概要

多層統計回帰トレーディング戦略は、高度な定量取引システムであり、3層の線形回帰フレームワークに統計的検証と統合ウェイト割り当てメカニズムを組み合わせたものです。この戦略は短期・中期・長期の価格動向を同時に分析し、厳格な統計的有意性テストを通じて高信頼性の方向性シグナルを生成し、厳格なリスク管理措置を実施します。戦略の核心は、複数の時間枠における線形回帰分析結果を加重統合し、過去のバックテストによる検証でシグナル品質を確保し、信頼度に応じてポジションサイズを動的に調整することにあります。

戦略の原理

本戦略の基本原理は、多層統計線形回帰分析に基づいており、主に以下の重要な要素で構成されています。

-

多層回帰エンジン: 戦略は3つのカスタマイズ可能な時間枠(短期/中期/長期)で並行して線形回帰分析を実行し、デフォルトでは各20/50/100期間です。各時間枠の傾き、R二乗値、相関係数などの統計指標を計算し、将来の価格動向を予測します。R二乗値、相関係数、傾きの絶対値がすべて既定の閾値を超えた場合のみ、回帰分析結果は統計的に有意とみなされます。

-

シグナル検証システム: 戦略は過去の予測値と実際の価格動向を比較することで予測精度を評価する、バックテスト検証メカニズムを設計しています。3つの時間枠からのシグナルは加重統合方式で統合され、短期・中期・長期シグナルに異なるウェイト(デフォルト0.4/0.35/0.25)が割り当てられます。総合信頼度スコアは、統計的強度、層間の一貫性、検証精度を組み合わせています。

-

リスク管理体制: 戦略はシグナル信頼度に応じてポジションサイズを動的に調整し(デフォルトで口座資金の50%)、1日あたりの最大損失制限(デフォルト12%)を設定し、制限に達した場合に自動的に取引を停止します。また、外国為替取引の特性を考慮し、戦略にはスプレッドスリッページとパーセンテージベースの手数料設定も含まれています。

シグナル生成ロジックでは、統合スコアの絶対値が0.5を超え、全体的な信頼度が既定の閾値(デフォルト0.75)を上回り、短期および中期の回帰が統計的に有意であり、かつ1日あたりの損失制限がトリガーされていないことが必要です。反対方向の高信頼度シグナルが出現した場合、または1日あたりの損失制限がトリガーされた場合、戦略はポジションをクローズします。

戦略の優位性

コードの詳細な分析を通じて、本戦略には以下の顕著な優位性があります。

-

多次元市場分析: 短期・中期・長期の価格動向を同時に分析することで、戦略は市場の動向を総合的に把握し、単一の時間枠による偏った判断を回避できます。

-

統計的厳密性: 戦略は厳格な統計的有意性テスト(R二乗値、相関係数、傾き閾値)を実施し、高品質な回帰分析結果のみがシグナル生成に使用されることを保証し、偽シグナルの可能性を大幅に低減します。

-

適応型ポジション管理: 戦略はシグナル信頼度に応じてポジションサイズを動的に調整し、高信頼度の場合はポジションを増やし、低信頼度の場合はリスクエクスポージャーを減らすことで、リスクとリターンのインテリジェントなバランスを実現します。

-

内蔵検証メカニズム: 過去のバックテスト検証により予測精度を評価し、シグナル品質に追加の保証層を提供し、戦略の安定性と信頼性を効果的に向上させます。

-

包括的なリスク管理: 1日あたりの最大損失制限を設定し、1日での大幅な損失を防止して口座資金の安全性を保護します。制限に達すると自動的に取引を停止し、市場環境の改善を待ちます。

