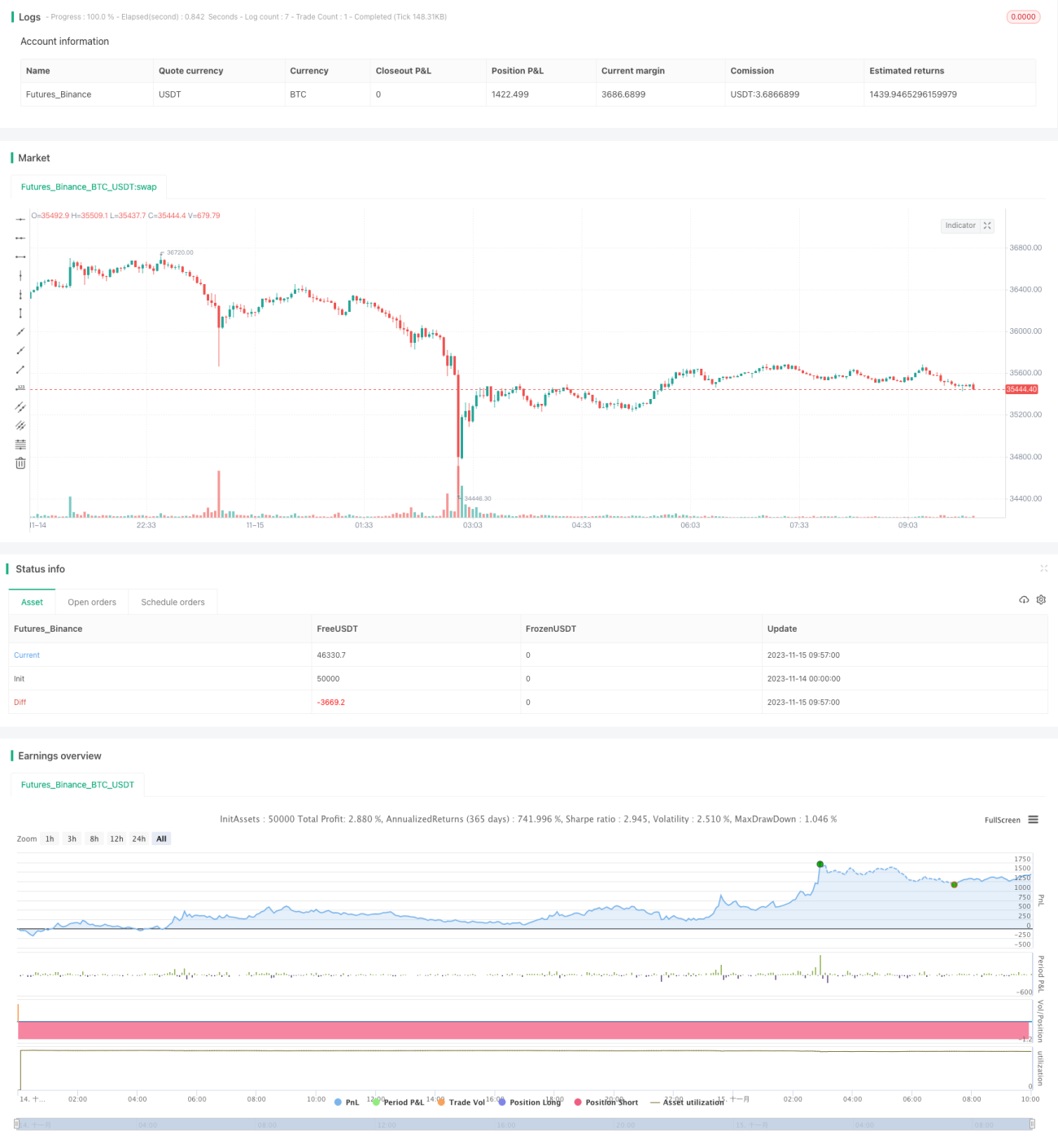

이중궤도 시스템 모멘텀 트레이딩 전략

[trans]

개요

본 전략은 MACD와 Stoch RSI 두 가지 지표를 조합하여 이중 레일 트레이딩 시스템을 구축, 추세 추종과 과매도/과매수 판단을 수행합니다. 또한 일봉과 4시간봉에 각각 지표를 구성하여 다중 시간 프레임 판단을 통해 오판 확률을 낮춥니다.

전략 원리

전략은 MACD와 Stoch RSI라는 서로 다른 유형의 기술 지표를 조합하여 구성합니다. MACD는 모멘텀 지표로서 가격 변화 속도를 판단하고, Stoch RSI는 과매수/과매도 지표로서 가격의 상대적 강도를 판단합니다.

먼저 일봉과 4시간봉에 각각 MACD와 Stoch RSI 지표를 구성하여 추세 및 과매수/과매도 신호를 판단합니다. 두 시간 프레임의 지표가 동시에 매수/매도 신호를 발생시키면 해당 매수/매도 거래를 실행합니다.

구체적으로, MACD 지표의 DIF선과 DEA선이 골든크로스/데드크로스를 형성하면 판단 기준이 되고, Stoch RSI 지표의 K선과 D선이 골든크로스/데드크로스를 형성하면 판단 기준이 됩니다. 두 지표 쌍이 동시에 골든크로스를 보이면 매수 신호, 동시에 데드크로스를 보이면 매도 신호가 생성됩니다.

이처럼 이중 지표 시스템과 다중 시간 프레임 판단을 종합적으로 활용하여 가격 변화 속도와 상대적 강도를 면밀히 평가함으로써 의사 결정의 정확성을 높이고 더 나은 수익을 얻을 수 있습니다.

