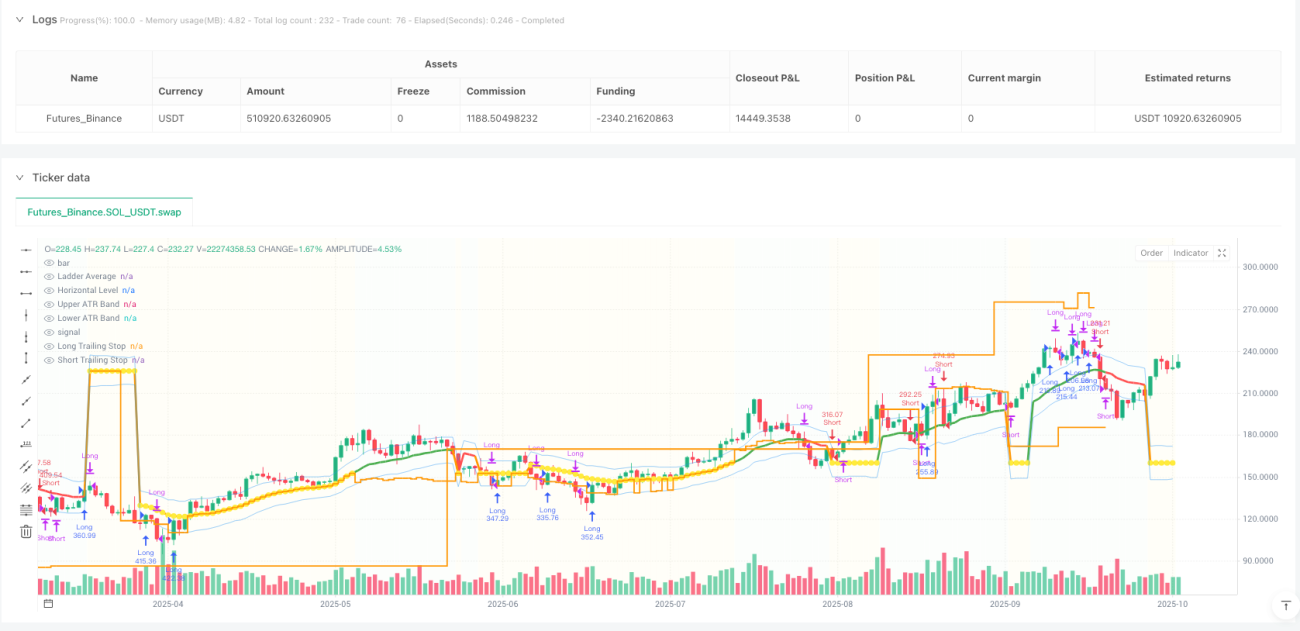

トレンド階段平均戦略:市場が横ばいのときに、いかに優雅に「寝そべる」か?

なぜ従来のトレンドフォロー戦略はレンジ相場で頻繁に「失敗」するのか?

私は定量取引の実務者として、よく次のような質問を受けます。「トレンド相場で優れたパフォーマンスを示す戦略が、なぜレンジ相場に入ると大幅なドローダウンを引き起こすのか?」

その答えは実にシンプルです。ほとんどのトレンドフォロー戦略は「トレンド強迫観念」に取り憑かれています。つまり、あらゆる市場環境で高頻度取引を維持しようと試みる一方で、市場の70%の時間は横ばいのレンジ相場であるという基本的事実を無視しているのです。

今回分析する「トレンド・ステップ平均戦略」は、まさにこの痛点に対して興味深い解決策を提示しています。トレンド相場では積極的に追跡し、レンジ相場では優雅に休息するというものです。

「ステップ平均」とは何か?この概念がどのようにトレンドフォローを再定義するのか?

従来の移動平均線戦略には致命的な欠陥があります。それは常に変化するという点です。市場が強いトレンドであろうと横ばいのレンジであろうと、移動平均線は価格変動に合わせて絶えず調整されるため、多くの偽シグナルが発生します。

一方、「ステップ平均」の核となる考え方は、特定の条件下で移動平均線を「凍結」するというものです。

具体的な実装ロジックは以下の通りです。

-

トレンド状態の検出:ADX指標を用いて市場のトレンド強度を判断

- ADX > 25:強いトレンド相場

- 移動平均線の傾き < 0.3%:横ばい相場

-

動的な移動平均線の切り替え:

- 強いトレンド時:通常通りEMA(21)を追跡

- 横ばい時:移動平均線を水平位置に「凍結」し、サポート/レジスタンスとして機能させる

この設計の巧妙な点は、戦略が異なる市場環境で異なる「性格」を示すことです。トレンド時には敏感に、レンジ時には安定して動作します。

「トレンド捕捉」システムをどのように実現するのか?

