이중 이동평균선 교차 추세 전략

개요

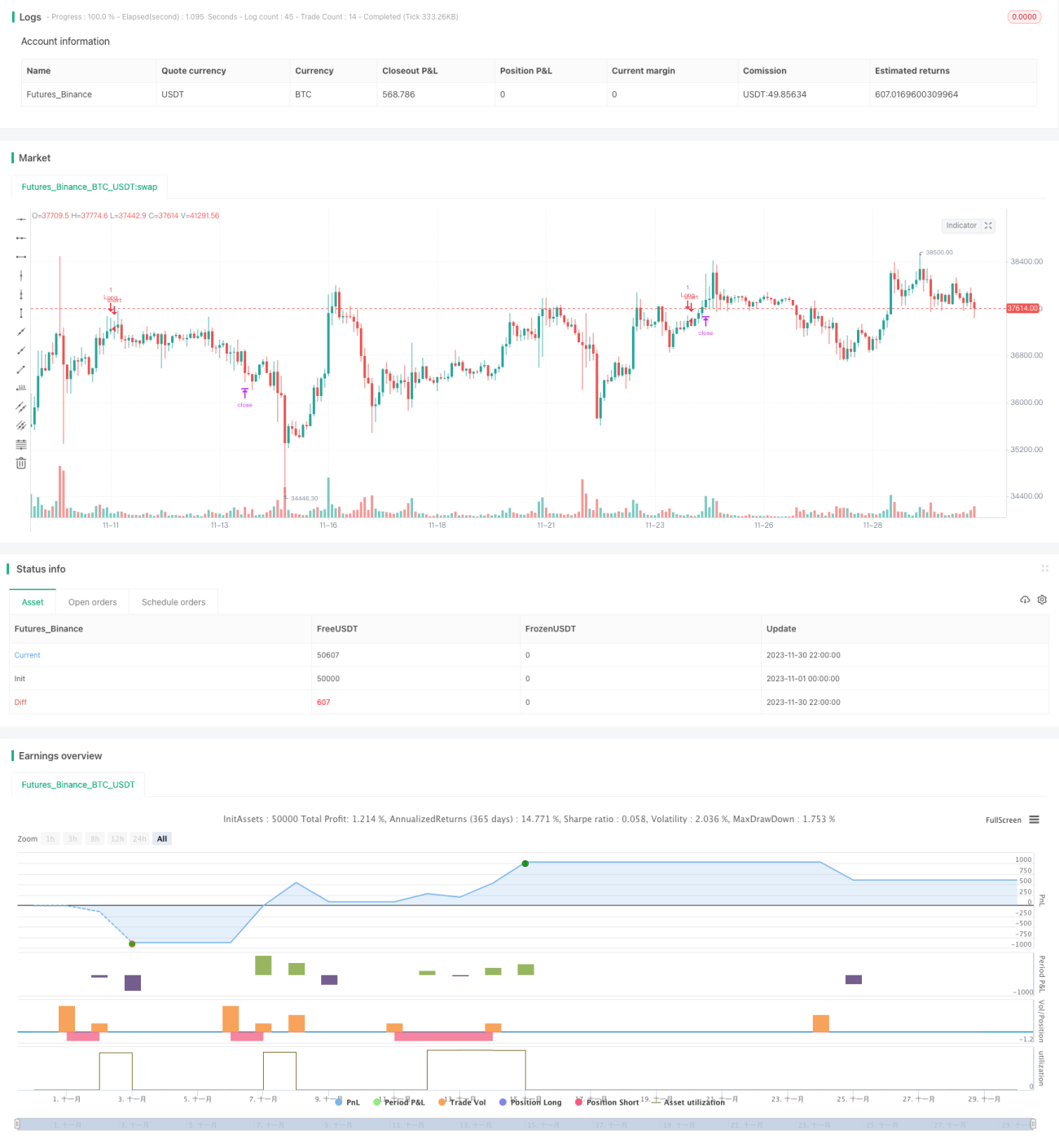

이중 이동평균선 교차 추세 전략은 이동평균선을 기반으로 하는 거래 전략입니다. 빠른선 EMA와 느린선 SMA의 교차를 매수 및 매도 신호로 활용하며, MACD 지표의 다이버전스를 결합하여 신호를 필터링합니다. 이 전략은 가격, 추세, 모멘텀 등 여러 요소를 동시에 고려하여 비교적 완전한 거래 체계를 형성합니다.

