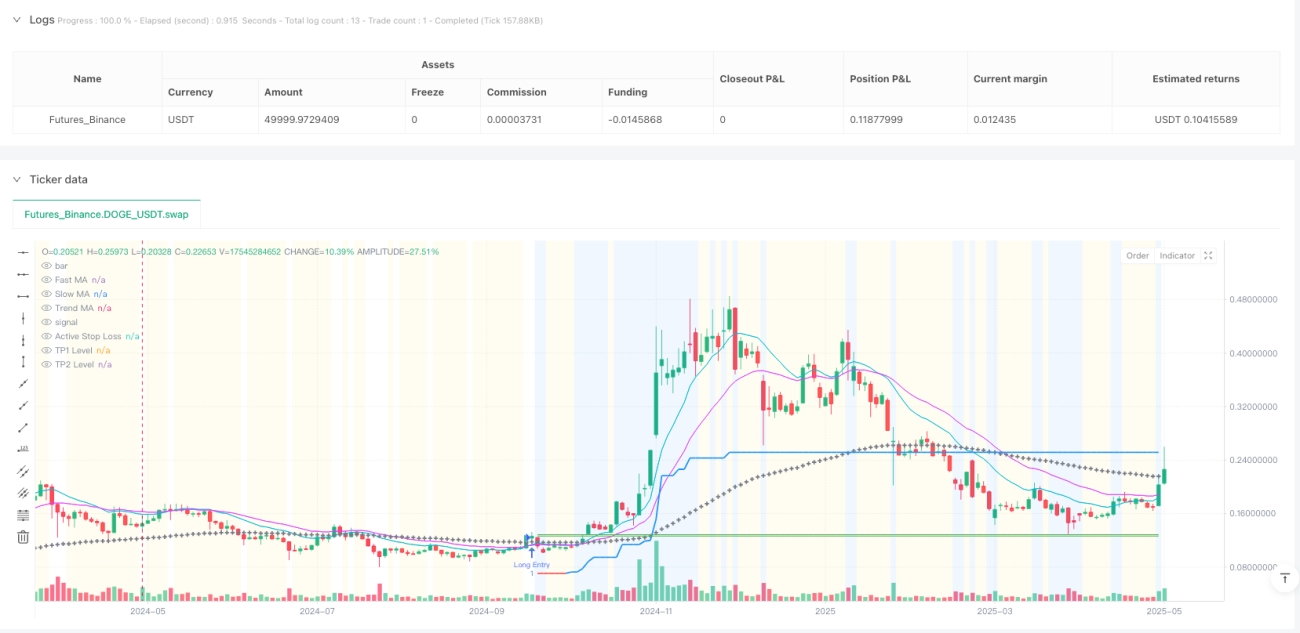

戦略概要

適応型移動平均線クロス・ボラティリティ・トラッキング定量取引戦略は、高頻度取引およびショートトレード向けに設計されたシステム化戦略です。本戦略の核は、高速移動平均線(MA)と低速移動平均線のクロスを主要シグナル発動点とし、複数の重要フィルターと精密なリスク管理ツールを組み合わせることで、小幅ながら急激な価格変動を捉えます。戦略は高いカスタマイズ性を持ち、ユーザーは移動平均線の種類(EMA、SMA、WMA、HMA、VWMA)や期間パラメータを柔軟に選択でき、様々な市場ペースの取引ニーズに対応できます。さらに、本戦略はAPI対応で、自動売買システムにシームレスに統合でき、シグナルの迅速な実行を実現します。特に高頻度・小額利益を追求するショートトレーダーに適しています。

戦略の原理

本戦略のコアロジックは以下の主要部分で構成されます:

-

エントリーシグナル:主に高速移動平均線と低速移動平均線のクロス/クロスオーバーをエントリー発動条件とします。ユーザーは移動平均線の種類(EMA、SMA、WMA、HMA、VWMA)と期間を柔軟に設定でき、シグナルの感度を調整して市場状況に適応できます。

-

トレンドフィルター:戦略はオプションで長期移動平均線を大トレンドフィルターとして使用し、取引を大トレンド方向にのみ行うよう制限します。強い方向性のある市場での逆張り短期取引を回避します。

-

確認フィルター:

- ATRボラティリティフィルター:極端にフラットまたは「沈黙」した市場ではエントリーを一時停止する設計です。これらの市場ではボラティリティが動的しきい値(平均ATRに基づく)を下回るため、無トレンド・低エネルギー状態での揉み合いを防ぎます。

- 出来高フィルター:最低限の市場参加(出来高とその移動平均線との比較)を要求することでエントリーシグナルを検証し、低流動性の急騰や重要でない価格行動に基づくエントリーを回避します。

-

リスク管理スイート:

- 初期ボラティリティストップロス:ATRベースの初期ストップロスは、各トレードのリスク定義に客観的な出発点を提供し、直近のボラティリティに適応します。

- ATRトレーリングストップロス:動的な市場において重要で、ストップロスラインが有利な価格変動に応じて調整され、成功した短期トレードの利益を保護しつつ、トレンド反転時には比較的迅速に損失を縮小します。

- 損益分岐点ストップロス(オプション):TP1到達または価格が特定のATR距離移動した後、ストップロスを自動的にエントリー価格(プラス緩衝)に移動します。初期成功を示したトレードのリスクを迅速に中立化します。

