이동평균선 기울기 교차 추세 추종 전략

개요

이 전략은 서로 다른 길이의 두 지수이동평균(EMA) 기울기의 교차를 이용하여 추세 추종 신호를 생성합니다. 기본값으로 길이 130과 400의 EMA를 사용하며, 이 두 매개변수의 조합이 효과적입니다.

빠른 EMA 기울기가 느린 EMA 기울기를 상향 돌파하고 가격이 200주기 EMA보다 높을 때 매수합니다. 빠른 EMA 기울기가 느린 EMA 기울기를 하향 돌파하고 가격이 200주기 EMA보다 낮을 때 매도합니다.

기울기 방향이 반대로 교차하면 포지션을 청산합니다.

이 전략은 비트코인과 유동성이 풍부하고 시가총액이 큰 알트코인에서 가장 우수한 성과를 보이지만, 변동성이 큰 자산에서도 잘 작동하며, 특히 이러한 자산이 자주 추세를 보일 때 효과적입니다.

4시간 시간 프레임에 가장 적합합니다.

선택적 변동성 필터도 함께 제공되며, 두 기울기 간의 차이가 특정 임계값보다 클 때만 포지션을 진입하여 가격이 횡보할 때 노이즈가 신호보다 훨씬 클 때 포지션을 여는 것을 방지합니다.

효과가 놀랍습니다. 즐기세요!

전략 원리

이 전략의 핵심은 서로 다른 길이의 두 EMA 지수이동평균의 기울기를 비교하는 것입니다.

먼저 길이 130과 400의 EMA를 계산한 후 각각의 기울기를 계산하고, 각 기울기에 대해 길이 3의 EMA를 계산하여 평활화된 기울기 곡선을 얻습니다.

빠른 EMA 기울기가 느린 EMA 기울기를 상향 돌파하면 매수 신호가 발생하고, 빠른 EMA 기울기가 느린 EMA 기울기를 하향 돌파하면 매도 신호가 발생합니다.

변동성을 필터링하기 위해 옵션으로 200주기 EMA를 추세 필터로 사용할 수 있으며, 가격이 해당 EMA보다 높을 때만 매수 신호를 고려하고, 낮을 때만 매도 신호를 고려합니다.

또한 옵션으로 변동성 필터를 사용할 수 있으며, 두 기울기 간의 차이가 사전 설정된 임계값보다 클 때만 신호를 생성하여 기울기가 교차하지만 변동성이 부족한 경우를 필터링합니다.

빠른 기울기와 느린 기울기가 반대 방향으로 교차하면 포지션을 청산하여 손익을 마감합니다.

장점 분석

-

기울기 교차를 사용하여 신호를 생성하므로 추세를 효과적으로 추적할 수 있습니다.

-

EMA 주기 매개변수 조합을 조정하여 다양한 시장 환경에 적응할 수 있습니다.

-

추세 필터는 변동성이 큰 장세에서 오도되는 것을 방지합니다.

-

변동성 필터는 가짜 신호를 걸러낼 수 있습니다.

-

규칙이 간단하고 명확하여 이해하고 구현하기 쉽습니다.

-

여러 시간 프레임에서 사용할 수 있습니다.

위험 분석

-

급격한 변동 장세에서는 빈번한 포지션 진입 및 청산이 발생할 수 있습니다.

-

EMA 주기 매개변수가 적절하지 않으면 추세 전환점을 놓칠 수 있습니다.

-

시장 환경 변화에 맞춰 매개변수 조합을 적절히 조정해야 합니다.

-

MA 시스템과 유사하게 큰 추세의 끝에서 반전 손실이 발생할 수 있습니다.

최적화 방향

-

다양한 EMA 주기 조합 매개변수를 시도하여 최적의 매개변수를 찾습니다.

-

다양한 코인 특성과 시장 환경에 따라 매개변수를 선택합니다.

-

손절 전략을 추가하여 리스크를 관리하는 것을 고려할 수 있습니다.

-

EMA 주기 매개변수를 동적으로 조정하는 것을 고려할 수 있습니다.

-

다양한 변동성 임계값 매개변수를 시도합니다.

-

다양한 시간 프레임에서의 효과를 테스트합니다.

요약

이 전략은 전체적으로 명확하고 이해하기 쉬우며, EMA 기울기 교차를 사용하여 신호를 생성하므로 추세를 효과적으로 추적할 수 있습니다. 추세 필터와 변동성 필터를 함께 사용하면 노이즈 거래를 줄일 수 있습니다. EMA 주기 매개변수 조합을 조정하여 다양한 시장 환경에 적응할 수 있습니다. 전반적으로 실전 테스트와 최적화에 가치가 있는 간단하고 실용적인 추세 추종 전략입니다.