전략 원리

이 전략은 EMA와 SMA 두 개의 이동평균선을 사용합니다. EMA는 200일, SMA는 100일을 기준으로 합니다. 가격이 상승하여 두 이동평균선을 돌파하면 매수 신호가 발생하고, 가격이 하락하여 두 이동평균선을 돌파하면 매도 신호가 발생합니다. 이를 통해 횡보 추세와 단기 되돌림을 효과적으로 필터링할 수 있습니다.

신호의 신뢰성을 더욱 높이기 위해 전략에는 MACD 지표도 도입되었습니다. 가격이 EMA와 SMA를 돌파하여 신호를 형성할 때, MACD의 빠른선이 느린선을 아래에서 위로 돌파하고 MACD 히스토그램이 0축 위에 있어야 실제 매수 신호가 발생합니다. 반대로 MACD의 빠른선이 느린선을 위에서 아래로 돌파하고 MACD 히스토그램이 0축 아래에 있을 때 실제 매도 신호가 발생합니다.

또한 전략에는 손절매와 이익실현이 설정되어 있습니다. 포지션 진입 후 사용자가 설정한 비율에 따라 손절매 및 이익실현 지점이 계산되어 설정됩니다. 이를 통해 개별 거래의 위험을 효과적으로 통제할 수 있습니다.

전반적으로 이 전략은 여러 지표를 종합적으로 고려하고 매수 및 매도 신호에 엄격한 필터링 조건을 적용하며 손절매 및 이익실현을 통해 위험을 관리하여 비교적 엄격하고 완전한 거래 체계를 형성합니다.

장점 분석

이중 이동평균선 교차 추세 전략은 다음과 같은 몇 가지 장점이 있습니다.

-

다중 지표를 결합하여 가격, 추세, 모멘텀을 종합적으로 고려하며 신호에 엄격한 필터링 조건을 적용하여 허위 신호를 효과적으로 방지하고 신호의 신뢰성을 높일 수 있습니다.

-

서로 다른 매개변수의 두 이동평균선을 사용하여 시장 추세를 더 잘 식별하고 횡보 장세를 필터링할 수 있습니다. 빠른 EMA선은 가격 변화를 신속하게 추적하고 느린 SMA선은 장기 추세를 판단하는 데 사용됩니다. 두 이동평균선의 조합은 더 나은 효과를 냅니다.

-

MACD 지표에 각 매개변수를 설정할 수 있어 시장 특성에 따라 조정이 가능하며 유연성이 높습니다. MACD 설정은 거래 신호가 가격, 추세, 모멘텀의 지지를 동시에 받도록 보장하여 적용 가치가 높습니다.

-

손절매 및 이익실현 지점을 설정하여 개별 거래의 손실을 최대한 통제하고 단일 거래 손실이 과도해지는 위험을 방지합니다. 합리적인 비율의 이익실현은 일부 이익을 확보하고 수익 후 시장 위험 노출을 낮출 수 있습니다.

-

이 전략의 매개변수는 유연하게 설정할 수 있으며 최적화 결과에 따라 전략을 조정할 수 있어 실용성이 매우 높습니다. 다양한 시장 및 매개변수 테스트를 통한 최적화 여지가 큽니다.

위험 분석

이중 이동평균선 교차 추세 전략에는 다음과 같은 몇 가지 위험도 존재합니다.

-

주가가 심하게 변동할 때 EMA와 SMA가 여러 번 잘못 교차하여 거래 신호가 빈번하게 발생할 수 있습니다. 이는 거래 빈도와 수수료 지출을 증가시킵니다.

-

MACD 지표는 특히 변동성이 불분명한 상황에서 가짜 돌파가 발생할 수 있습니다. 이런 경우 신호도 신뢰할 수 없어 불필요한 손실을 초래할 수 있습니다.

-

손절매 설정 위치와 비율은 손익 결과에 큰 영향을 미칩니다. 손절매가 너무 좁게 설정되면 물릴 위험이 있고, 너무 넓게 설정되면 단일 손실이 과중해질 수 있습니다. 최적의 매개변수를 찾기 위해 충분한 테스트가 필요합니다.

-

이동평균선은 추세 추종 지표로서 가격이 급격히 반전될 때 그 지시 효용이 떨어집니다. 전략이 손절매를 실행하기 전에 가격 반전에 직면하여 큰 손실을 볼 수 있습니다.

