡線計算:ボリンジャーバンドのシグナルと現在の価格位置に基づき、システムは一時的な追跡線値を計算します。強気シグナルの場合、追跡線は現在のローソク足の安値からATR値を差し引いた値(ATRフィルター有効時)、または安値をそのまま使用します。弱気シグナルの場合、追跡線は現在のローソク足の高値にATR値を加えた値(ATRフィルター有効時)、または高値をそのまま使用します。

-

追跡線ロックメカニズム:戦略は『ラチェット』ロジックを用いて追跡線を維持します。上昇トレンドでは、新しい追跡線値は一時的な値と前回の値の大きい方を取ります。下降トレンドでは、小さい方を取ります。これにより、追跡線はトレンド方向にのみ移動でき、動的なサポート/レジスタンスレベルを形成します。

-

トレンドの確定:現在の追跡線と前回の追跡線値を比較することで、システムはトレンド方向を確定します。上昇は強気トレンド(1)、下降は弱気トレンド(-1)、横ばいは前回のトレンドを維持します。

-

マルチタイムフレーム分析:戦略は同様のロジックを高次時間枠(HTF)で使用して追跡線とトレンド状態を計算し、自動または手動で適切なHTF(例:1分足に自動対応する15分足HTF)を選択できます。

-

エントリー条件:取引時間枠のトレンドが中立または下降から上昇に転じ、かつHTFが上昇トレンドと確認された場合にロングシグナルが発生します。逆の場合にショートシグナルが発生します。

-

エグジット条件:取引時間枠のトレンドが逆方向になった場合、またはHTFのトレンドが逆方向になった場合(v2.5で追加)、戦略は保有ポジションを決済します。

-

時間フィルター:特定の取引時間帯(例:通常の米国株式取引時間0930-1600)のみで取引を実行するオプションがあります。

戦略の利点

-

高い適応性:追跡線メカニズムは市場のボラティリティに応じて自動調整されます。特にATRフィルターを有効にした場合、異なるボラティリティ環境に対して動的な適応力を発揮します。

-

トレンド確認メカニズム:マルチタイムフレーム確認機能により『ノイズ』取引を効果的にフィルタリングし、HTFトレンド方向が一致する場合のみ取引を行うことで、シグナルの品質が大幅に向上します。

-

柔軟な設定オプション:ボリンジャーバンドの期間と偏差、ATR期間、時間フィルター、HTF選択方法など、豊富なパラメーター設定が可能で、さまざまな市場や取引銘柄に最適化できます。

-

高い応答性:v2.5で追加されたHTFトレンド変化への反応メカニズムにより、戦略は大きなトレンド変化に迅速に対応し、早期に損切りを行い、深刻なドローダウンを回避できます。

-

可視化補助:チャート上に取引時間枠とHTFの追跡線を描画し、オプションで売買シグナルラベルも表示可能なため、取引ロジックが直感的に理解できます。

-

ポジション管理:pyramiding=0設定により同一方向への複数回エントリーを防止し、不要なリスクの蓄積を回避します。

戦略のリスク

-

偽ブレイクアウトのリスク:ボリンジャーバンドとHTF確認を使用していても、市場は特に高ボラティリティ環境において偽ブレイクアウトを発生させる可能性があります。解決策:ボリンジャーバンドの偏差値を大きくするか、確認期間を延長する、あるいは追加のブレイク確認メカニズムを導入することが考えられます。

-

パラメーター感度:戦略のパフォーマンスはATR期間やボリンジャーバンド設定などのパラメーターに敏感です。解決策:バックテストを通じて特定の取引銘柄に最適なパラメーターの組み合わせを見つけ、過度な最適化によるカーブフィッティング問題を避ける必要があります。

-

トレンド変化の遅れ:追跡線メカニズムはトレンド初期段階での反応が遅く、エントリーが遅れる可能性があります。解決策:より小さなATR乗数やボリンジャーバンド期間を使用して応答速度を上げることが考えられますが、シグナルの品質と応答性のバランスを取る必要があります。

-

時間枠依存性:不適切なHTF選択は過度なフィルタリングやシグナル競合を引き起こす可能性があります。解決策:自動HTF選択機能を使用することを推奨します。この機能は現在のチャート時間枠に基づいて適切な高次時間枠を自動選択します。

-

資金管理の欠如:戦略自体には完全な資金管理メカニズムが含まれていません。解決策:実際の適用では、固定パーセンテージリスクやATR倍数ストップロスなど、適切なストップロス戦略とポジション管理ルールを組み合わせる必要があります。

戦略の最適化方向

-

シグナルフィルターの強化:相対力指数(RSI)やストキャスティクスなどの他のテクニカル指標を導入してエントリーシグナルを確認し、指標が買われすぎ/売られすぎの状態を示した場合のみ取引を実行することが考えられます。これにより、偽ブレイクシグナルをさらに減らし、勝率を向上させます。

-

動的パラメーター調整:市場の状態に基づく適応的パラメーター調整メカニズムを開発できます。例えば、高ボラティリティ環境では自動的にボリンジャーバンドの偏差値を増加させ、低ボラティリティ環境では減少させることで、戦略がさまざまな市場状況にうまく適応できるようになります。

