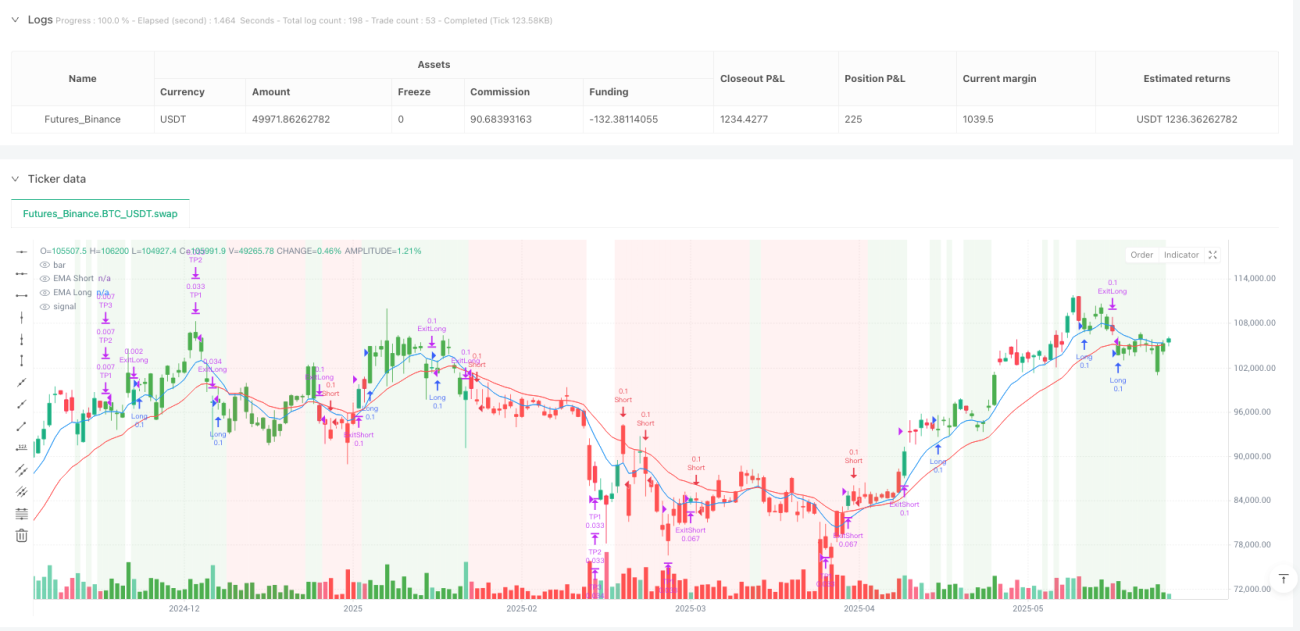

概要

マルチタイムフレーム動的ボラティリティ追跡戦略は、高速/低速指数移動平均(EMA)のクロスと相対力指数(RSI)フィルターを組み合わせた短期トレードシステムです。本戦略は、支配的な短期トレンド内での押し目・戻りエントリーを狙い、複数の確認メカニズムによりノイズ取引を低減します。コア機能には、平均真実レンジ(ATR)に基づくリスク管理、適応型トレーリングストップ、出来高ベースのストップ調整、および3段階の部分利益確定目標が含まれます。さらに、上位時間足のRSIチェックを早期警戒エグジット機構として導入し、不利なトレンドでの滞留を回避します。

戦略の原理

本戦略は、多層シグナルスタックアーキテクチャに基づき動作します:

- トレンド識別:高速EMAと低速EMAのクロスによりミクロトレンド方向を判断。高速EMAが低速EMAを上回った場合は強気トレンド、下回った場合は弱気トレンドと認識。

- モメンタム健全性フィルター:過度に延びた相場でのエントリーを防止。RSIが買われ過ぎ水準未満でのみ買いを許可し、売られ過ぎ水準超えでのみ売りを許可。

- ローソク足確認メカニズム:シグナル条件が複数連続ローソク足で成立することを要求し、市場ノイズを効果的に除去。

- エントリートリガー:確認ウィンドウ完了後のローソク足出現時に成行注文を発行。

- 初期ストップ:ATRベースのボラティリティ調整に加え、相対出来高に応じて動的に調整。

- トレーリングストップロジック:ピボットポイントとATRベースのストップを最適化して組み合わせ、利益を確定。

- 高時間足RSIモニタリング:市場背景に基づくエグジットシグナルを提供し、逆張りトレードを防止。

- 段階的利益確定目標:ATRに基づく3つの目標位置を設定し、徐々にポジションを減らす。

- トレード制限:各トレンドフェーズでの最大取引回数を制限し、過剰取引を防止。

本戦略の革新的なポイントは、複数のテクニカル指標と市場行動指標(出来高、ボラティリティなど)を有機的に組み合わせ、異なる市場環境で自動的にパラメータを調整する適応性の高い取引システムを構築した点にあります。

