개요

초일 전략은 초일 지표를 기반으로 거래 결정을 내리는 추세 추종 전략입니다. 이 전략은 초일 지표의 전환선, 기준선 및 구름대 관계를 활용하여 현재 추세 방향을 판단하고, 가격의 되돌림을 이용하여 진입합니다.

초일 전략은 주로 중장기 추세 거래에 적합하며, 큰 추세에서 수익을 낼 수 있습니다. 또한 이 전략은 강력한 추세 식별 능력을 가지고 있습니다.

전략 원리

초일 전략은 다음 요소들을 판단하여 거래 방향을 결정합니다:

-

전환선과 기준선의 관계: 전환선이 위에 있을 때 상승, 아래에 있을 때 하락으로 판단

-

구름대의 색상: 구름대가 녹색일 때 상승, 빨간색일 때 하락으로 판단

-

가격 되돌림: 가격이 전환선과 기준선 밖으로 되돌려져야 진입 가능

구체적으로, 전략의 거래 신호는 다음과 같습니다:

매수 신호:

- 전환선이 기준선보다 높음

- 가격이 전환선과 기준선보다 높음

- 전환선과 기준선이 구름대보다 높음

- 가격이 전환선과 기준선 아래로 되돌려짐

매도 신호:

- 전환선이 기준선보다 낮음

- 가격이 전환선과 기준선보다 낮음

- 전환선과 기준선이 구름대보다 낮음

- 가격이 전환선과 기준선 위로 되돌려짐

매수/매도 신호가 동시에 충족되면 포지션 상태에 따라 진입합니다.

장점 분석

초일 전략은 다음과 같은 장점을 가지고 있습니다:

-

초일 지표 조합을 사용하여 추세 방향을 판단하므로 정확도가 높음

-

전환선과 기준선이 중단기 추세를 명확히 판단하고, 구름대가 장기 추세를 판단함

-

조건이 가격을 전환선으로 되돌리도록 요구하여 허위 돌파로 인한 손실을 방지함

-

위험 관리는 최근 기간 내 최고/최저 가격을 기준으로 손절매를 설정하여 개별 손실을 효과적으로 통제함

-

손익비가 합리적이며 안정적인 수익을 추구함

-

다양한 주기에 적용 가능하며 중장기 추세 거래에 적합함

-

전략 개념이 명확하고 이해하기 쉬우며 매개변수 최적화 여지가 큼

-

다양한 시장 환경에서 효과적으로 작동함

위험 분석

초일 전략은 다음과 같은 위험도 존재합니다:

-

횡보장에서는 손절매가 자주 발생하여 수익성에 영향을 줄 수 있음

-

추세가 급변할 때 신속하게 포지션을 반전시키지 못해 손실이 발생할 수 있음

-

설정된 손익비가 모든 상품에 적합하지 않으며, 대상별로 매개변수 조정이 필요함

-

구름대 돌파 후 상승 여력이 제한적일 때 수익이 제한될 수 있음

-

지표 매개변수를 반복적으로 테스트하고 최적화해야 하며, 매개변수 변경이 잦은 상품에는 부적합함

다음 방법으로 위험을 줄일 수 있습니다:

-

매개변수를 최적화하여 다양한 주기와 상품 특성에 더 부합하도록 함

-

다른 지표를 결합하여 진입 신호를 필터링하고 횡보장에서의 허위 돌파를 방지함

-

손절매 위치를 동적으로 조정하여 손절매 발생 확률을 낮춤

-

다양한 손익비 설정을 테스트함

-

차트 패턴 등을 사용하여 추세 신호 강도를 판단함

최적화 방향

초일 전략은 다음 측면에서 최적화할 수 있습니다:

