概要

本戦略は、ウィリアムズ・アリゲーター指標(Williams Alligator)と相対力指数(RSI)を組み合わせた多段階確認取引システムであり、15分足の時間足向けに設計されています。価格とアリゲーターの3本線(唇線、牙線、顎線)の位置関係、およびRSIの数値に基づいて取引シグナルを生成します。買いシグナルは4つの条件(終値が唇線より上、唇線が牙線より上、牙線が顎線より上、RSIが55より大きい)すべてを満たす必要があります。売りシグナルはその逆で、終値が唇線より下、唇線が牙線より下、牙線が顎線より下、RSIが45未満であることが条件です。本戦略には厳格なストップロスおよび利食いルールも含まれており、リスクを管理し、利益を適時に確定できるようになっています。

戦略の原理

本戦略の核心は、ウィリアムズ・アリゲーター指標とRSI指標の総合的な活用にあります。ウィリアムズ・アリゲーター指標は3本の移動平均線で構成されます。顎線(青、13期間SMA、8期間先行)、牙線(赤、8期間SMA、5期間先行)、唇線(緑、5期間SMA、3期間先行)です。この3本線の並び順と価格の突破状況により、市場のトレンドの方向性と強さを示します。

唇線が牙線より上、牙線が顎線より上にあるときは市場が上昇トレンドにあることを示し、逆に唇線が牙線より下、牙線が顎線より下にあるときは下降トレンドを示します。同時に、本戦略はRSI指標による確認も行います。RSIが55より大きい場合は買いを支持し、45未満の場合は売りを支持します。これにより、取引判断に追加の確認シグナルが得られます。

戦略実行中、システムは複数のストップロス条件を監視します。ロングポジションの場合、RSIが50を下回った、終値が牙線を下回った、または唇線が牙線を下回った場合にストップロスが発動します。ショートポジションの場合、RSIが50を上回った、終値が牙線を上回った、または唇線が牙線を上回った場合にストップロスが発動します。利食いはエントリー価格から上下2ティックに設定されています。

戦略の優位性

-

多重確認メカニズム:本戦略はエントリーに4つの条件がすべて満たされることを要求するため、偽シグナルを効果的に削減し、取引の質を向上させています。ウィリアムズ・アリゲーター指標の3本線の並びがトレンド方向を確認し、RSIの数値が勢いを確認します。

-

明確なエントリーおよびエグジットルール:戦略は明確なエントリーシグナルとエグジット条件を提供するため、主観的な判断が減り、取引プロセスがより規範的で規律正しくなります。

-

リスク管理の充実:戦略は複数のストップロス条件を設定しており、RSIに基づく反転シグナル、価格と牙線の関係変化、唇線と牙線の位置関係の変化など、多層的なリスク管理メカニズムにより、タイムリーな損切りと1回の取引における最大リスクの管理が可能です。

-

視覚的フィードバック:戦略はチャート上に買いシグナル、売りシグナル、ストップロス、利食いポイントをマークし、テーブルで各条件の充足状況をリアルタイム表示するため、取引プロセスの可視化が大幅に向上します。

-

適応性の高さ:戦略パラメータにはデフォルト設定がありますが、すべての主要パラメータを入力で調整可能なため、トレーダーはさまざまな市場環境や個人の好みに合わせて最適化できます。

戦略のリスク

-

小幅レンジ市場での頻繁な取引:市場が小幅に揉み合う場合、価格がアリゲーターラインを頻繁に上下し、RSIも境界値付近で変動するため、取引シグナルが過多になり、頻繁なエントリーとエグジットが発生し、取引コストが増加します。解決策としては、確認条件を増やすか、観察期間を延長することが挙げられます。

-

急激な相場変動時のスリッページリスク:市場で突発的な重要ニュースが発生し価格が急激に変動した場合、実際の約定価格とシグナル発生時の価格に大きな乖離が生じ、スリッページリスクが高まります。重要なデータ発表前は本戦略の使用を控えるか、一時停止することを推奨します。

-

利益目標の保守性:戦略は利食い目標を2ティックと設定していますが、これは変動の大きい市場では保守的すぎ、トレンド相場を十分に活用できない可能性があります。市場の変動に応じて利食い目標を動的に調整するか、分割決済戦略を採用することを検討できます。

-

指標の遅延性:ウィリアムズ・アリゲーター指標とRSIはどちらもある程度の遅延性を持っており、市場が急に転換する場合にタイムリーに転換点を捉えられない可能性があります。他の先行指標や価格アクション分析を補助的に活用することを推奨します。

-

パラメータ感応度:戦略のパフォーマンスはパラメータ設定、特にRSIの閾値に敏感です。異なるパラメータの組み合わせは市場環境によって大きく異なる結果をもたらすため、バックテストを通じて最適なパラメータを見つける必要があります。

戦略の最適化方向性

-

動的RSI閾値:現在の戦略は固定のRSI閾値(55および45)を使用していますが、市場のボラティリティに応じてこれらの閾値を動的に調整することを検討できます。高ボラティリティ市場ではより緩やかな閾値を、低ボラティリティ市場ではより厳しい閾値を設定することで、異なる市場環境に適応できます。

