추세 돌파 이동평균선 추적 전략

개요

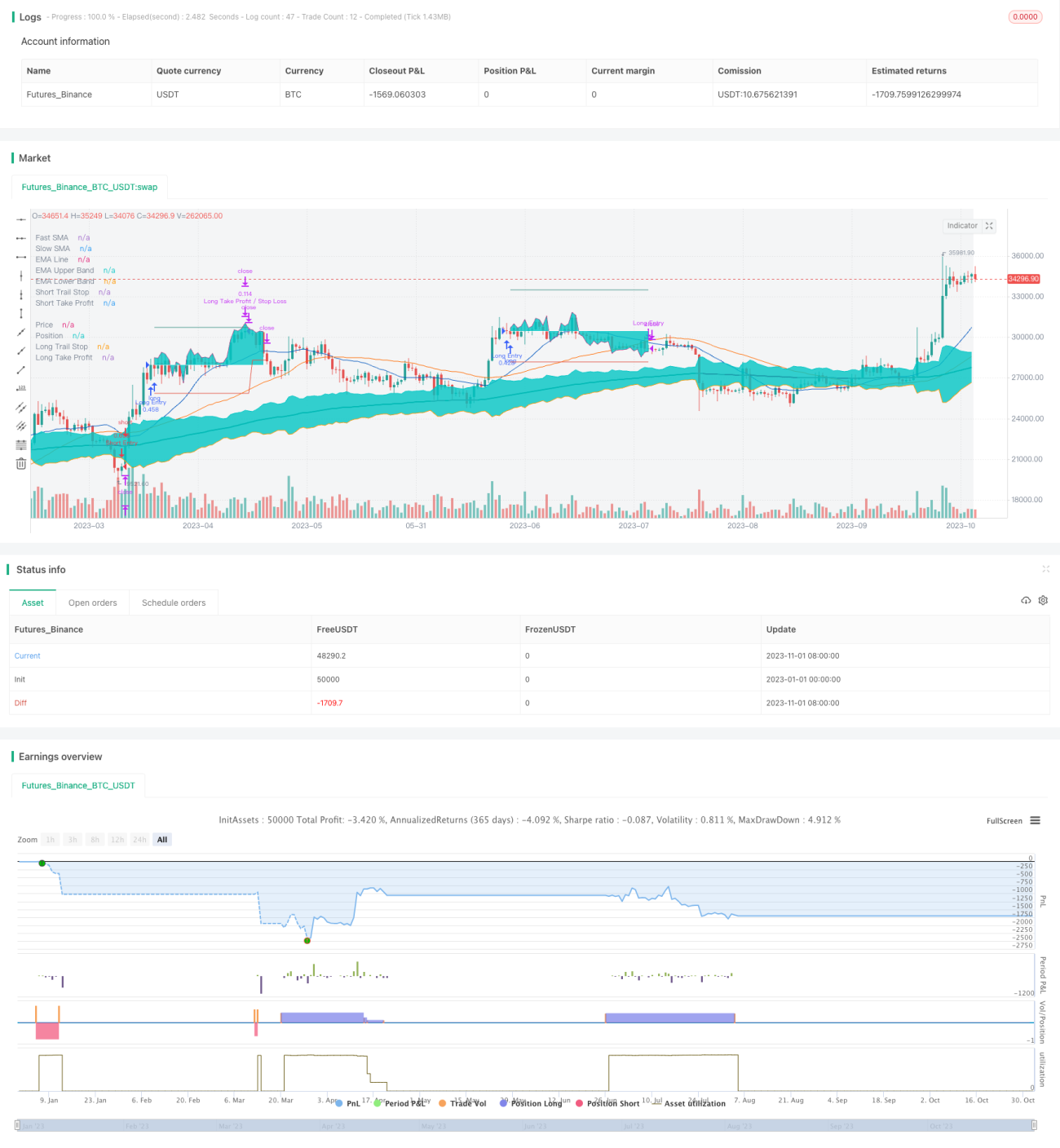

이 전략은 단순이동평균선의 골든크로스와 데드크로스를 활용하여 추세 방향을 판단하고, 추세 시작 시점에 전량 매수 또는 매도 포지션을 진입한 후 손절매와 이익실현 주문을 설정하여 리스크를 관리합니다. 포지션 진입 후에는 이동평균선을 이용해 지속적으로 추세를 추적하며, 추세가 반전될 때 신속히 손절매합니다. 이 전략은 손절매, 이익실현, 포지션 관리 모듈을 설정할 수 있어 다양한 상품에 유연하게 적용할 수 있습니다.

