가격 변화율과 이동평균선 기반의 퀀트 전략

1

Follow

1802

Followers

개요

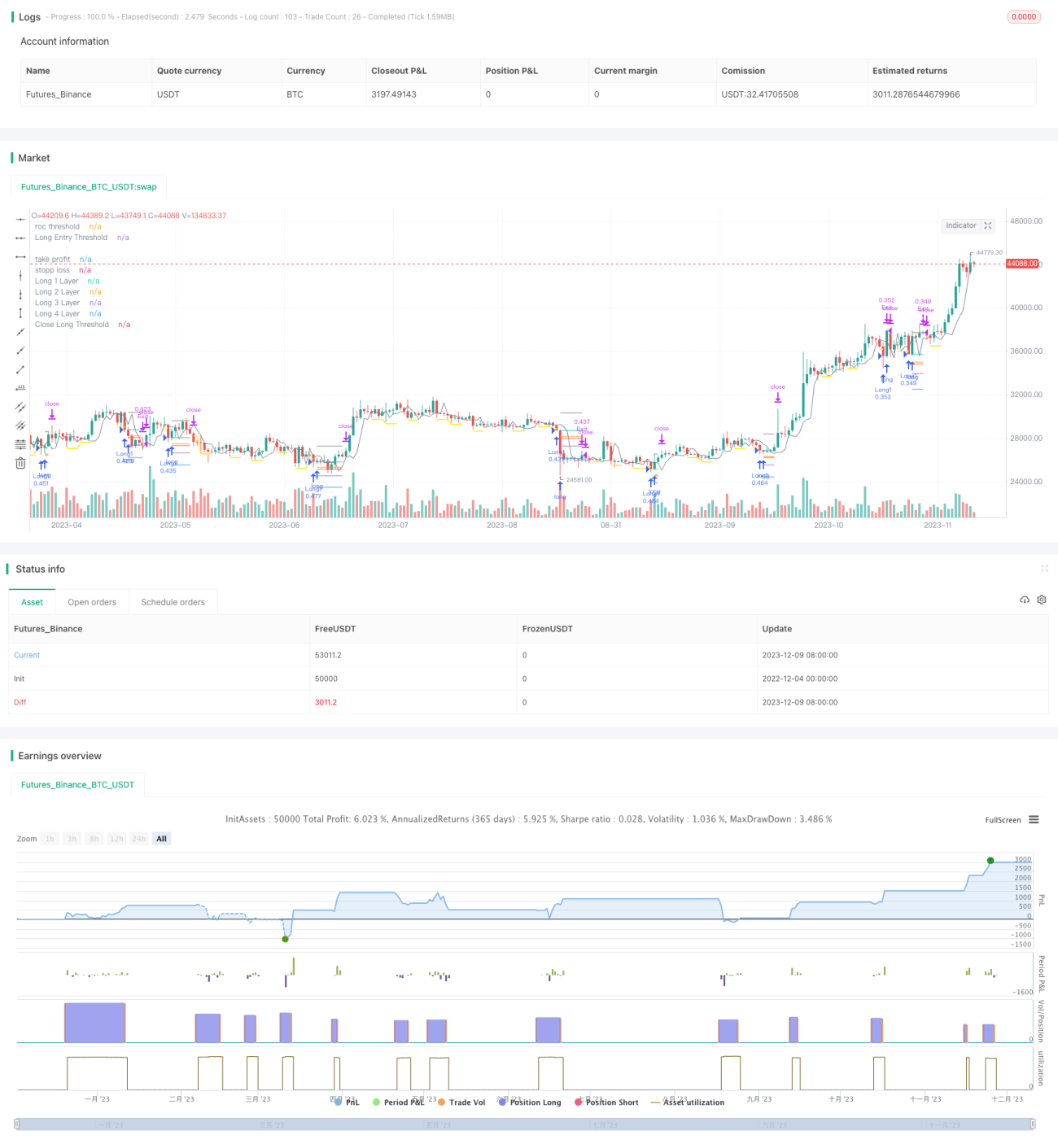

해당 전략은 가격 변화율과 이동평균선의 기술적 지표를 결합하여 매수 지점과 매도 지점을 정밀하게 찾아냅니다. 가격이 뚜렷하게 하락할 때 매수 임계값을 설정하고, 추가 하락 시 롱 포지션을 오픈합니다. 가격이 상승할 때는 매도 임계값을 설정하고, 추가 상승 시 포지션을 청산합니다. 또한, 전략은 포지션을 분할하여 여러 번 매수하는 방식(분할 매수)을 채택하여 비용을 낮춥니다.