基本のステップ平均メカニズムに加え、この戦略には「トレンド捕捉」モジュールが統合されています。私が最も革新的だと考える部分です。

高速反転メカニズム:

- 決済したばかりの逆方向の強いトレンドが出現した場合

- 3期間以内に迅速に新しいポジションを構築

- 条件:ADX > 30 かつ DI+とDI-の差 > 10

この設計は、従来の戦略が抱える重要な問題を解決します。トレンド反転の初期段階でいかに迅速にポジションを調整するかという課題です。

次のようなシナリオを想像してみてください。ロングポジションを損切りで手仕舞いした直後に、市場が急激な下降トレンドに入ったとします。従来の戦略では新たなシグナル確認を待つ必要があるかもしれませんが、この「トレンド捕捉」システムは3期間以内に迅速にショートポジションを構築できます。

リスク管理:なぜ市場状態を区別するのか?

この戦略で最も学ぶべき点は、状況に応じたリスク管理メカニズムです。

レンジ相場におけるリスク管理:

- 損切りラインをステップ移動平均線付近に調整

- ATR倍率を引き下げ、損切りをタイトに

- 目標値もより保守的に設定

トレンド相場におけるリスク管理:

- 標準的なATR倍率の損切りを採用

- ステップ式トレーリングストップを有効化

- より大きな価格変動幅を許容

この設計は、重要な取引哲学を示しています。異なる市場環境には異なるリスク選好が必要であるということです。レンジ相場ではより慎重に、トレンド相場では利益に十分な余地を与える必要があります。

ステップ式トレーリングストップ:利益保護とトレンドフォローのバランスをどう取るか?

従来のトレーリングストップは往々にして機械的すぎ、タイトすぎると早期離脱を招き、緩すぎると利益を効果的に保護できません。この戦略のステップ式トレーリングストップは、よりスマートな解決策を提供します。

ステップ設定のロジック:

- ATRに基づいてステップ間隔を動的に計算

- 最大5つのステップレベルを設定

- 各ステップを突破するごとに、損切りラインを引き上げる

この設計の利点は、利益を保護しつつ、トレンドに十分な発展の余地を与える点にあります。

実際の適用で注意すべき点は?

私の実運用経験に基づくと、このタイプの戦略を使用する際には以下の点に注意が必要です。

-

パラメータ最適化の落とし穴:ADX閾値を過度に最適化しないこと。25~30の範囲の値はほとんどの市場で安定して機能します。

-

市場適合性:この戦略はボラティリティが中程度の市場に適しています。極端な変動環境ではATR倍率の調整が必要になる場合があります。

-

資金管理:特にトレンド捕捉機能を有効にする場合は、1回のポジションサイズを総資金の10%以下に抑えることを推奨します。

-

バックテストの罠:スリッページと手数料の影響に特に注意すること。特にレンジ相場での頻繁な取引において重要です。

この戦略の革新的な価値はどこにあるのか?

定量戦略の発展という観点から見ると、この戦略は重要な進化の方向性を示しています。単一ロジックからマルチ状態への適応的転換です。

従来の戦略は、一つの固定ロジックですべての市場状況に対応しようとしますが、この戦略は「状況に応じた知恵」を発揮します。

- トレンド相場では攻撃的なトレンドフォロワーのように振る舞う

- レンジ相場では保守的なレンジトレーダーのように振る舞う

この設計思想は、戦略開発者にとって重要な示唆を与えます。戦略に「市場感知」能力を持たせるべきであり、固定ロジックを盲目的に実行してはならないということです。

最後に強調しておきたいのは、どんな戦略も万能ではないということです。このステップ平均戦略は理論的にはエレガントですが、実際の適用では具体的な市場環境や個人のリスク選好に合わせて調整する必要があります。覚えておいてください。最良の戦略は、常にあなたに最も適した戦略です。

/*backtest

start: 2024-10-09 00:00:00

end: 2025-10-07 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT","balance":500000}]

*/

//@version=5

strategy("Trend Following Ladder Average Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// ═══════════════════════════════════════════════════════════════════════════════- 1