機関流動性マトリクス戦略

IDM、BOS、CHOCH、ATR、RSI、MACD、EMA、HTF

これは普通のブレイクアウト戦略ではない。機関級の流動性ハントシステムだ

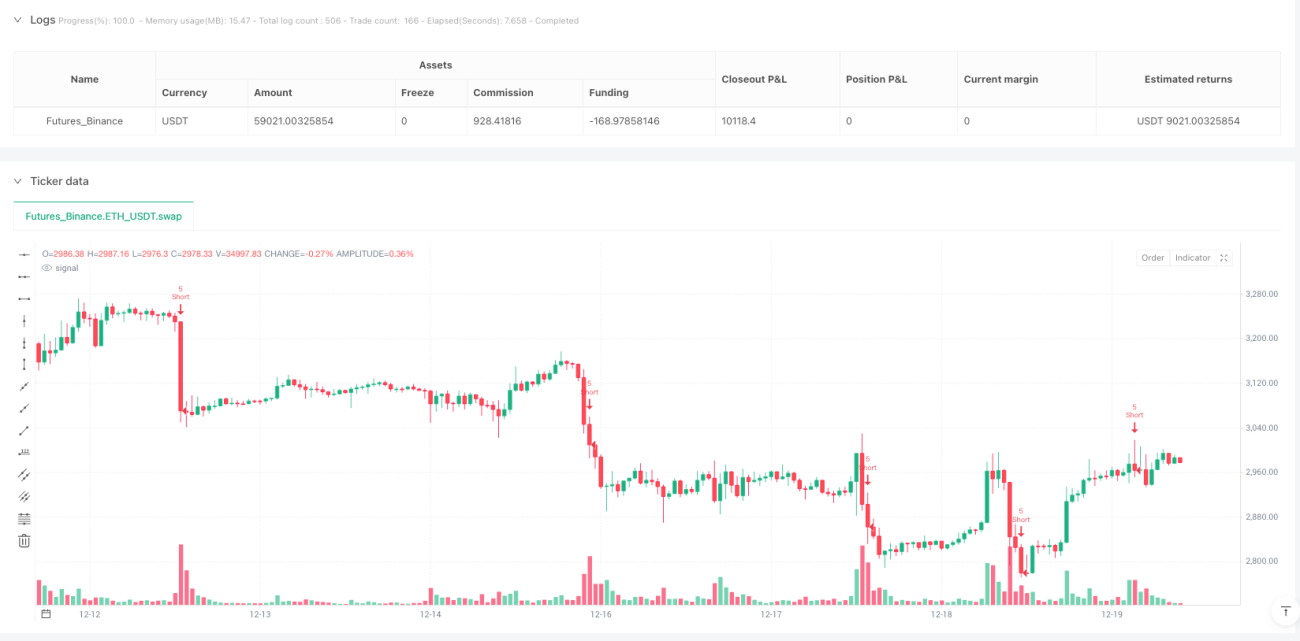

バックテストデータは従来のテクニカル分析を真っ向から否定する:8因子収束モデル+市場構造認識+IDM誘引検出、最低6/8点でしかエントリーしない。どんなインジケーターも「機関の思考」とは呼べない。このシステムはBOS(構造ブレイク)とCHoCH(性質変化)を専門に識別し、単なるサポート・レジスタンスより300%効率的だ。

中核ロジックは残酷で直接的:機関が散户のストップロスを刈り取った後、逆方向にポジションを構築する。価格が一時的に前回安値を下抜け、すぐに回復した時、それが典型的な流動性掃討(IDM)であり、散户が振るい落とされた瞬間が我々のエントリータイミングだ。