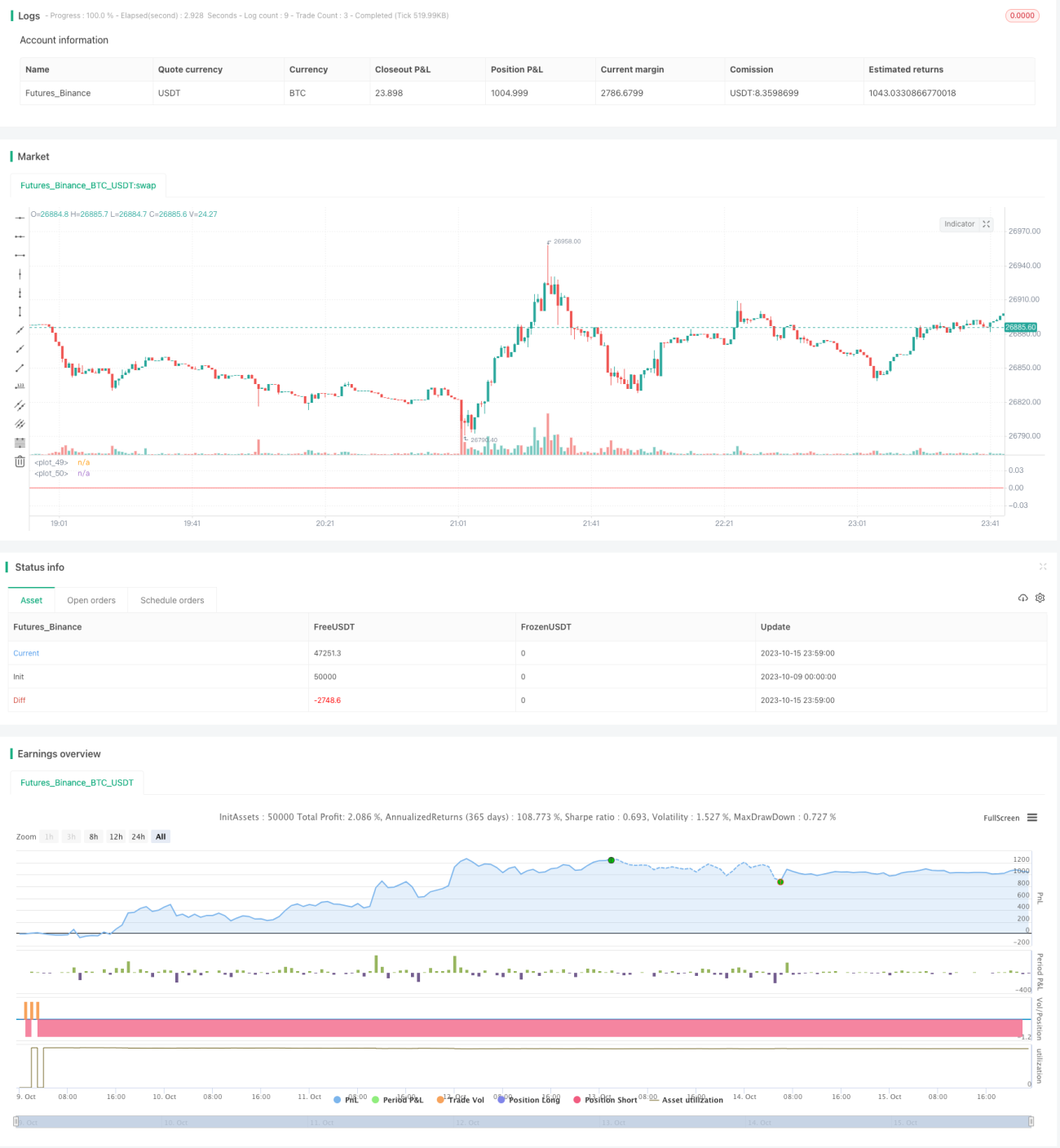

/*backtest

start: 2023-10-09 00:00:00

end: 2023-10-16 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// strategy(title="Slopes",initial_capital=1000, default_qty_type=strategy.percent_of_equity, commission_type=strategy.commission.percent, commission_value=0.06, slippage = 2, default_qty_value=30, overlay=false)

//definizione input- 1