장점 분석

본 전략은 다음과 같은 장점을 가집니다:

- 이중 지표 시스템 조합으로 포괄적 판단, 의사 결정 정확도 향상

- 다중 시간 프레임 활용으로 오판 확률 감소

- 추세 추종과 과매수/과매도 판단을 결합하여 가격 변화 속도와 상대적 강도 모두 고려

- 지표 파라미터 조정 가능하여 다양한 상품 및 시장 환경에 대응

- 코드 구조가 명확하여 이해와 확장이 용이

리스크 분석

본 전략에는 다음과 같은 리스크도 존재합니다:

- 시장 시스템 리스크는 완전히 회피할 수 없음

- 지표 파라미터 설정이 부적절하면 과도한 거래나 기회 손실 발생 가능

- 이중 지표가 동시에 오류 신호를 줄 가능성이 있으나 단일 지표보다는 낮음

- 블랙스완 사건 같은 급격한 시장 변화에 대응 어려움

대응 방안:

- 파라미터 최적화, 매매 조건 조정으로 오판 감소

- 더 많은 지표를 결합하여 판단 근거 추가

- 손절 전략 추가로 단일 손실 위험 통제

최적화 방향

본 전략은 다음과 같은 측면에서 추가 최적화가 가능합니다:

- 더 많은 지표를 조합하여 다중 지표 전략 구축

- 머신러닝 알고리즘 추가로 동적 파라미터 최적화 구현

- 감성 지표, 뉴스 등 추가 요소를 결합하여 시장 상황 판단 강화

- 손절, 익절 전략 추가로 자금 관리 최적화

- 더 많은 거래 상품으로 확장하여 더 나은 거래 기회 발굴

요약

본 전략은 이중 지표 시스템과 다중 시간 프레임 판단을 조합하여 가격 변화 속도와 상대적 강도를 포괄적으로 평가함으로써 시장 추세를 효과적으로 포착하고 단일 지표의 오판 단점을 개선합니다. 또한 파라미터 조정이 유연하고 이해와 확장이 용이한 장점이 있습니다. 추후 다중 지표 조합, 동적 파라미터 최적화, 감성 지표 도입 등을 통해 확장 및 최적화하여 전략 성과를 더욱 향상시킬 수 있습니다.

||

Overview

This strategy combines the MACD and Stoch RSI indicators to build a dual-rail trading system for trend tracking and oversold/overbought judgment. The strategy also builds indicators on the daily and 4-hour timeframes to make multi-timeframe judgments to reduce misjudgment probability.

Strategy Principle

The strategy combines the MACD and Stoch RSI indicators, which are different types of technical indicators, for configuration. MACD is a momentum indicator that judges price change velocity; Stoch RSI is an overbought/oversold indicator that judges relative price strength.

The strategy first constructs the MACD and Stoch RSI indicators on the daily and 4-hour timeframes respectively for trend and overbought/oversold judgments. When signals are triggered on both timeframes, corresponding buy/sell operations are performed.

Specifically, the MACD indicator is constructed with the DIF and DEA lines forming golden/dead crosses for judgment; the Stoch RSI indicator is constructed with the K and D lines forming golden/dead crosses for judgment. When both indicator pairs have golden crosses, buy signals are generated; when both have dead crosses, sell signals are generated.

Thus, by comprehensively applying the dual-indicator system and multi-timeframe judgments, the strategy judges price velocity and relative strength thoroughly, which helps improve decision accuracy and gain better returns.

Advantage Analysis

This strategy has the following advantages:

- Combining dual-indicator system for comprehensive judgment and higher decision accuracy

- Applying multi-timeframe to reduce misjudgment probability

- Adopting trend tracking and overbought/oversold judgment for consideration of both price velocity and relative strength

- Flexible indicator parameters adjustable for different products and market environments

- Clean code structure easy to understand and expand

Risk Analysis

There are also some risks with this strategy:

- There exist systemic market risks that cannot be fully avoided

- Inappropriate indicator parameter settings may lead to overtrading or missing opportunities

- Dual indicators may still give concurrent wrong signals, but less likely than single ones

- Unable to cope with drastic market changes like black swan events

Countermeasures:

- Optimize parameters and adjust trading conditions to reduce misjudgments

- Incorporate more indicators for combined judgments

- Add stop loss mechanisms to control single loss risk

Optimization Directions

This strategy can also be improved in the following aspects:

- Incorporate more indicators for multi-indicator strategies

- Add machine learning algorithms for dynamic parameter optimization

- Combine sentiment indicators, news etc. for more comprehensive market condition judgments

- Add stop loss, take profit strategies to optimize money management

- Expand to more trading products to discover better opportunities

결론

이중 지표 시스템과 다중 시간대 판단을 결합하여, 이 전략은 가격 속도와 상대적 강도를 종합적으로 평가함으로써 시장 추세를 효과적으로 포착하고 단일 지표의 한계를 보완합니다. 또한 파라미터 조정이 유연하고, 이해하기 쉬우며 확장이 용이한 장점이 있습니다. 다중 지표 조합, 동적 파라미터 최적화, 감정 지표 통합 등을 통한 추가 확장을 통해 전략 성과를 더욱 향상시킬 수 있습니다.

/*backtest

start: 2023-11-14 00:00:00

end: 2023-11-15 10:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title='[RS]Khizon (UWTI) Strategy V0', shorttitle='K', overlay=false, pyramiding=0, initial_capital=100000, currency=currency.USD)

// || Inputs:

macd_src = input(title='MACD Source:', defval=close)- 1