일반화된 지지/저항 기반 반전 거래 전략

개요

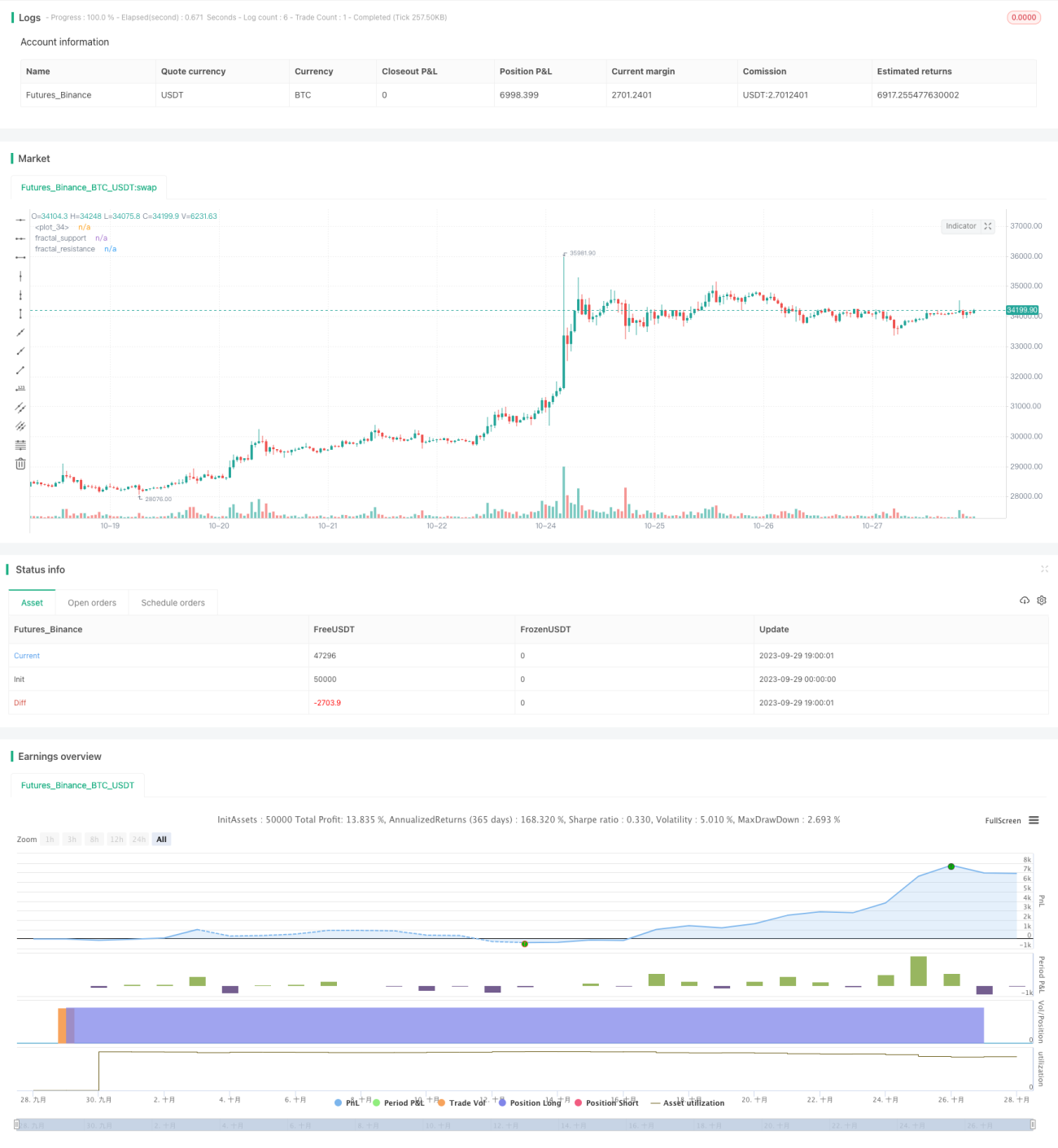

본 전략은 지표 다중 요인을 기반으로 역추세 매매(반전 거래)를 수행하며, 동시에 목표 이익 지점을 설정합니다. 다중 요인의 핵심은 거래량 기반의 확장된 형태인 '일반 지지/저항'으로, 높은 거래량과 변동성을 가진 종목에 적합합니다. 전략의 장점은 중단기 추세 반전 기회를 포착하여 빠르게 이익을 얻을 수 있다는 점이지만, 반대로 물릴 위험도 존재합니다.