-

전환선과 기준선 매개변수를 최적화하여 거래 대상 상품의 특성에 더 적합하게 함

-

구름대 매개변수를 최적화하여 장기 추세 판단의 정확성을 높임

-

손절매 알고리즘을 최적화, 예를 들어 ATR 기준 손절매 또는 동적 손절매 도입

-

다른 지표와 결합하여 신호 필터링, 더 많은 필터 조건을 구성하여 잘못된 진입 확률을 낮춤

-

손익비 설정을 최적화하여 다양한 상품과 주기에서 전략의 특성에 맞춤

-

마틴게일 방식으로 포지션을 관리하여 다양한 시장 변동 빈도에 적응

-

머신러닝 방법을 사용하여 매개변수를 최적화하고 더 높은 안정성 달성

-

다양한 거래 시간대를 설정하여 야간장과 주간장의 시장 특성에 맞게 조정

요약

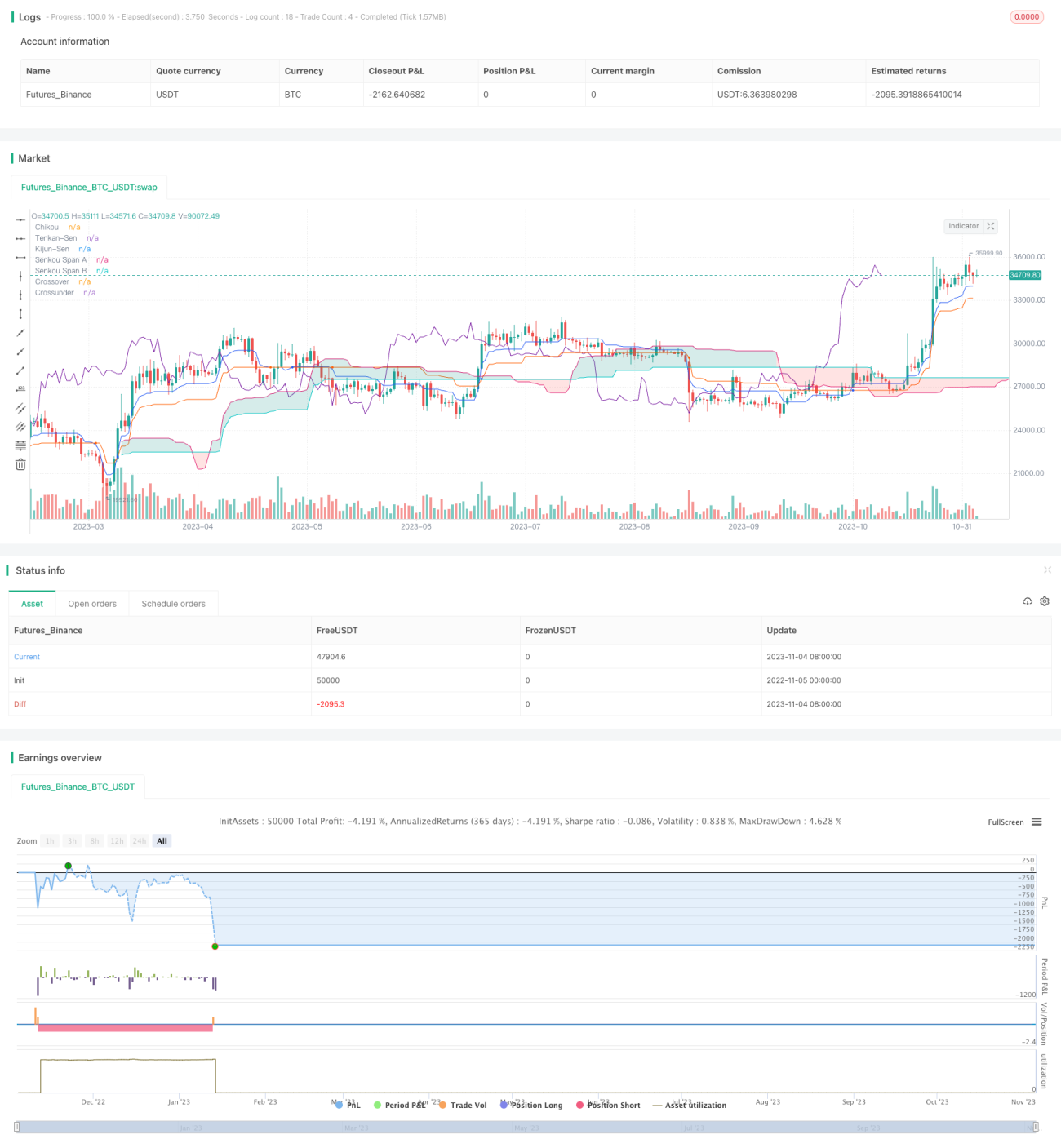

초일 전략은 전반적으로 중장기 추세 거래에 매우 적합한 전략입니다. 초일 지표를 활용한 추세 방향 판단의 장점이 뚜렷하며, 가격 되돌림을 결합한 진입은 잘못된 진입을 효과적으로 방지합니다. 매개변수 설정 최적화를 통해 더 많은 상품과 주기에서 안정적인 수익을 낼 수 있습니다. 이 전략은 이해하기 쉬우면서도 최적화 여지가 커서 전략 연구 및 학습의 기초 전략 중 하나로 적합합니다.

/*backtest

start: 2022-11-05 00:00:00

end: 2023-11-05 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Strategy based on the the SuperIchi indicator.

//

// Strategy was designed for the purpose of back testing.

// See strategy documentation for info on trade entry logic.- 1