-

HTFトレンド判断の最適化:HTFトレンド確認アルゴリズムを改善し、追跡線方向のみに依存するのではなく、指数平滑移動平均線のクロスオーバーや他のトレンド指標を導入することで、より安定したトレンド判断を得ることができます。

-

資金管理の充実:包括的な資金管理システムを統合し、市場のボラティリティとアカウントサイズに基づいてポジションサイズを動的に調整し、ATRベースのストップロスレベルと利益目標を設定することで、リスク調整後リターンを最大化します。

-

市場状態分析の追加:市場環境の分類を導入し、トレンド相場とレンジ相場を区別し、市場状態に応じて戦略パラメーターや取引ルールを自動調整します。また、本戦略に不適切な市場環境では取引を一時停止することも検討します。

-

マルチ戦略統合:本戦略を一つのコンポーネントとし、他の補完的戦略(逆張り戦略やブレイク確認戦略など)と組み合わせて、完全な戦略ポートフォリオを形成し、さまざまな市場環境でのパフォーマンスバランスを取ります。

まとめ

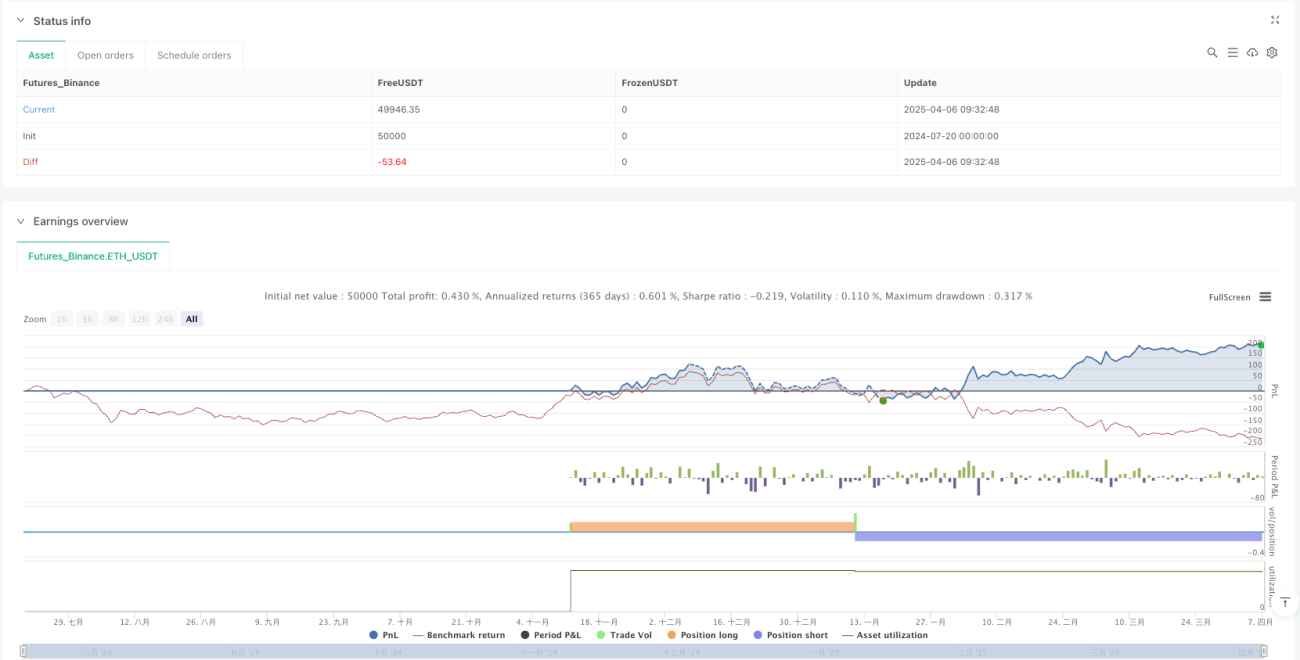

ボリンジャーバンドとATR動的トレンド追跡戦略は、ボリンジャーバンド、ATR、マルチタイムフレーム分析を組み合わせ、市場トレンドを効果的に識別・追跡する精巧に設計された定量取引システムです。本戦略の中核的な利点は、その適応性と柔軟性にあり、市場状況に応じて動的に調整しながら、HTF確認メカニズムによりシグナル品質と勝率を向上させます。

パラメーター感度や偽ブレイク問題などいくつかの固有リスクは存在しますが、適切なパラメーター最適化と追加のフィルタリングメカニズムにより緩和できます。シグナルフィルターの強化、動的パラメーター調整、資金管理の充実などの戦略最適化方向は、戦略パフォーマンスをさらに向上させるための明確な道筋を提供します。

全体として、本戦略は中長期のトレンドフォロートレーダーに特に適しており、トレンド変化を識別し、有利な市場条件下で取引を実行するための堅牢なフレームワークを提供します。適切なパラメーター設定と適切なリスク管理により、本戦略はさまざまな市場環境で安定したリターンを生み出す可能性を秘めています。

/*backtest

start: 2024-07-20 00:00:00

end: 2025-04-07 00:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=6

//@fenyesk

//Optional Working Hours and ATR based TP/SL removed

// Added Optional Higher Timeframe Confirmation with Auto/Manual Selection- 1