戦略の利点

- 高い適応性:ATRにより調整されたストップと目標は、戦略が異なる市場変動条件に適応することを可能にし、頻繁なパラメータ再最適化を不要にします。

- 多層リスク管理:初期ストップ、トレーリングストップ、部分利益確定、複数時間足RSIフィルターを組み合わせ、完全なリスク管理体制を構築。

- ノイズフィルタリングメカニズム:連続ローソク足確認要求により、偽シグナルを効果的に削減し、取引品質を向上。

- 流動性感知:出来高比率に基づいてストップ水準を調整し、低流動性環境では自動的にリスクエクスポージャーを縮小。

- トレンド成熟度の監視:トレンドの進行に伴い、許可される取引回数を自動的に削減し、トレンド後期の過剰取引を防止。

- 柔軟な利益確定メカニズム:3段階の部分利益確定戦略により、価格が有利に動いた場合に利益を確定しつつ、上昇余地を残せます。

- クロス時間足分析:高時間足のRSI監視により、より広い市場背景の視点を提供し、大規模トレンド反転時にミクロシグナルに固執することを回避。

- 実行の簡便性:PineConnector統合により、戦略の自動化を容易に実現し、人為的介入や感情の影響を軽減。

戦略のリスク

- ドローダウンリスク:多層リスク管理にもかかわらず、極端な市場状況(ギャップ、フラッシュクラッシュなど)では、予想を超えるドローダウンが発生する可能性があります。対処法はポジションサイズを適切に縮小するか、ATR倍率を増やすことです。

- パラメータ感度:EMA長さやRSI閾値などの主要パラメータは戦略のパフォーマンスに大きな影響を与えます。過度な最適化はオーバーフィッティングリスクにつながります。サンプル内最適化よりもステップフォワードテストを使用することを推奨します。

- 高頻度取引コスト:短期戦略として取引頻度が高いため、累積取引コスト(スプレッド、手数料)が実際の収益に大きく影響する可能性があります。バックテストでは実際の取引コストを考慮すべきです。

- レイテンシーリスク:PineConnectorの実行遅延(約100~300ミリ秒)により、高ボラティリティ市場ではスリッページが増加する可能性があります。ボラティリティが極端に高い、または流動性が不十分な市場では使用を推奨しません。

- ピボットポイントの再描画:分足以下の超短期チャートでは、リアルタイムのローソク足形成中にピボットポイントが再描画され、ストップの精度に影響を与える可能性があります。

- トレンド識別の遅延:EMAクロスに基づくトレンド識別には固有の遅延があり、トレンド初期に一部の値動きを逃す可能性があります。

- 過剰レバレッジリスク:ポジションサイズ乗数を大きく設定しすぎると、1回の取引で過大なリスクが生じ、口座資金を急速に消耗させる可能性があります。

戦略の最適化方向性

- 機械学習による最適化:機械学習アルゴリズムを導入し、EMAおよびRSIパラメータを動的に調整。異なる市場環境に適応的に変化させます。これにより、固定パラメータが異なる市場フェーズで適応性に欠ける問題を解決できます。

- 市場状態分類:ボラティリティクラスター分析を追加し、市場を高・中・低ボラティリティ状態に分類。各状態に対して異なる取引パラメータを採用します。これにより、変化する市場における戦略の適応性が向上します。

- 複数指標コンセンサスメカニズム:他のモメンタム・トレンド指標(MACD、ボリンジャーバンド、KDJなど)を統合し、指標コンセンサスシステムを形成。大多数の指標が合意した場合のみシグナルを生成します。これにより偽シグナルを削減できます。

- スマートタイムフィルター:市場時間帯やボラティリティパターンの分析を追加し、非効率な取引時間帯や既知の高ボラティリティイベント(重要な経済指標発表など)を回避。

- 動的部分利益確定比率:市場ボラティリティとトレンド強度に応じて、部分利益確定の割合と目標距離を自動調整。強いトレンドではより多くのポジションを保持し、弱いトレンドでは積極的に利益確定。

- ドローダウン制御強化:過去のドローダウンパターンに基づくリスク自己適応メカニズムを導入。過去の大規模ドローダウンの前兆を検知した場合、取引頻度を自動的に減らすか、ストップ距離を拡大。

- 高頻度データ強化:条件が許せば、ティックレベルデータをエントリー最適化に統合し、スリッページを低減してエントリー価格を改善。

- クロス市場相関分析:関連市場との連動分析を追加し、市場間のリード・ラグ関係を利用してシグナル品質を向上。

まとめ

マルチタイムフレーム動的ボラティリティ追跡戦略は、古典的なテクニカル分析ツールと現代の量的リスク管理手法を組み合わせた短期トレードシステムです。多層シグナルスタックアーキテクチャにより、EMAトレンド識別、RSIモメンタムフィルター、連続ローソク足確認メカニズム、ATRボラティリティ調整、マルチタイムフレーム分析を統合し、包括的な取引判断フレームワークを構築しています。本戦略の最も顕著な特徴はその適応性にあり、市場ボラティリティ、出来高、トレンド成熟度に応じて取引パラメータやリスク管理手段を自動的に調整します。

パラメータ感度、高頻度取引コスト、レイテンシーリスクなどの固有のリスクが存在しますが、適切な資金管理と継続的な最適化により、これらのリスクは効果的にコントロール可能です。今後の最適化方向性としては、主に機械学習によるパラメータ最適化、市場状態分類、複数指標コンセンサスメカニズム、動的リスク管理などが挙げられます。

短期市場でトレンド内の押し目・戻り機会を捉えたいトレーダーにとって、本戦略は取引機会の捕捉とリスク制御のバランスを取った構造化フレームワークを提供します。しかし、すべての取引戦略と同様、実際の適用に際しては、まずデモ口座で十分にテストし、個人のリスク許容度や資金規模に合わせてパラメータを適切に調整することを推奨します。

- 1