- 二重利益確定レベル:TP1とTP2の2つの利益目標を設定。TP1は迅速な部分利益確定(例:50%)、TP2は残りポジションの更大な利益獲得を狙います。

-

ポジション管理:固定数量のポジションサイズを採用し、各トレードのポジション規模を正確に制御します。高頻度環境での一貫したリスク適用とAPIコマンド生成に不可欠です。

戦略の優位性

コードを詳細に分析した結果、本戦略には以下の明確な利点があります:

-

高いカスタマイズ性:ユーザーは移動平均線の種類や期間、フィルター設定、リスク管理パラメータなど様々なパラメータを柔軟に調整でき、様々な市場環境や取引スタイルに適応できます。

-

多層フィルター機構:トレンド、ボラティリティ、出来高フィルターを組み合わせることで、誤シグナルや市場ノイズを効果的に低減し、取引の質を向上させます。

-

完善なリスク管理:戦略には複数のストップロス機構(初期、トレーリング、損益分岐点)と二重利益確定目標が組み込まれており、精密なリスクコントロールと利益保護を実現します。

-

APIフレンドリー設計:明確なエントリー・エグジットロジックが曖昧さのないシグナルを生成し、外部取引システムとの統合が容易で、ほぼ即時の注文執行を可能にします。

-

精密なポジションコントロール:固定数量のポジションサイズにより、APIエンドポイントのペイロードが簡素化され、自動実行の信頼性が向上します。

-

適応性の高さ:パラメータ調整により、高頻度短期取引モードからより長期のトレンドフォロー型モードへと切り替えられ、様々な市場条件や個人の取引選好に対応します。

戦略のリスク

本戦略はよく設計されていますが、以下の潜在的なリスクと課題があります:

-

パラメータ最適化リスク:戦略には多くの設定可能なパラメータが含まれるため、過度な最適化によりバックテスト結果は良好でも実績が悪化する可能性があります(オーバーフィッティング)。投資家はサンプル外データでの検証やフォワードテストでこのリスクを回避すべきです。

-

取引コストの影響:高頻度取引は大量の取引を意味し、累積された手数料とスリッページが純利益に大きく影響する可能性があります。使用前にこれらのコストを正確に計算してバックテストに反映させることが必須です。

-

シグナル品質の変動:市場条件によって移動平均線クロスの信頼性は変化します。特に揉み合い相場や変動の激しい市場では注意が必要です。

-

技術依存性:API対応戦略であるため、実行速度と技術的安定性に効果が左右されます。システムの遅延や障害は機会損失や執行誤差を引き起こす可能性があります。

-

資金規模の制約:固定数量のポジションサイズはすべての口座規模に適しているとは限らず、小口座は過剰リスクに晒され、大口座は資金を十分活用できない可能性があります。

戦略の最適化方向

戦略設計と潜在リスクに基づき、以下の最適化方向が考えられます:

-

適応型パラメータ:ATR乗数や移動平均線期間などの主要パラメータを市場状況に応じて自動調整する設計にすることで、様々な市場フェーズでの適応性を向上させる。

-

スマートフィルター強化:追加の市場状態指標(市場構造、変動パターン認識、関連資産の相関など)を統合し、フィルターの精度をさらに高める。

-

動的ポジション管理:固定数量のポジションを、口座規模、現在のボラティリティ、直近の戦略成績に基づく動的計算に置き換え、よりスマートな資金管理を実現する。

-

マルチタイムフレーム確認:異なる時間軸でシグナルを検証し、取引方向がより大きな市場構造と一致することを確認し、不要な取引を削減する。

-

機械学習の統合:機械学習アルゴリズムで過去のシグナル成績を分析し、将来のシグナル成功確率を予測し、勝率の高い取引を優先実行する。

-

取引セッション管理:取引時間フィルターを追加し、低流動性または高ボラティリティの時間帯を避け、市場効率が最も高い取引ウィンドウに集中する。

-

相関フィルター:複数資産取引向けに、関連市場との相関分析を追加し、特定リスク要因への過度なエクスポージャーを回避する。

まとめ

適応型移動平均線クロス・ボラティリティ・トラッキング定量取引戦略は、高頻度取引システムとして機能が充実しており、移動平均線クロスによるシグナル発動に加え、複数の重要フィルターと精密なリスク管理ツールを組み合わせて、小幅ながら急激な価格変動を捉えるよう設計されています。本戦略の強みは、高いカスタマイズ性と完全なリスク管理フレームワークにあり、トレーダーは自身のリスク許容度や市場条件に応じて取引パラメータを細かく調整できます。

高頻度トレーダーにとって、本戦略は明確なエントリー・エグジットロジックと外部執行プラットフォームとのシームレスな統合能力を提供し、瞬息万変の市場で迅速な意思決定を実行する上で極めて重要です。ただし、本戦略を使用する際は、取引コストの累積と過度な最適化のリスクに特に注意し、実取引において戦略の堅牢性と収益性を維持する必要があります。

最終的に、本戦略はバランスの取れたアプローチを体現しています。すなわち、テクニカル指標とリスク管理ツールの力を活用しつつ、変化する市場環境に適応するための十分な柔軟性を維持するものです。慎重なパラメータ調整と継続的なモニタリングによる改善を通じて、本戦略は定量取引ポートフォリオにおいて価値ある構成要素となり得ます。

- 1