소수 진동 기반 거래 전략

개요

해당 전략은 소수 오실레이터(Prime Number Oscillator) 지표를 사용하여 시장 추세를 판단하고, 이를 기반으로 롱/숏 포지션을 구축합니다. 소수 오실레이터는 가격 근처의 가장 가까운 소수와 가격의 차이를 계산하며, 양수는 상승 추세, 음수는 하락 추세를 나타냅니다. 이 전략은 가격 변동 속에 숨겨진 추세 정보를 포착할 수 있어 돌파 거래에 지침을 제공합니다.

전략 원리

이 전략은 먼저 PrimeNumberOscillator 함수를 정의하며, 매개변수로 가격과 allowedPercent를 받습니다. 이 함수는 가격을 기준으로 allowedPercent 범위 내에서 가장 가까운 소수를 찾아 두 값의 차이를 반환합니다. 차이가 0보다 크면 상승 추세, 0보다 작으면 하락 추세를 나타냅니다.

그런 다음 전략 내에서 PrimeNumberOscillator 함수를 호출하여 xPNO 값을 계산합니다. xPNO의 양수/음수에 따라 포지션 방향을 판단하고, reverseFactor를 곱하여 최종 거래 방향을 결정합니다. 이 거래 방향에 따라 롱 또는 숏 포지션을 오픈합니다.

이 전략은 주로 소수 오실레이터 지표에 의존하여 추세 방향을 판단합니다. 지표 자체는 다소 거칠기 때문에 다른 요소와 결합하여 거래 신호를 검증해야 합니다. 하지만 수학적 원리에 기반하여 어느 정도 객관적인 지침을 제공할 수 있습니다.

장점 분석

- 수학적 원리에 기반하여 비교적 객관적입니다.

- 변동 속에 숨겨진 추세를 식별할 수 있습니다.

- 매개변수 조정이 유연하여 민감도를 자유롭게 설정할 수 있습니다.

- 구현이 간단하고 이해 및 최적화가 쉽습니다.

위험 분석

- 소수 오실레이터 지표 자체가 다소 거칠어 여러 번 오판할 가능성이 있습니다.

- 다른 기술 지표와 결합하여 검증해야 하며, 단독으로 사용할 수 없습니다.

- 매개변수를 신중하게 선택해야 하며, 너무 크거나 작으면 모두 무용지물이 됩니다.

- 거래 빈도가 너무 높을 수 있으므로 포지션 규모를 통제해야 합니다.

최적화 방향

- 이동 평균, 과매수/과매도 등의 지표를 결합하여 신호를 필터링할 수 있습니다.

- 손절매 전략을 추가하여 단일 손실을 줄일 수 있습니다.

- 시장 상황에 따라

allowedPercent매개변수를 동적으로 조정할 수 있습니다. - 변동성 등의 지표를 사용하여 포지션 크기를 통제하는 포지션 관리를 최적화할 수 있습니다.

요약

이 전략은 소수 오실레이터 원리를 기반으로 추세 방향을 판단하며, 구현이 간단하고 논리가 명확합니다. 그러나 소수 오실레이터 자체에는 일정한 한계가 있으므로 신중하게 사용해야 합니다. 다른 기술 지표와 조합하여 신호를 검증하고 거래 위험을 통제할 수 있습니다. 이 전략은 수학적 거래 전략의 대표적인 예시로, 학습과 연구에 있어 참고 가치가 있습니다.

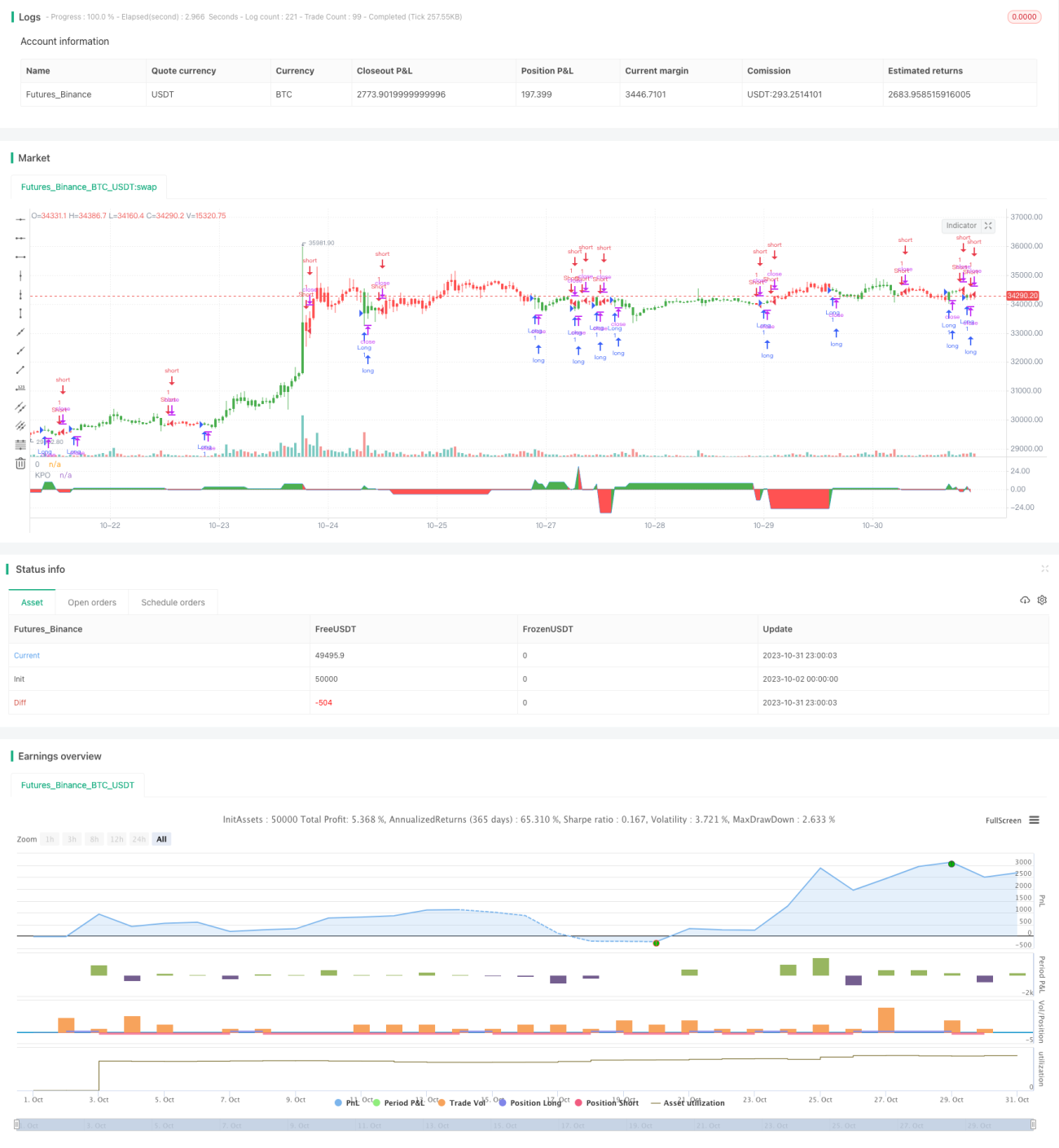

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 29/03/2018

// Determining market trends has become a science even though a high number or people - 1