전략 원리

-

거래량 기반 '일반 지지/저항'을 통한 다중 요인 식별

-

캔들 패턴을 사용하여 고전적 지지/저항을 식별하고, 큰 거래량으로 거짓 돌파를 필터링합니다.

-

일반 지지/저항은 고전적 패턴보다 더 포괄적입니다.

-

일반 지지 돌파는 상승 요인 신호, 일반 저항 돌파는 하락 요인 신호입니다.

-

-

역추세 매매

-

요인 신호 발생 후 반대 방향으로 거래합니다.

-

이미 포지션을 보유 중인 경우, 반대 방향으로 포지션을 줄이거나 반대 방향으로 새 포지션을 오픈합니다.

-

-

목표 이익 설정

-

ATR을 기반으로 손절매를 설정합니다.

-

1R/2R/3R 등 여러 목표 이익 지점을 설정합니다.

-

각 목표 이익에 도달하면 분할 청산합니다.

-

장점 분석

-

중단기 큰 폭의 반전 포착 가능

지지/저항 돌파는 강력한 추세 반전 신호로 어느 정도 신뢰성이 있으며, 중단기 큰 폭의 반전을 포착할 수 있습니다.

-

빠른 수익 실현, 적은 하락

손절매와 다단계 목표 이익 설정을 통해 빠르게 수익을 실현하고 종목별 하락 폭을 제한할 수 있습니다.

-

대규모 기관 자금이 유입되고 변동성이 큰 종목에 적합

이 전략은 거래량 지표에 의존하므로 충분한 기관 자금 유입이 추세를 뒷받침해야 하며, 수익을 내기 위한 일정한 변동 폭이 필요합니다.

위험 분석

-

횡보장에 갇힐 위험

횡보장에서 손절 후 반대 방향 진입을 반복하면 자주 물릴 수 있습니다.

-

지지/저항 실패 위험

일반 지지/저항은 절대적으로 신뢰할 수 없으며, 실패 테스트 후 반전될 확률이 있습니다.

-

단방향 포지션 위험

순수 역추세 전략으로 추세 추종을 고려하지 않아 큰 방향성 기회를 놓칠 수 있습니다.

-

리스크 관리 측면

-

역추세 매매의 요인 조건을 적절히 완화하여 모든 돌파마다 반대 방향으로 거래하지 않아도 됩니다.

-

거래량-가격 다이버전스 등 다른 지표로 필터링할 수 있습니다.

-

손절매 전략을 최적화하여 물릴 확률을 낮출 수 있습니다.

-

최적화 방향

-

파라미터 최적화

일반 지지/저항의 파라미터를 최적화하여 더 신뢰할 수 있는 요인을 식별합니다.

-

수익 전략 최적화

더 많은 목표 이익 단계를 추가하거나 비고정 목표 이익을 사용할 수 있습니다.

-

손절매 전략 최적화

ATR 파라미터를 조정하거나 변동성 기반 손절매를 사용하여 불필요한 급격한 손절로 인한 거래 비용을 줄입니다.

-

추세 및 기타 요인 결합

이동평균선 등 추세 판단 지표를 도입하여 추세와 심하게 반대되는 것을 피하고, 보조 요인을 추가할 수 있습니다.

요약

본 전략의 핵심은 역추세 매매를 통해 중단기 큰 변동을 포착하는 데 있습니다. 전략의 아이디어는 간단하고 직접적이며, 파라미터 조정을 통해 실전에서 좋은 결과를 얻을 수 있습니다. 그러나 역추세 전략은 공격적이어서 일정 하락과 물릴 위험이 있으므로, 손절매 및 수익 전략을 추가로 최적화하고 추세 판단을 적절히 결합하여 불필요한 손실을 줄여야 합니다.

- 1