二重移動平均線クロス トレンド追従戦略と高度リスク管理システム

戦略概要

二重移動平均線クロス・トレンド追跡戦略は、テクニカル分析と包括的なリスク管理を組み合わせた定量取引システムです。本戦略の核心は、短期単純移動平均線(Fast SMA)と長期単純移動平均線(Slow SMA)のクロスシグナルを利用して市場トレンドの変化を識別し、多重リスク管理メカニズムによって資金の安全性を確保することにあります。この戦略はPine Scriptプラットフォームで実装され、多様な取引銘柄のトレンド追跡取引に適用可能です。

戦略の原理

本戦略は、2本の単純移動平均線間の相互作用関係に基づいて取引判断を行います。

-

シグナル生成メカニズム:

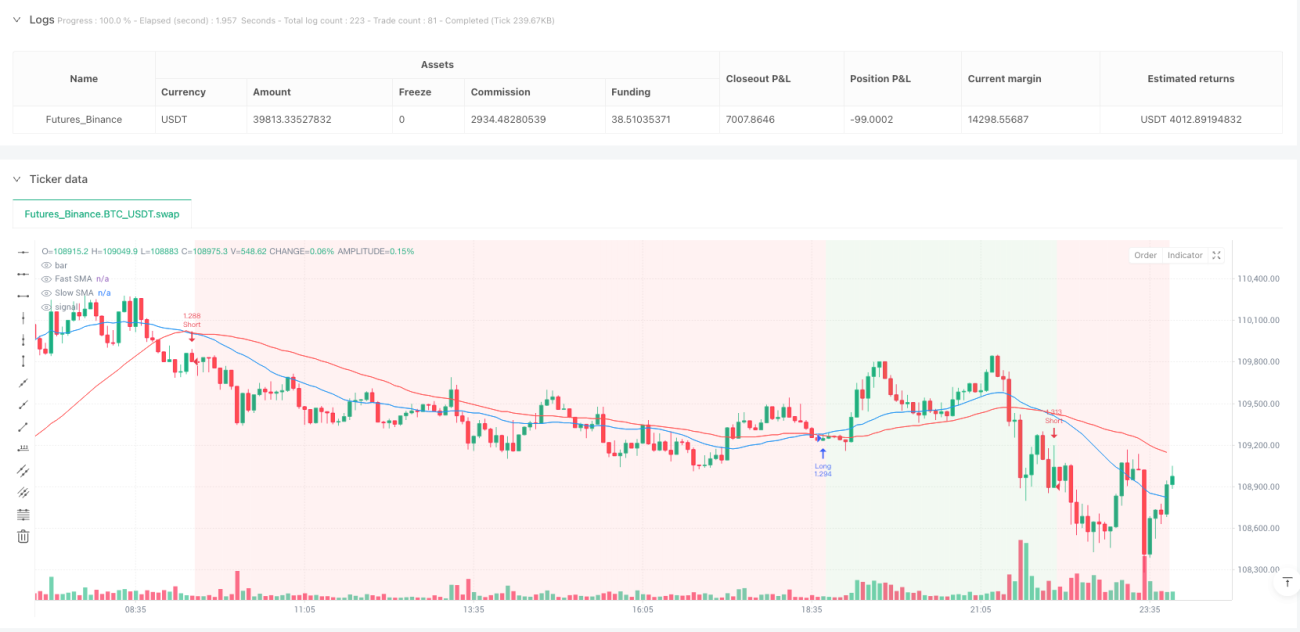

- 買いシグナル: 短期SMA(デフォルト24期間)が長期SMA(デフォルト48期間)を上抜けたとき

- 売りシグナル: 短期SMAが長期SMAを下抜けたとき

- 手仕舞いシグナル: 逆方向のクロスシグナルが発生したとき

-

執行タイミングの制御:

戦略はローソク足の終値で全ての取引判断を実行し、先見バイアス(look-ahead bias)を回避し、バックテスト結果の信頼性と再現性を確保します。 -

資金管理システム:

- 1取引あたりのリスク管理: デフォルトでは1取引あたりの最大リスクを口座総資金の2.0%に制限

- ポジションサイズの自動計算: ストップロス距離とリスク額に基づいて動的に調整し、事前設定されたリスク制限を超過しないようにする

-

多層的なリスク管理:

- 固定ストップロス: エントリー直後に固定パーセンテージのストップロス(デフォルト0.8%)を設定し、1取引あたりの損失を制限

- 利益確定目標: リスクリワード比(デフォルト2.0)に基づいて自動計算。例えば、0.8%のストップロスと2.0のリスクリワード比から1.6%の利益確定目標を算出

- 高度なトレーリングストップロス:

- 発動条件: 利益が所定のパーセンテージ(デフォルト1.0%)に達したときに発動開始

- 追跡メカニズム: 一度発動すると、ストップロス価格は最高値(買いの場合)または最安値(売りの場合)を追跡し、指定された距離(デフォルト0.5%)を維持

- 安全確保: トレーリングストップロスが初期ストップロス水準を決して下回らないようにし、資金の安全性を守りながら利益の増加を可能にする

本戦略は、移動平均線クロスを通じてトレンドを捉え、包括的なリスク管理措置により取引の安全性と持続可能性を確保します。

戦略の優位性

-

堅牢なトレンド識別メカニズム:

