三重共振キャッチ戦略

3つの指標が2本のローソク足内で同時にシグナルを発しなければならない。さもなければ無効

これは通常のマルチインジケーター戦略ではない。WaveTrend + Connors RSI + 線形回帰偏差の組み合わせにおいて、鍵となるのはウィンドウ同期メカニズムである。全ての買いシグナルは2本のローソク足の範囲内で出現しなければならず、単独のシグナルは無視される。この設計により、90%の偽シグナルが直接フィルタリングされる。

従来の戦略では、各インジケーターが独立して判断するためノイズが発生しやすく、あるいは同時トリガーを要求するため多くの機会を逃してしまう。この戦略はバランスを見つけている。2本のローソク足という許容ウィンドウは、シグナルの相関性を保証しつつ、過度に厳しい同期要求を回避している。

WaveTrendは-48の売られ過ぎラインに設定。標準RSIより高感度

WTの長さは10期間、売られ過ぎラインは-48、買われ過ぎラインは48に設定。このパラメーターの組み合わせは従来のRSIの30/70よりもアグレッシブであり、価格反転シグナルをより早期に捉えられる。WTの利点は、価格位置とボラティリティを組み合わせている点にあり、相場がレンジ内にある場合、単純なRSIよりも信頼性が高い。

重要なのはWTの計算方法である。(典型価格-EMA)/(0.015*偏差のEMA)。この数式は本質的にボラティリティ調整機能を備えている。市場の変動が激しくなると、分母が大きくなりWT値は比較的安定する。これにより、高ボラティリティ期間中の通常のRSIで生じる歪みを回避できる。

Connors RSIの三重検証、20/80の閾値設定に深い意味

CRSIは通常のRSIではない。価格RSI、連続上昇/下降RSI、価格変動百分位数ランクを融合させている。20の売られ過ぎ閾値は従来の30よりもアグレッシブだが、CRSIの三重検証メカニズムにより偽シグナルの確率が低下する。

6期間のRSI長さ設定はやや短めで、シグナル感度を高めることを目的としている。15分足では、6期間は約1.5時間の価格記憶に相当し、短期的な売られ過ぎを捉えつつ過度な遅延を防ぐ。このパラメーターは、BTCのような24時間取引される銘柄に特に効果的である。

線形回帰偏差LSDD、20期間でトレンド転換を捉える

LSDD = 現在価格 - 線形回帰値。LSDDが0ラインを上抜けた場合、価格が下降トレンドラインから乖離し始めたことを示す。20期間の設定は15分足で5時間をカバーし、中短期的なトレンド変化を効果的に識別できる。

このインジケーターの巧妙な点は、単純なトレンドフォローではなく、トレンドからの乖離度を測定する点にある。価格が継続的に下落した後、回帰線から上方に乖離し始めると、反発の開始を示唆することが多い。WTとCRSIの売られ過ぎシグナルと組み合わせることで、「売られ過ぎ+トレンド転換」の二重確認が形成される。

ロングのみ、30%のポジション、1倍ピラミッディング

戦略は純粋なロング、毎回資金の30%でエントリー、1回の追加ポジションを許容する。この設定は仮想通貨の長期的な上昇トレンドに適しており、ポジション管理によってリスクをコントロールする。30%の単回ポジションは十分な収益を得られる一方、単一取引の過度なリスクを回避する。

エグジット条件も同様に厳格:WT買われ過ぎ(>48)かつCRSI買われ過ぎ(>80)かつLSDDがマイナスに転じる、の3条件が同時に満たされなければならない。この設計により、トレンド取引の完全性が確保され、早期離脱を防ぐ。

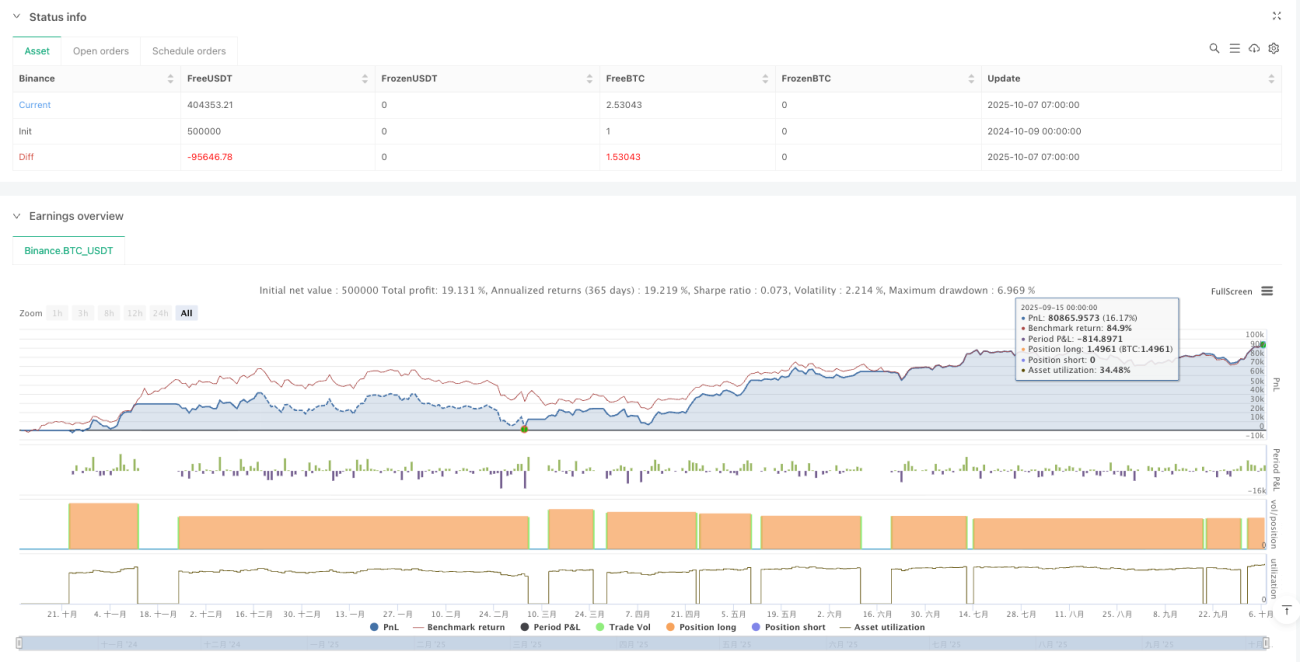

15分足BTCバックテストは良好だが、市場環境に注意

戦略はBTC 15分足でのバックテストで良好なパフォーマンスを示しているが、これは全ての市場環境で有効というわけではない。もみ合い相場では、三重確認があっても偽シグナルが多発する可能性がある。この戦略は明確なトレンド特徴を持つ市場環境に最も適している。

リスク警告:過去のパフォーマンスは将来の収益を保証するものではなく、仮想通貨市場は非常に変動が激しく、元本損失のリスクがあります。リアルトレードに入る前に、十分なペーパートレードで検証し、全体のポジションを厳格に管理することを推奨します。

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"BTC_USDT","balance":500000}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © alescha13

// WT + CRSI + Linear Regression Long-only Strategy- 1