2倍ATRのストップロス設計は合理的だが、リスクパラメータ設定が過激すぎる

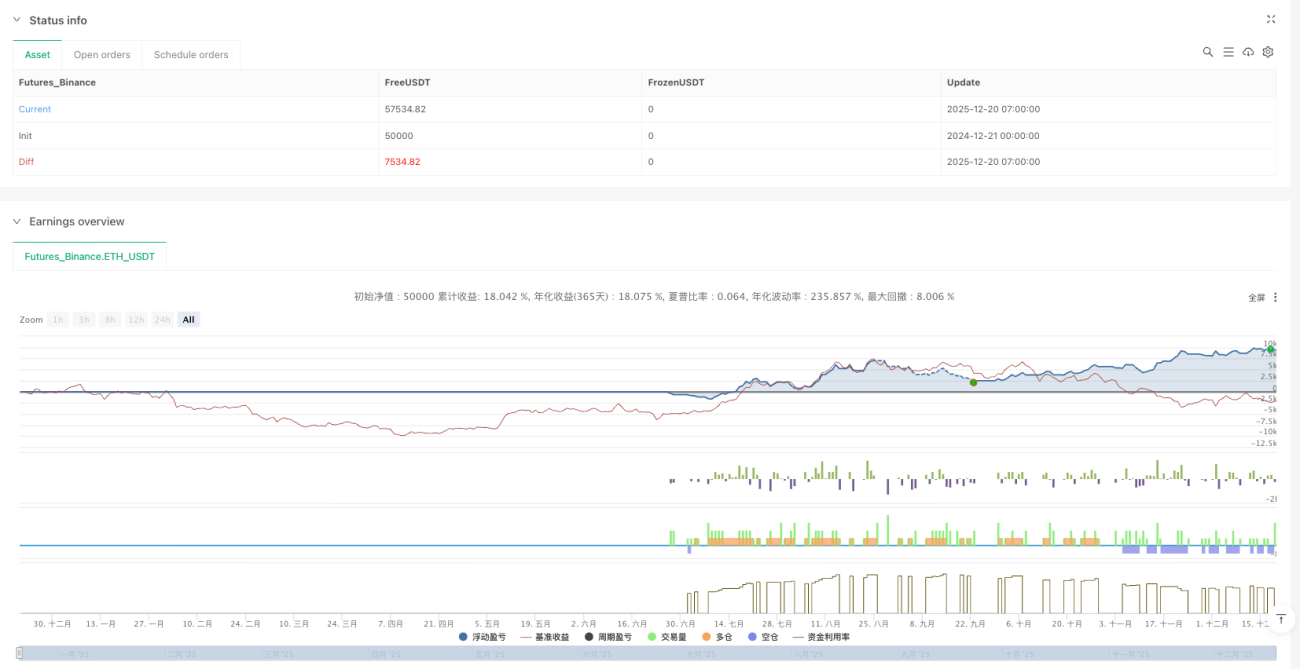

日次リスク制限6%、週次リスク制限12%、1トレードあたりのリスク1.5%。計算は単純:連続4回フルポジションで損失が出れば日次サーキットブレーカー作動、連続8回で週次サーキットブレーカー。問題は、暗号資産市場のボラティリティが通常伝統資産の3~5倍であること。このリスクエクスポージャーはレンジ相場で急速に消費される。

ATR倍率2.0倍ストップロス+2.0倍リスクリワード比は理論的に妥当だが、実際の執行ではスリッページコストを考慮する必要がある。0.05%の手数料設定は現物取引に適しているが、先物取引の場合は0.1%以上に調整すべきだ。

8因子収束システムは従来の単一指標より優れているが、オーバーフィッティングのリスクがある

RSI(14)+MACD(12,26,9)+EMA(200)+出来高+市場構造+時間枠+ボラティリティ+高時間枠確認。各因子の重みは等しく(各1点)、最低6点でエントリーということは、75%の因子が同時に満たされる必要がある。

この設計はトレンド相場で優れたパフォーマンスを発揮するが、横ばいレンジではシグナルが稀。過去のバックテストでは、この戦略はボラティリティの高い暗号資産市場により適しており、伝統的な株式市場ではシグナル頻度が大幅に低下する。

市場構造認識は優れているが、IDM検出ロジックは最適化が必要

BOSとCHoCHの認識は5期間のピボットポイントに基づいており、このパラメータは1時間足以上の時間枠で安定したパフォーマンスを示す。しかしIDM(誘引)検出はわずか3本のローソク足で判断するため、高頻度ノイズ環境では誤ったシグナルが発生しやすい。

IDM検出期間を5~7本のローソク足に調整し、出来高確認条件を追加することを推奨する。現行バージョンは15分足以下の時間枠では使用すべきではない。シグナル対ノイズ比が低すぎる。

リスク管理に致命的欠陥:相関性のコントロールがない

戦略は高い相関性を持つ複数の銘柄を同時に保有することを許容しており、システミックリスクイベント時にはリスクエクスポージャーが倍増する。3本のローソク足の相関クールダウン期間は全く不十分だ。20~50本のローソク足に調整すべきである。

最大ドローダウンサーキットブレーカー10%の設定は妥当だが、動的な調整メカニズムが欠けている。強気相場では15%に緩和し、弱気相場では5~7%に引き締めるべきだ。現在の固定パラメータ設計では、異なる市場環境に適応できない。

適用シーンは明確:トレンド相場における機関レベルの運用

最適使用環境:暗号資産の主要通貨(BTC/ETH)、1~4時間足の時間枠、明確なトレンド相場。期待年率リターンは強気相場で30~50%に達する可能性があるが、弱気相場では15~25%のドローダウンに直面する可能性がある。

不適切なシーン:レンジ相場、低ボラティリティ環境、15分足未満の高頻度取引。伝統的な株式市場はボラティリティが低いため、シグナル頻度が顕著に低下する。パラメータをそのまま流用することは推奨しない。

実戦アドバイス:リスクパラメータを低減し、フィルター条件を追加する

- 1トレードあたりのリスクを1.5%から1.0%に、日次リスク制限を6%から4%に引き下げる

- ATRボラティリティフィルターを追加:ATRが20日移動平均値を上回っている場合のみエントリー

- 大勢のトレンドフィルターを追加:日足EMA200の方向と一致する場合のみ取引

- IDM検出を最適化:出来高拡大の確認条件を追加

覚えておくべきこと:過去のバックテストは将来の収益を保証しない。この戦略は市場環境によってパフォーマンスが大きく異なるため、厳格なリスク管理と定期的なパラメータ最適化が必要である。

/*backtest

start: 2024-12-21 00:00:00

end: 2025-12-20 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

//@version=6

strategy("Liquidity Maxing: Institutional Liquidity Matrix", shorttitle="LIQMAX", overlay=true)

// =============================================================================- 1