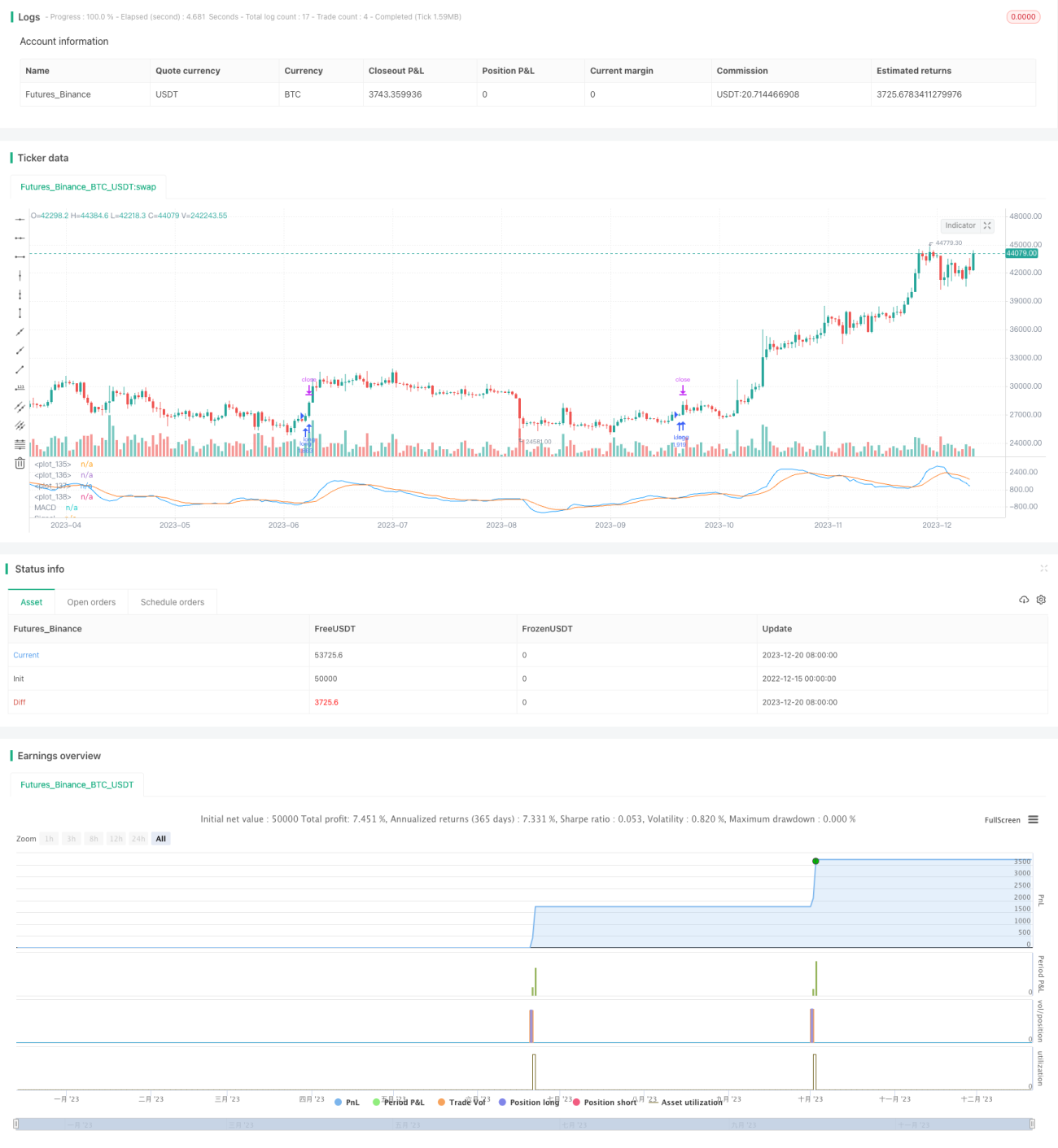

사용자 정의 비재도화 HTF MACD MFI 확장 가능 로봇 전략

개요

해당 전략은 높은 사용자 정의가 가능한 비재도장 MACD 및 MFI 지표의 조합 전략으로, 알고리즘 트레이딩 봇에 적합합니다. 추세 지표와 모멘텀 지표를 결합하여 다양한 필터를 통해 트레이딩 신호를 생성합니다.

전략 원리

이 전략은 MACD 지표를 사용하여 시장 추세 방향을 판단합니다. MACD는 추세 추종형 모멘텀 지표로, 빠른 이동 평균선에서 느린 이동 평균선을 뺀 MACD 히스토그램과 MACD의 지수 이동 평균선을 통해 시그널 라인을 얻습니다. 빠른 선이 느린 선을 상향 돌파하면 매수 신호, 하향 돌파하면 매도 신호입니다.

또한, 이 전략은 MFI 지표를 사용하여 시장의 과매수/과매도 상태를 판단합니다. MFI 지표는 가격과 거래량 정보를 결합하며, 값은 0에서 100 사이에서 변동합니다. MFI가 20 미만이면 과매도 영역, 80 초과이면 과매수 영역입니다.

허위 신호를 걸러내기 위해 이 전략에는 추세 필터와 RSI 필터도 추가되었습니다. 가격이 상승 추세에 있고 RSI가 설정된 임계값보다 낮을 때 매수 신호가 발생합니다.

전략 장점

- 여러 지표를 조합하여 시장 상태를 종합적으로 판단, 승률 향상

- 필터 메커니즘을 추가하여 허위 신호 방지, 불필요한 거래 감소

- 다양한 파라미터 및 필터를 사용자 정의할 수 있어 여러 종목 및 거래 선호도에 적응 가능

- 수동 거래에 사용하거나 알고리즘 봇에 연결하여 프로그램 트레이딩 가능

전략 리스크 및 해결 방법

-

지표 파라미터 설정이 부적절하면 허위 신호가 발생하기 쉬움

-

다양한 파라미터를 테스트하여 최적의 조합 선택 가능

-

여러 종목에 파라미터가 공통적으로 적용되지 않으므로 각각 테스트 및 최적화 필요

-

거래 빈도가 너무 높아 거래 비용 및 슬리피지 위험 증가

-

필터를 조정하여 거래 빈도 낮출 수 있음

-

실전 거래 시 비용 관리에 주의

전략 최적화 방향

- 더 긴 데이터 기간을 테스트하여 파라미터 안정성 평가

- 다양한 지표 파라미터 조합 시도

- 지표 가중치 최적화로 전략 안정성 향상

- 더 많은 필터 추가하여 불필요한 거래 감소

요약

해당 전략은 높은 사용자 정의가 가능한 추세 추종형 전략으로, 추세 및 모멘텀 지표를 결합하여 시장 상태를 판단하고 필터 메커니즘을 효과적으로 활용하여 리스크를 관리합니다. 수동 거래에 사용하거나 알고리즘 봇에 연결하여 높은 수준의 자동화된 프로그램 트레이딩을 구현할 수 있으며, 장기적으로 추적 및 최적화할 가치가 있는 전략 체계입니다.

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//(c) Wunderbit Trading

//Modified by Mauricio Zuniga - Trade at your own risk

//This script was originally shared on Wunderbit website as a free open source script for the community. (https://help.wundertrading.com/en/articles/5246468-macd-mfi-trading-bot-for-ftx)

// - 1