전략 원리

매수 로직

- 가격 변화율(ROC)을 계산하고 매수 임계값 라인을 설정합니다.

- 가격이 매수 임계값 라인 아래로 떨어지면 해당 지점을 기록하고 매수 제한 라인을 활성화합니다.

- 매수 제한 라인은 입력 매개변수에 따라 지속 시간이 설정되며, 만료 후 비활성화됩니다.

- 가격이 계속 하락하여 매수 제한 라인을 아래로 돌파하면 첫 번째 롱 포지션을 오픈합니다.

매도 로직

- 가격 변화율(ROC)을 계산하고 매도 임계값 라인을 설정합니다.

- 가격이 매도 임계값 라인 위로 돌파하면 해당 지점을 기록하고 매도 제한 라인을 활성화합니다.

- 매도 제한 라인은 입력 매개변수에 따라 지속 시간이 설정되며, 만료 후 비활성화됩니다.

- 가격이 계속 상승하여 매도 제한 라인을 위로 돌파하면 모든 롱 포지션을 청산합니다.

위험 관리

전략에는 손절매와 이익 실현 기능이 내장되어 있으며, 매개변수를 사용자 정의하여 보유 포지션의 위험을 실시간으로 제어할 수 있습니다.

분할 매수 방식

각 거래 포지션이 열릴 때마다 입력 매개변수에 따라 일정 비율로 후속 매수 가격을 설정하여 분할 매수(포지션 추가) 효과를 구현합니다.

장점 분석

- 가격 변화율 지표 ROC를 사용하여 매매 지점을 찾습니다. ROC는 가격 변화에 매우 민감하므로 매수/매도 지점을 정확하게 포착합니다.

- 제한 라인 방식을 사용하여 매매 타이밍을 추가로 확인함으로써 가짜 돌파를 방지합니다.

- 분할 매수 방식을 통해 위험을 통제 가능한 범위 내에서 유지하면서 시장 가치를 추적할 수 있습니다.

- 내장된 손절매 및 이익 실현 기능으로 단일 포지션의 위험을 엄격하게 관리합니다.

위험 및 해결 방안

- 시장이 급격하게 변동할 때 전략이 너무 많은 포지션을 열 수 있습니다. 해결 방법은 분할 매수 매개변수를 합리적으로 설정하고 총 포지션 수를 제어하는 것입니다.

- 가격이 뚜렷한 추세 없이 횡보할 경우 손절매나 이익 실현 가격이 자주 트리거될 수 있습니다. 손절매/이익 실현 범위를 적절히 넓히거나 해당 기능을 비활성화할 수 있습니다.

최적화 제안

- 다른 지표를 결합하여 진입 시점을 필터링합니다. 예를 들어 이동평균선과 함께 사용하여 가격이 이동평균선 아래로 떨어질 때만 ROC 지표를 신뢰합니다.

- 분할 매수 로직을 최적화하여 특정 조건이 충족될 때만 분할 매수를 활성화합니다. 예를 들어 가격이 일정 폭 이상 추가 하락할 때만 계속 매수합니다.

- 다양한 종목에 따라 매개변수 설정이 크게 다를 수 있으므로 충분한 백테스트와 모의 거래를 통해 최적의 매개변수 조합을 찾아야 합니다.

- 적응형 손절매/이익 실현을 설정하여 시장 변동성에 따라 다른 손절매 폭을 적용할 수 있습니다.

요약

해당 전략은 ROC 지표를 종합적으로 활용하여 매수/매도 지점을 정밀하게 찾고, 제한 라인 방식으로 신호를 필터링하며, 내장된 손절매/이익 실현으로 위험을 방지하고, 분할 매수를 통해 수익을 확대합니다. 매개변수가 합리적으로 설정된 경우, 위험을 통제 가능한 범위 내에서 유지하면서 초과 수익을 얻을 수 있습니다. 향후 신호 필터링 및 위험 관리 메커니즘을 더욱 최적화하여 다양한 시장 환경에 적응할 수 있도록 할 수 있습니다.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1