-

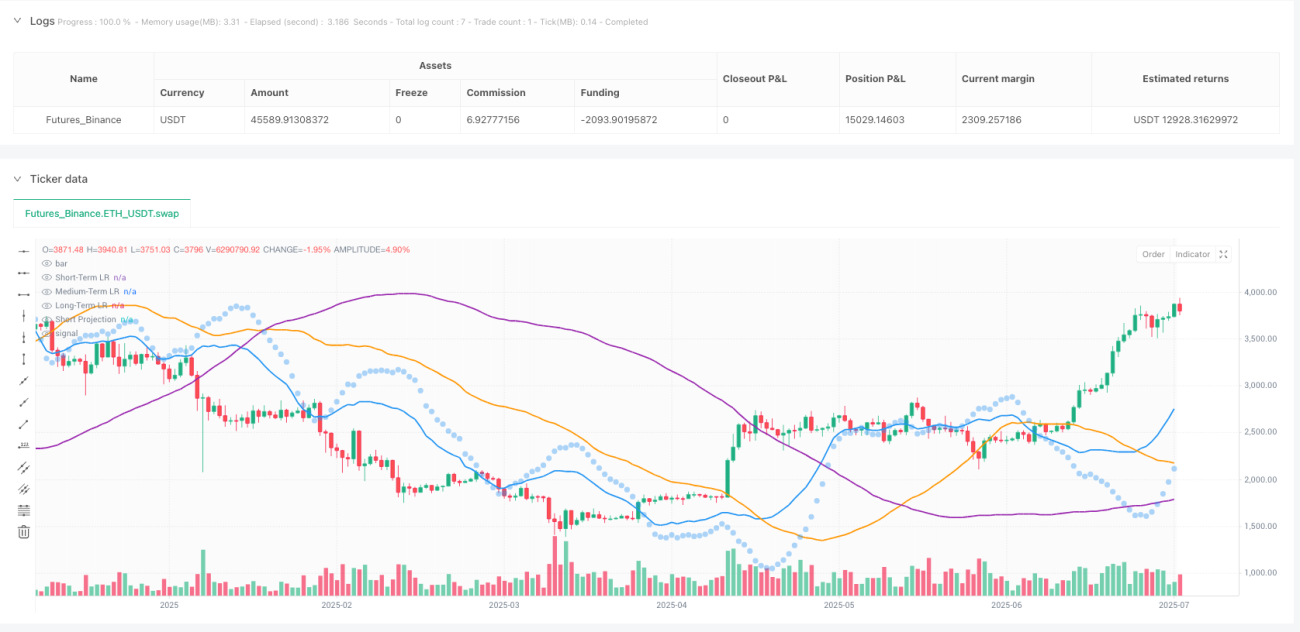

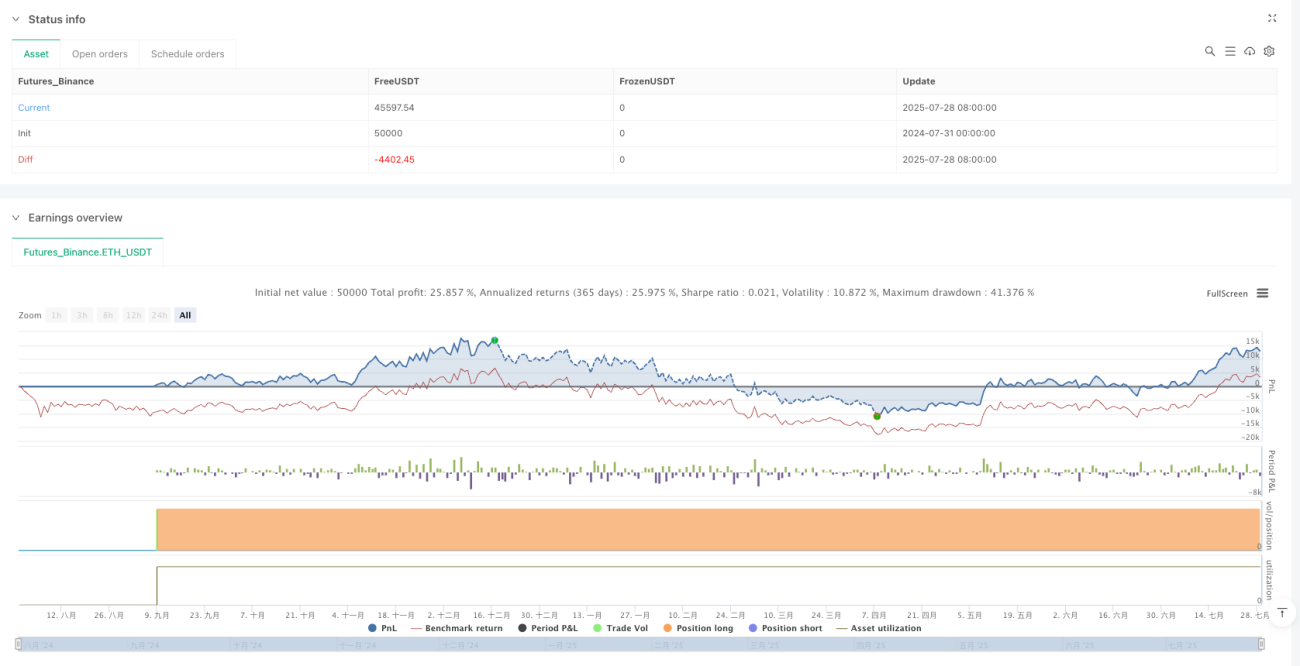

可視化意思決定サポート: 戦略はリアルタイムの回帰線チャート(3層で異なる色)、短期予測マーカー、市場バイアスの背景色表示、および包括的な統計データパネル(R二乗指標、検証スコア、損益状況)を提供し、取引判断に直感的なサポートを提供します。

