이동평균선 볼린저 밴드 돌파 전략

1

Follow

1802

Followers

개요

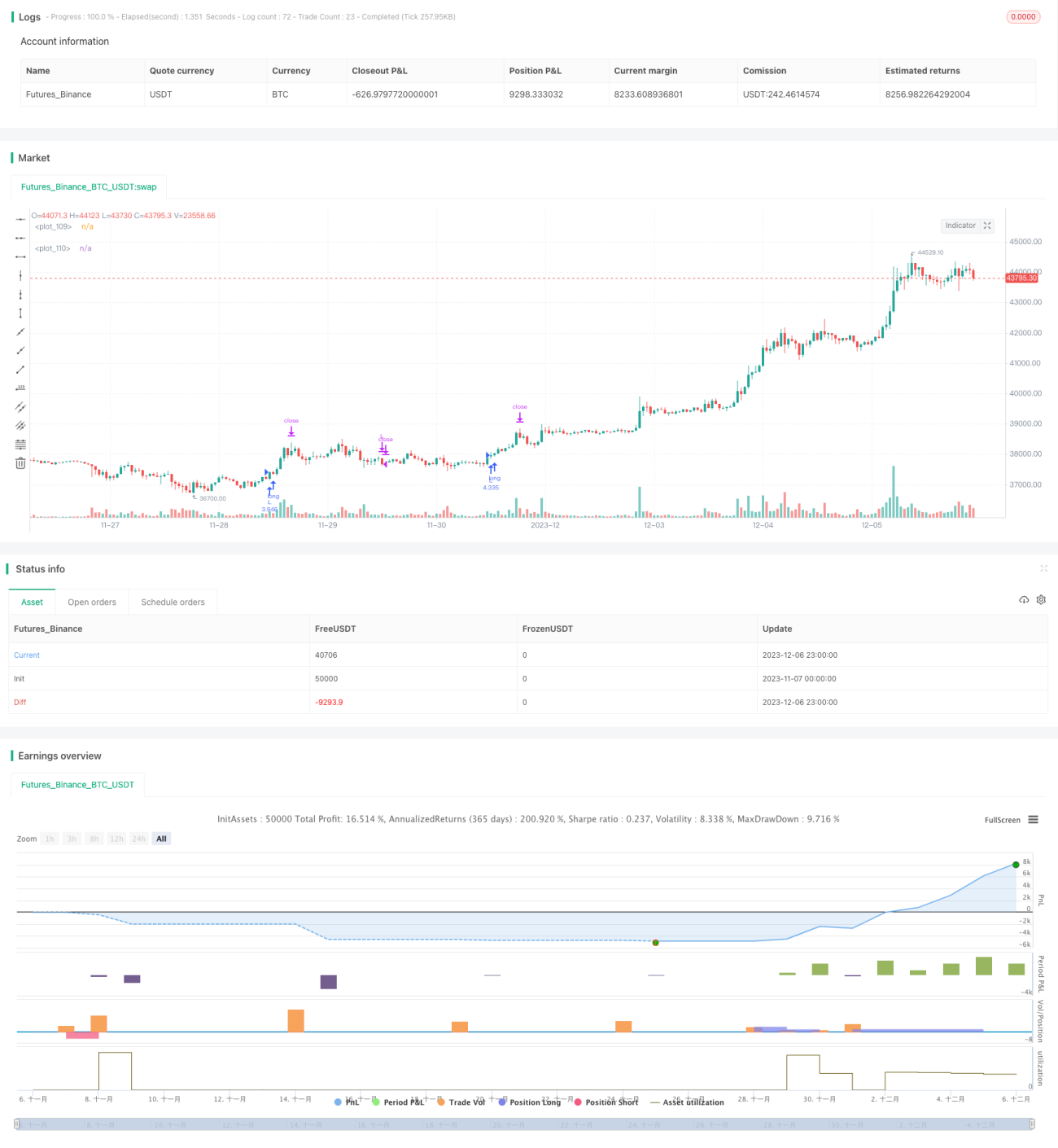

해당 전략은 이동평균선 지표, 볼린저 밴드 지표, UT Bot Alerts 지표를 결합하여 간단한 돌파 매매 전략을 구현합니다. 가격이 볼린저 밴드 상단을 돌파하면 매수하고, 가격이 볼린저 밴드 하단을 돌파하면 매도합니다.

전략 원리

- 200주기 EMA를 추세 판단의 중축선으로 사용합니다. 가격이 EMA 위에 있으면 상승 추세, 가격이 EMA 아래에 있으면 하락 추세로 간주합니다.

- UT Bot Alerts 지표는 ATR과 결합하여 매수/매도 신호를 생성합니다. 가격과 빠른 EMA가 볼린저 밴드 상단을 교차하면 매수 신호, 가격과 빠른 EMA가 볼린저 밴드 하단을 교차하면 매도 신호가 발생합니다.

- ATR 손절 지표를 사용하여 손절점을 설정합니다. 손절 거리는 ATR 값의 1.5배입니다.

- 진입 후 위험 보상 비율을 사용하여 손절점, 이익 실현점을 설정하고, 손절을 진입 가격으로 이동시킵니다.

장점 분석

- 볼린저 밴드 지표를 사용하여 매수/매도 타이밍을 판단하면 수익 확률을 높일 수 있습니다.

- UT Bot Alerts 지표는 비교적 정확한 신호를 생성할 수 있습니다.

- 위험 보상 비율을 사용하여 손절 및 이익 실현을 설정함으로써 위험을 효과적으로 통제할 수 있습니다.

위험 분석

- 볼린저 밴드는 횡보장에서 잘못된 신호를 발생시키기 쉽습니다.

- ATR은 지연성이 있어 추세 시작 단계에서 손절 거리가 너무 클 수 있습니다.

- 위험 보상 비율이 적절하지 않게 설정되면 지나치게 공격적이거나 지나치게 보수적인 매매가 될 수 있습니다.

최적화 방향

- UT Bot Alerts 지표 대신 다른 지표를 사용해 볼 수 있습니다.

- ATR의 주기와 배수를 최적화하여 손절 거리를 더 적절하게 조정할 수 있습니다.

- 다양한 위험 보상 비율을 테스트하여 최적의 매개변수를 찾을 수 있습니다.

요약

해당 전략은 여러 지표의 장점을 통합하여 실용성이 높습니다. 매개변수 최적화를 통해 안정적이고 신뢰할 수 있는 돌파 시스템이 될 수 있습니다. 다만 지표의 효력 상실과 부적절한 매개변수로 인한 위험을 주의해야 합니다.

Source

Pine

/*backtest

start: 2023-11-07 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

//Developed by StrategiesForEveryone

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1