포인트 손절매 및 이익실현 기반 이동 손절매 전략

개요

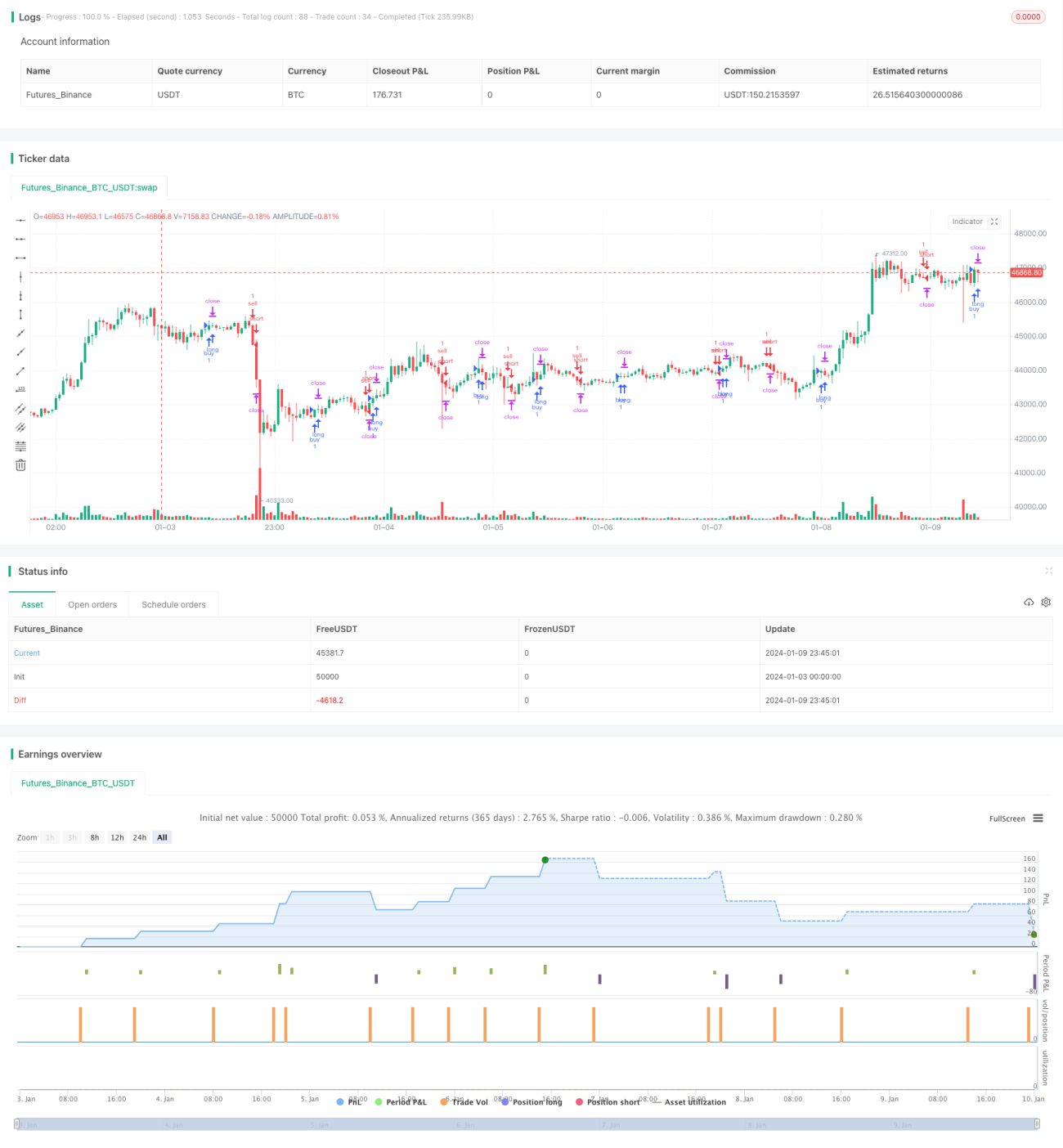

해당 전략의 핵심 아이디어는 EMA와 WMA의 교차를 진입 신호로 활용하고, 포인트 기반으로 계산된 손절매 및 이익실현을 통해 거래를 진행하는 것입니다. 가장 큰 장점은 포인트 크기를 조정하여 손절 및 이익실현 폭을 제어함으로써 매우 유연하고 정밀하게 리스크를 관리할 수 있다는 점입니다.