戦略のリスク

本戦略は設計が優れているものの、以下の潜在的なリスクが存在します。

-

パラメータ感応性: 戦略は複数の重要なパラメータ(R二乗閾値、相関係数最小値、傾き閾値など)に依存しており、これらの設定が戦略のパフォーマンスに大きな影響を与えます。不適切なパラメータ設定は、過剰な取引や重要なシグナルの見逃しにつながる可能性があります。解決策: 過去データによるバックテストでパラメータ設定を最適化し、定期的にパラメータの有効性を再評価します。

-

市場環境の変化: 高いボラティリティや突発的なイベント時には、線形回帰の予測能力が著しく低下し、戦略のパフォーマンスが悪化する可能性があります。解決策: 市場状態認識メカニズムを追加し、非線形市場環境では自動的に調整または取引を一時停止します。

-

統計的ラグ: 線形回帰分析は本質的に遅行指標であり、急激な方向転換のある市場では十分に迅速に反応できない可能性があります。解決策: 先行指標やモメンタム指標を統合し、市場転換点に対する感度を向上させることを検討します。

-

過学習リスク: 多層統計フレームワークは過去データに過学習する可能性があり、将来の市場環境でパフォーマンスが低下する恐れがあります。解決策: フォワードテストとクロスバリデーションを実施し、戦略の頑健性と適応性を確保します。

-

計算の複雑さ: 戦略の多層回帰分析と統計的検証は多くの計算リソースを必要とし、高頻度取引環境では実行遅延が発生する可能性があります。解決策: コードの効率を最適化し、より効率的な統計計算方法の使用を検討します。

戦略の最適化方向

コード分析に基づき、本戦略は以下の方向で最適化が可能です。

-

動的時間枠適応: 現在の戦略は固定の短期/中期/長期の時間枠長を使用していますが、市場のボラティリティに応じてこれらのパラメータを自動調整することを検討できます。高ボラティリティ市場では時間枠を短縮し、低ボラティリティ市場では延長することで、戦略がさまざまな市場条件にうまく適応できるようにします。

-

予測モデルの強化: 現在の戦略は線形回帰のみを使用していますが、多項式回帰、ARIMA、機械学習モデル(ランダムフォレスト、サポートベクターマシンなど)などのより複雑なモデルを統合し、予測精度を向上させることを検討します。

-

市場環境分類: 市場環境認識モジュールを追加し、トレンド市場とレンジ相場を区別し、異なる市場環境で異なる取引ロジックとパラメータ設定を使用することで、戦略の適応性を高めます。

-

検証メカニズムの最適化: 現在のバックテスト検証は主に短期予測に基づいていますが、これを3つのすべての時間枠に拡張し、ローリングウィンドウクロスバリデーションなど、より複雑な検証方法を実装することで、検証の信頼性を向上させます。

-

高度なリスク管理: 動的ストップロス水準、ボラティリティ調整済みポジションサイズ、関連資産のリスクパリティなど、より高度なリスク管理技術を導入し、リスク調整後リターンをさらに向上させます。

-

センチメントとファンダメンタルズの統合: ボラティリティ指数、金利差、経済指標発表の影響など、市場センチメント指標やファンダメンタルズ要因をモデルに統合し、より包括的な取引判断フレームワークを構築することを検討します。

まとめ

多層統計回帰トレーディング戦略は、技術的に先進的で綿密に設計された定量取引システムです。多層線形回帰分析と厳格な統計的検証、インテリジェントなリスク管理を組み合わせ、取引判断に強固な数学的基盤を提供します。この戦略の最大の強みは、包括的な市場分析能力と厳密な統計手法にあり、短期・中期・長期の価格トレンドを同時に考慮し、統計的有意性テストを実施することで、低品質のシグナルを効果的にフィルタリングします。

戦略の統合加重メカニズムと適応型ポジション管理システムにより、シグナル品質に応じて取引判断とリスクエクスポージャーを動的に調整でき、内蔵のバックテスト検証と1日あたりの損失制限が追加の安全策を提供します。充実した可視化インターフェースと統計データパネルは、トレーダーに直感的な意思決定ツールを提供します。

本戦略にはパラメータ感応性、市場環境適応性、統計的ラグなどの潜在リスクが存在しますが、定期的なパラメータ最適化、市場環境分類、予測モデル強化などの方向での最適化により、頑健性と収益性をさらに向上させることが可能です。全体的に、これは定量金融技術と実用的な取引保証を組み合わせた高度な戦略であり、特に統計手法にある程度精通したトレーダーに適しています。

- 1