- 二重移動平均線クロスシステムは、古典的なトレンド追跡指標として歴史的に検証された有効性と安定性を持つ

- 短期・長期移動平均線の期間を調整することで、異なる市場環境や時間足のトレンド特性に適応可能

-

精密な資金管理:

- 口座純資産に基づく動的リスク配分により、各取引のリスクを常に管理可能な範囲に維持

- ポジションサイズは実際のストップロス距離に応じて自動調整され、過剰レバレッジや過小ポジションの問題を回避

- システムは内蔵の安全チェックメカニズムにより、極端な状況下での計算エラーを防止

-

多層的なリスク防御:

- 固定ストップロスが基本的な保護を提供し、最大損失幅を制限

- リスクリワード比に基づく利益確定目標設定により、平均収益が平均損失を上回ることを確保

- 高度なトレーリングストップロスメカニズムが実現利益を保護しつつ、トレンド継続による潜在的利益を妨げない

-

取引執行のタイミング制御:

- 全ての取引判断を厳密にローソク足終値で実行し、先見バイアスを回避

process_orders_on_close=trueパラメータを使用し、注文処理を実際の取引環境に適合- 取引ロジックは前のローソク足のシグナルに基づいて計算し、未来のデータを使用しない

-

自己適応型トレーリングストップロスシステム:

- トレーリングストップロスは取引が所定の利益水準に達した後にのみ発動され、早期のトリガーを回避

- ストップロス水準は価格変動に応じて自動調整され、一部の利益を確定しつつトレンドの継続を許容

- 内蔵の保護メカニズムにより、トレーリングストップロスが初期ストップロス水準を下回らないよう継続的なリスク保護を提供

戦略のリスク

-

トレンド識別の遅延性:

- 移動平均線は本質的に遅行指標であり、トレンド転換点での反応が不十分な場合がある

- レンジ相場では頻繁な偽シグナルが発生し、「のこぎり効果」(Whipsaw)を引き起こす可能性がある

- 緩和方法: ボラティリティ指標やトレンド強度確認などの追加フィルター条件の導入を検討

-

固定パラメータの適応性問題:

- デフォルトのSMA期間(24と48)は、市場や時間足によって有効性が異なる可能性がある

- ストップロスや利益確定目標の固定パーセンテージ設定は、全てのボラティリティ環境に適さない可能性がある

- 緩和方法: 取引銘柄の特性や過去のボラティリティに基づいてパラメータを調整するか、自己適応型パラメータメカニズムを導入することを推奨

-

トレーリングストップロスの発動タイミング:

- トレーリングストップロス発動の利益水準(デフォルト1.0%)を高く設定しすぎると、利益確定の機会を逃す可能性がある

- 低く設定しすぎると早期に発動され、潜在的利益を制限する可能性がある

- 緩和方法: 対象銘柄の平均真実レンジ(ATR)に比例してトレーリングストップロスパラメータを設定し、より自己適応的にする

-

資金管理リスク:

- ボラティリティが極めて低い銘柄では、固定パーセンテージのストップロスがポジションサイズを過大にする可能性がある

- 極端な市場条件下(ギャップやフラッシュクラッシュなど)では、所定のストップロス価格で執行できない可能性がある

- 緩和方法: 最大ポジション制限を設定するか、ボラティリティ指標(ATRなど)に基づいてリスクパラメータを動的に調整することを検討

-

技術実装の限界:

- ストップロスパーセンテージがゼロまたは負の場合の代替ロジックが、予期せぬリスクを引き起こす可能性がある

- 取引手数料やスリッページが戦略の実際のパフォーマンスに与える影響を考慮していない

- 緩和方法: エラーハンドリングロジックの改善、より多くの安全チェックの追加、バックテストへの取引コストの組み込み

戦略の最適化方向

-

シグナル生成メカニズムの最適化:

- 自己適応型移動平均線期間の導入: 市場ボラティリティに応じて短期・長期移動平均線の期間を動的に調整し、様々な市場環境への適応性を向上

- 補助確認指標の追加: 相対力指数(RSI)、ストキャスティクス、MACDなどの指標を組み合わせ、低品質シグナルをフィルタリング

- 価格構造分析の考慮: サポート/レジスタンス、価格パターン認識などの要素を統合し、シグナル品質を向上

-

リスク管理システムの強化:

- ボラティリティ適応型ストップロス: ATRなどのボラティリティ指標に基づいてストップロス距離を動的に設定し、固定パーセンテージを排除

- 段階的トレーリングストップロス戦略: 複数段階のトレーリングストップロスを実装し、利益増加に伴って追跡距離を徐々に縮小

- 最大ドローダウン制御: 口座最大ドローダウン比率に基づくリスク調整メカニズムを追加し、不利な市場環境で自動的にリスクを低減

-

エントリー最適化:

- トレンド強度フィルター: トレンド強度が一定の閾値に達した場合のみ取引シグナルを実行

- ボラティリティウィンドウフィルタリング: 適切なボラティリティ環境でのみ取引を実行し、過剰変動や低変動の市場を回避

- 最適執行価格: シグナル生成後の最適なエントリータイミングと価格水準の研究

-

バックテストと評価フレームワーク:

- 複数時間足の一貫性: 戦略が異なる時間足で一貫性と頑健性を持つことを検証

- 感応度分析: 各パラメータ変化が戦略パフォーマンスに与える影響を包括的にテストし、最も安定したパラメータ組み合わせを発見

- モンテカルロシミュレーション: 取引結果をランダム化し、戦略の確率分布と頑健性を評価

-

技術実装の向上:

- エラーハンドリングの改善: エッジケース処理を強化し、様々な市場環境で戦略が安定動作することを確保

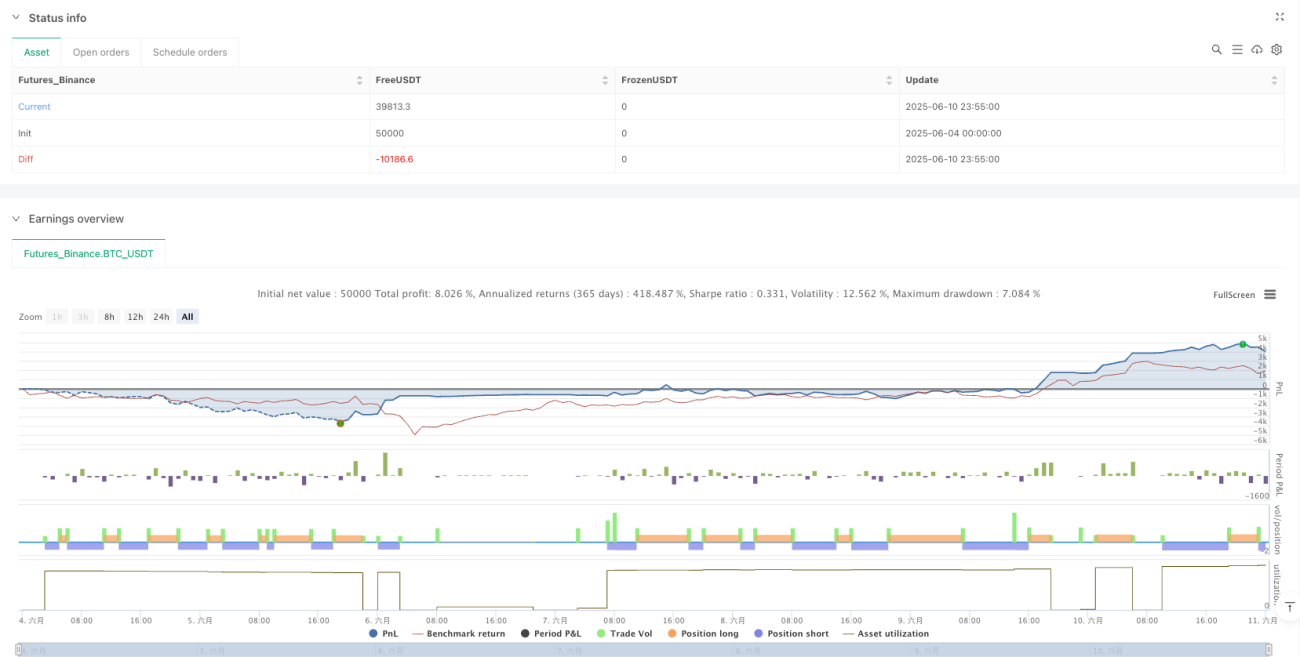

- パフォーマンス指標モニタリングの追加: シャープレシオ、最大ドローダウンなどの主要パフォーマンス指標をリアルタイムで追跡

- 戦略状態の可視化: グラフィカルインターフェースを改善し、戦略状態、ポジション、リスクレベルを直感的に表示

まとめ

二重移動平均線クロス・トレンド追跡戦略は、古典的なテクニカル分析手法と現代的なリスク管理概念を融合した完全な取引システムです。その核心的優位性は、簡潔で明確なトレンド識別メカニズムと多層的なリスク管理体制、特に緻密な資金管理と高度なトレーリングストップロスメカニズムにより、リスク調整後のリターン可能性を提供することにあります。

しかし、この戦略は移動平均線に固有の遅延性やパラメータ適応性といった課題にも直面しています。自己適応型パラメータの導入、シグナルフィルタリングメカニズムの強化、リスク管理システムの改善を通じて、戦略パフォーマンスのさらなる向上が期待できます。

全体として、これは構造が整備され、ロジックが明確な定量戦略フレームワークであり、中長期トレンド追跡システムの基盤として適しており、特に明確なトレンド特性を持つ市場に有効です。トレーダーにとって、戦略パラメータを単にコピーするよりも、そのリスク管理概念を理解し習得することが重要であり、これこそが本戦略の最も価値ある部分です。

- 1