전략 원리

EMA가 아래에서 위로 WMA를 돌파하면 매수 신호가 발생하고, EMA가 위에서 아래로 WMA를 하향 돌파하면 매도 신호가 발생합니다. 포지션 진입 후에는 진입 가격을 실시간으로 계산하여 이를 기준으로 손절매와 이익실현을 설정합니다. 예를 들어 손절 20포인트, 이익실현 100포인트로 설정하면 구체적인 손절 가격은 진입가에서 20포인트 × 계약 가치를 뺀 값이 되고, 이익실현 가격은 진입가에 100포인트 × 계약 가치를 더한 값이 됩니다. 이렇게 하여 리스크와 수익을 제어합니다.

동시에 전략은 현재 호가창과 과거 손절매 값을 비교하여 이동 손절매 위치를 조정함으로써 유동적 손절매 추적을 구현합니다.

장점 분석

일반적인 고정 포인트 또는 백분율 손절매에 비해 이 전략의 가장 큰 장점은 매우 유연하고 정밀하게 리스크를 제어할 수 있다는 점입니다. 포인트 크기를 조정하면 손절매 폭에 직접적인 영향을 미칠 수 있습니다. 이는 다양한 거래 종목에 적합하며, 시장의 변동성 빈도와 폭에 따라 미세 조정이 가능합니다.

또한 유동적 손절매(Trailing Stop)는 매우 실용적인 기능입니다. 시세의 실시간 변화에 따라 손절매 위치를 추적 조정하여 리스크를 통제하면서도 더 큰 수익을 추구할 수 있습니다.

리스크 분석

이 전략의 주요 리스크는 EMA와 WMA라는 두 지표 자체에서 발생합니다. 시장이 급격하게 변동할 때 이들 지표는 종종 잘못된 신호를 발생시켜 손절매가 발생하기 쉽습니다. 이러한 경우 손절매 포인트를 적절히 완화하거나 다른 지표 조합으로 대체하는 것을 고려하는 것이 좋습니다.

또 다른 리스크 포인트는 손절매와 이익실현을 동시에 만족시키기 어렵다는 점입니다. 더 높은 이익실현을 추구하려면 일반적으로 더 큰 리스크를 감수해야 하며, 이는 시장이 반전할 때 쉽게 손절매당할 수 있습니다. 따라서 손절매 및 이익실현 설정은 신중한 테스트와 평가가 필요합니다.

최적화 방향

해당 전략은 다음과 같은 방향으로 최적화할 수 있습니다:

- 다양한 파라미터의 EMA와 WMA 조합을 테스트하여 최적의 파라미터를 찾습니다.

- MACD, KDJ 등의 다른 지표를 대체하거나 결합하여 승률을 높일 수 있는지 확인합니다.

- 다양한 손절매 및 이익실현 포인트의 리스크-수익 상황을 평가하여 최적 구성을 찾습니다.

- 각 거래 종목의 특성을 연구하고 파라미터를 조정하여 다양한 시장에 적응시킵니다.

- 머신러닝 알고리즘을 도입하여 파라미터의 동적 최적화를 구현합니다.

요약

이 전략의 핵심 아이디어는 간단하고 명확합니다. EMA와 WMA 지표를 기반으로 하고 포인트 기반 손절매 및 이익실현 메커니즘을 사용하여 리스크를 통제합니다. 전략의 장점은 리스크 관리가 정밀하고 유연하며, 각 시장에 맞게 적절히 조정할 수 있다는 점입니다. 향후 진입 신호, 파라미터 선택, 손절매 메커니즘 등의 측면에서 심층 최적화를 통해 복잡하고 변화무쌍한 시장 환경에 더욱 적응할 수 있는 전략으로 발전시킬 수 있습니다.

/*backtest

start: 2024-01-03 00:00:00

end: 2024-01-10 00:00:00

period: 45m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// inspiration script from: @ahmad_naquib

// inspiration script link: https://www.tradingview.com/script/tGTV8MkY-Two-Take-Profits-and-Two-Stop-Loss/

// inspiration strategy script name: Two Take Profits and Two Stop Loss

- 1