이에 대한 해결 방법은 다음과 같습니다.

-

심한 변동 장세에서는 이동평균선 매개변수를 적절히 조정하여 낮은 매개변수의 EMA와 SMA를 사용하여 교차 횟수를 줄일 수 있습니다.

-

MACD 0축 상하 돌파 필터링 조건을 추가하면 가짜 돌파를 어느 정도 줄일 수 있습니다. KDJ, BOLL 등 다른 지표를 조합하는 것도 고려할 수 있습니다.

-

손절매 위치와 비율 설정은 충분한 백테스트 최적화를 통해 최적의 매개변수를 찾아야 합니다. 이를 바탕으로 지속적인 모니터링과 동적 조정도 고려해야 합니다.

-

가격 급격 반전을 식별하는 메커니즘을 설정할 수 있습니다. 이상 반전이 감지되면 포지션 축소 또는 전략 일시 중단 등의 응급 조치를 통해 위험 노출을 통제합니다.

최적화 방향

이중 이동평균선 교차 추세 전략은 다음과 같은 몇 가지 측면에서 추가 최적화 여지가 있습니다.

-

더 많은 지표 조합을 테스트하여 더 나은 매개변수를 찾습니다. 예를 들어 BOLL 채널을 도입하고 변동성 영향을 고려하는 등이 있습니다.

-

이동평균선 길이 매개변수를 최적화하여 다양한 시장 조건에서 최적의 매개변수 조합을 찾습니다. 매개변수 롤링 최적화도 하나의 선택입니다.

-

보다 과학적이고 합리적인 이익실현 및 손절매 전략을 설정합니다. 예를 들어 트레일링 스탑을 도입하거나 과거 통계 결과에 기반한 동적 위험 보상 비율을 설정하는 등입니다. 이를 통해 전략 안정성을 더욱 높일 수 있습니다.

-

가격 이상 반전에 대한 자동 인식 및 비상 대응 메커니즘을 구축합니다. 극단적인 장세에서 능동적으로 포지션을 축소하거나 전략을 일시 중단하여 막대한 손실을 방지합니다.

-

거래 대상 종목을 확장합니다. 예를 들어 외환, 디지털 통화 등 다른 종목에 적용합니다. 다양한 종목에서의 매개변수 강건성을 테스트하여 전략 적용 범위를 넓힙니다.

-

전략의 자금 관리 전략을 최적화합니다. 예를 들어 정액 거래, 고정 포지션 비율 등을 적용합니다. 개별 거래 손실 위험을 통제하여 전체 자금 곡선을 더욱 안정적으로 만듭니다.

요약

이중 이동평균선 교차 추세 전략은 여러 요소를 종합적으로 고려하여 거래 신호를 발생시킬 때 가격, 추세, 모멘텀 등 여러 지표의 지지를 필요로 하여 신호의 신뢰성을 보장합니다. 또한 이동 손절매 및 이익실현을 사용하여 개별 거래의 위험을 효과적으로 통제할 수 있습니다. 이 전략은 매개변수 설정이 유연하고 실용성이 높아 자동 거래에 적합합니다.

그러나 어떤 전략도 완벽할 수 없습니다. 이 전략을 적용할 때도 빈번한 거래, 가짜 돌파, 손절매 위치 설정 등의 어려움에 직면할 수 있습니다. 이러한 문제는 최적의 매개변수 조합 도출, 새로운 기술 지표 조합 도입, 손절매 메커니즘 개선 등 여러 측면에서 접근하여 전략의 견고성과 수익성을 더욱 강화해야 합니다.

전반적으로 이중 이동평균선 교차 추세 전략은 비교적 완전하고 엄격한 거래 체계를 형성합니다. 향후 연구와 적용에서 지속적인 최적화와 개선을 통해 이 전략은 더 큰 실전 가치를 발휘할 수 있을 것으로 기대됩니다.

/*backtest

start: 2023-11-01 00:00:00

end: 2023-11-30 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// Hi,

// This is my first strategy made by myself(except for the MACD indicator). I'm publishing this to get myself out there and for some newer people to see how a basic strategy works. All credits go to Zen&TheArtofTrading, for teaching me almost everything I know about Pinescript

// The strategy is basically an MACD crossover trend strategy. If the MACD line crosses the signal line upward, above the zero point of the histogram, while the price is above 200 EMA and 100 SMA it's a buy signal- 1