-

取引フィルターの追加:出来高確認、ボラティリティフィルター、またはトレンド強度指標を導入し、レンジ相場での弱いシグナルを除外し、明確なトレンド時のみエントリーすることで勝率を向上させます。

-

利確戦略の最適化:現在の固定2ティックの利確戦略は単純すぎるため、トレーリングストップやATR(平均真のレンジ)に基づく利確など、動的な利確戦略を導入することで、強いトレンド相場でより多くの利益を得ることができます。

-

時間フィルター:時間フィルター機能を追加し、流動性が不足していたり異常な変動が発生しやすい時間帯(寄り付き前後15分や重要データ発表時間帯など)を避けることで、不要なリスクを低減します。

-

資金管理の最適化:現在の戦略は固定の資金割合(100%)で取引していますが、市場のボラティリティや口座資産の変動に基づいてポジションサイズを動的に調整することで、より科学的な資金管理を実現できます。

まとめ

ウィリアムズ・アリゲーターとRSIを組み合わせた多段階確認取引戦略は、構造が整い、論理が明確な取引システムです。ウィリアムズ・アリゲーター指標のトレンド判断能力とRSIの勢い確認機能を統合することで、多層的な取引判断フレームワークを構築しています。本戦略の主な優位性は多重確認メカニズムと充実したリスク管理にありますが、レンジ相場でのシグナル過多、スリッページリスク、保守的な利益目標といった課題も抱えています。

RSI閾値の動的調整、取引フィルターの追加、利確戦略の最適化、時間フィルターの追加、資金管理の改善といった方向での最適化により、本戦略の安定性と収益性はさらに向上する可能性があります。全体として、実用的な価値を持つ定量取引戦略であり、テクニカル指標にある程度精通し、先物市場で安定した収益を目指すトレーダーに適しています。

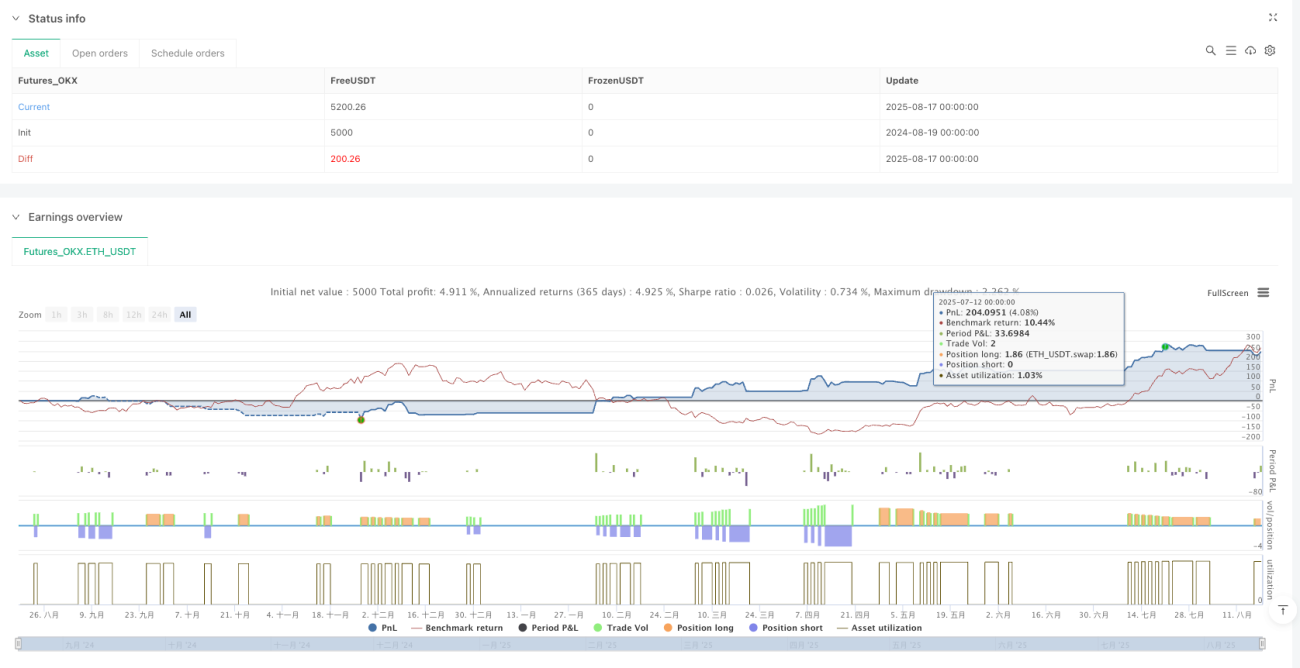

/*backtest

start: 2024-08-19 00:00:00

end: 2025-08-18 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_OKX","currency":"ETH_USDT","balance":5000}]

*/

//@version=5

strategy("Natural Gas Alligator RSI Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// =====================================- 1