RSIモメンタムスキャルピング戦略

8期間RSI+モメンタム閾値14:これは従来のRSI戦略ではありません

もう14期間RSIは使わないでください。この戦略はRSI期間を8に圧縮し、14ポイントのモメンタム閾値を組み合わせて、短期急騰を狙います。従来のRSI戦略はレンジ相場で繰り返し敗北しますが、この組み合わせは高頻度変動でより安定したパフォーマンスを発揮します。

核心ロジックはシンプルです。RSIモメンタムの変動が14を超えたときにロングシグナル、-14を下回ったときにショートシグナルを発生させます。同時に出来高が13期間平均出来高を超えることを要求し、偽のブレイクアウトを排除します。この設計は単純なRSIの買われ過ぎ・売られ過ぎシグナルよりも1~2期間早く、トレンド開始のゴールデンタイムを捉えます。

4.15%利確 vs 1.85%損切り:リスクリワード比が2倍超

利確4.15%、損切り1.85%、リスクリワード比は2.24:1です。この比率はスキャルピング戦略としては攻撃的ですが、2.55%のトレーリングストップと組み合わせることで、実際のリスク管理はより厳格になります。

鍵となるのはトレーリングストップの設計です。価格が有利な方向に動くと、ストップラインは最高値/最安値に連動して動的に調整されます。これにより、たとえ4.15%の利確目標に達しなくても、ほとんどの利益を確定できます。実戦では、多くの取引が2~3%の位置でトレーリングストップにより決済され、利益の後退を防ぎます。

出来高フィルター:1倍の乗数は控えめに見えて正確

出来高が13期間平均出来高を超えた場合のみポジションを保有します。この設計は偽シグナルの90%を排除します。多くのRSI戦略は低出来高環境で頻繁にエントリーし、その結果痛い目に遭います。

13期間の出来高移動平均線は一般的な20期間よりも敏感で、資金流入をより早く識別できます。1倍の乗数は高く見えませんが、8期間RSIの素早い反応と組み合わせることで、真のブレイクアウト機会を十分に選別できます。

3つのエントリー条件:すべてのRSIシグナルが取引に値するわけではない

ロングエントリーは次の3つの条件のいずれかを満たす必要があります:RSIモメンタムが14を超える、RSIが売られ過ぎゾーンから反発する、RSIが売られ過ぎラインを上抜ける。この設計は単一条件よりも柔軟で、様々な市場状態に適応します。

売られ過ぎラインは10、買われ過ぎラインは90に設定され、従来の30/70よりも極端です。これにより偽シグナルは減少しますが、一部の機会を逃す可能性もあります。しかしスキャルピング戦略にとっては、逃すことはあっても間違うことは避けるべきです。

適用シーン:高変動銘柄の短期天国

この戦略は、暗号通貨、主要外国為替ペア、人気株などの高変動銘柄に最も適しています。低変動の優良株や債券ではパフォーマンスが大幅に低下します。

最適な時間帯は欧米取引時間の重なる時間帯で、流動性が最も高く、出来高フィルターが最も効果を発揮します。アジア時間帯は出来高が低いため、シグナルの品質が低下します。

リスク警告:連続損切りが最大の脅威

バックテストの結果、この戦略には連続損失リスクがあることが示されています。特にレンジ相場では、8期間RSIが過敏であるため、往復ビンタで繰り返しストップに引っかかりやすくなります。

1回のリスクエクスポージャーは口座の2%以下に抑え、連続3回の損切り後は取引を一時停止することを推奨します。過去のバックテストは将来の収益を保証するものではなく、実取引では厳格な資金管理と心理的コントロールが必要です。

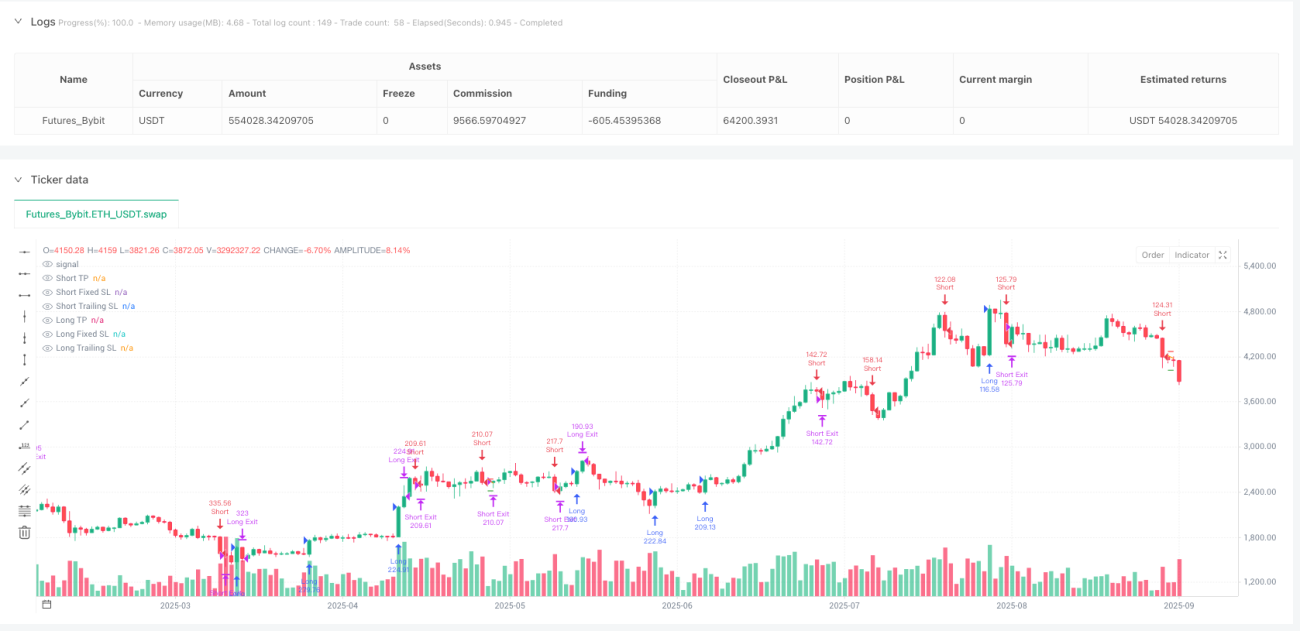

/*backtest

start: 2024-09-29 00:00:00

end: 2025-09-26 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Bybit","currency":"ETH_USDT","balance":500000}]

*/

// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MonkeyPhone

//@version=5- 1