전략 원리

이 전략은 주로 단순이동평균선의 골든크로스와 데드크로스를 활용하여 추세의 시작과 종료를 판단합니다. 먼저 빠른선 SMA(예: 21일선)와 느린선 SMA(예: 49일선)의 관계를 통해 추세 방향을 결정합니다. 빠른선이 느린선을 하향 상승 돌파하면 상승 추세가 시작되었다고 판단하여 해당 시점에 매수 포지션을 진입합니다. 반대로 빠른선이 느린선을 상향 하락 돌파하면 하락 추세가 시작되었다고 판단하여 해당 시점에 매도 포지션을 진입합니다.

포지션 진입 후에는 가격과 SMA의 관계를 실시간으로 모니터링합니다. 가격이 위에서 아래로 SMA를 하향 돌파하면 상승 추세가 종료되었다고 판단하여 매수 포지션을 청산하고, 가격이 아래에서 위로 SMA를 상향 돌파하면 하락 추세가 종료되었다고 판단하여 매도 포지션을 청산합니다.

리스크 관리를 위해 포지션 진입 시 동시에 손절매 주문과 이익실현 주문을 설정합니다. 손절매 거리는 ATR을 기준으로 설정하고, 이익실현 거리는 백분율 또는 ATR 기준으로 선택할 수 있습니다. 포지션 진입 후 손절매 주문은 가격을 실시간으로 추적하여 추세 추적 효과를 냅니다. 이익실현 주문에 도달하면 일부 포지션을 청산하고 나머지 포지션은 계속 추적하며 최종적으로 전량 청산됩니다.

이 전략은 포지션 관리 모듈도 포함하여 각 거래의 자금 사용률을 제한함으로써 개별 거래의 리스크 노출을 통제합니다. 또한 최대 손실폭 설정을 통해 전략 전체 리스크를 관리할 수 있습니다.

전략 장점

- 이동평균선 비교를 통해 추세 방향을 판단하여 원리가 간단하고 이해하기 쉬움

- 포지션 진입 후 손절매를 실시간 추적하여 대부분의 수익을 확보할 수 있음

- 설정 가능한 손절매 및 이익실현 방식으로 다양한 상품에 맞게 조정 가능

- 개별 거래 리스크를 통제하여 전량 거래하지 않음

- 최대 손실폭 설정으로 전략 전체 손실 제한 가능

리스크 및 해결 방안

- 이중 이동평균선 교차는 일정한 지연성을 가지므로 추세 시작의 최적 진입 시점을 놓칠 수 있음

- 다양한 주기의 이동평균선 조합을 테스트하기 위해 매개변수를 반복 조정해야 함

- 이동평균선 교차는 일정한 오보율을 가지며 진입 정확도가 100%에 도달하지 않음

- 추적 손절매가 쉽게 돌파되어 모든 수익을 확보할 수 없음

- 적절히 넉넉한 손절매 거리를 설정하여 가격에 일정한 되돌림 공간을 부여해야 함

- 최대 손실폭 제한이 지나치게 보수적일 경우 상승 기회를 잃을 수 있음

- 최대 손실폭 비율을 적절히 완화하여 전략에 더 많은 오류 허용 공간을 제공해야 함

최적화 방향

- 다양한 매개변수 조합을 시도하여 최적의 이동평균선 주기 선택

- 추세 강도 지표를 추가하여 진입 정확도 향상

- 손절매 전략을 최적화하여 추세 내에서 가능한 한 추세 추종

- 다양한 이익실현 전략을 테스트하여 최적의 이익실현 지점 선택

- 포지션 관리 방안 최적화로 자금 효율성 향상

- 최대 손실폭 설정 조정으로 수익과 리스크 균형

요약

이 전략은 전반적으로 초보자에게 매우 적합한 입문 전략으로, 원리가 간단하고 이해 및 습득이 쉽습니다. 동시에 적절한 리스크 관리 능력을 갖추어 대규모 손실 확률을 줄일 수 있습니다. 매개변수 최적화를 통해 좋은 효과를 얻을 수 있습니다. 그러나 본질적인 한계로 인해 고도로 정밀한 운용은 불가능합니다. 초보자의 연습용 전략으로 사용하기를 권장하며, 높은 효율성과 높은 승률을 추구하는 트레이더에게는 적합하지 않습니다. 더 나은 거래 성과를 원한다면 더 강력한 예측 능력을 가진 전략을 찾아야 합니다.

/*backtest

start: 2023-01-01 00:00:00

end: 2023-11-02 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//

// ▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒▒

// ------------------------------------------------------------------------------ 1