다중 지표를 통합한 감정 기반 돌파 전략

개요

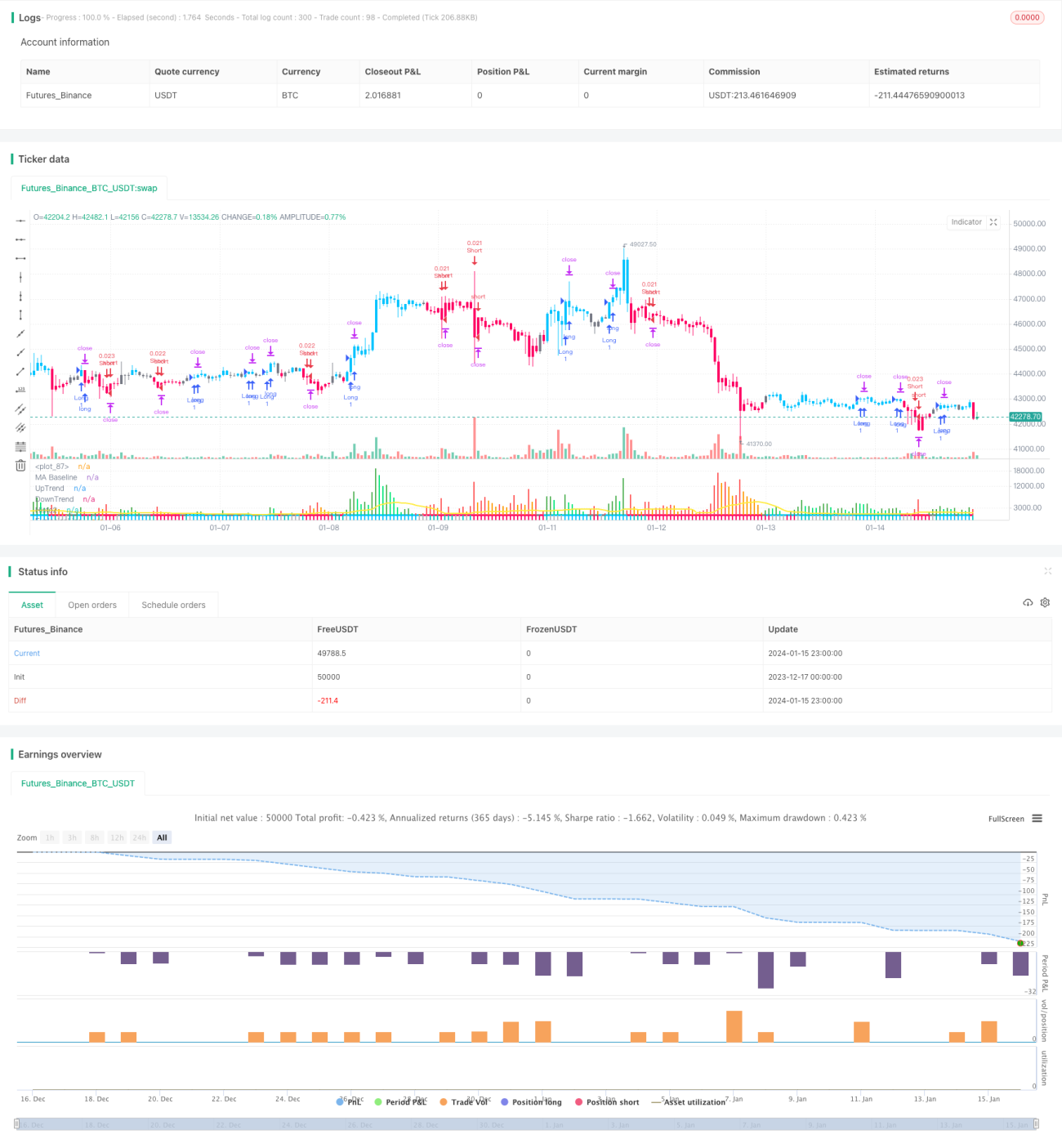

본 전략은 QQE 개량형 지표, SSL 하이브리드 지표, Waddah Attar 폭발 지표라는 세 가지 감성 지표를 융합하여 거래 신호를 형성하며, 다중 지표 기반 감성 돌파 전략에 속합니다. 돌파 전에 시장 심리 상태를 판단하여 가짜 돌파를 피할 수 있어 비교적 우수한 돌파 전략입니다.

전략 원리

본 전략의 핵심 논리는 세 가지 지표를 기반으로 거래 결정을 내립니다.

QQE 개량형 지표: 이 지표는 RSI 지표를 개량하여 더 민감하게 만든 것으로, 시장 심리의 고저를 판단할 수 있습니다. 본 전략에서는 이 지표를 사용하여 바닥 반전 및 상단 반전 신호를 판단합니다.

SSL 하이브리드 지표: 이 지표는 여러 이동 평균선의 돌파 상황을 종합적으로 고려하여 시장 징후를 판단합니다. 본 전략에서는 이 지표를 사용하여 채널 돌파 패턴을 판단합니다.

Waddah Attar 폭발 지표: 이 지표는 채널 내부에서 가격의 폭발 강도를 판단합니다. 본 전략에서는 이 지표를 사용하여 돌파 시 모멘텀이 충분한지 확인합니다.

QQE 지표가 바닥 반전 신호를 보내고 SSL 지표가 채널 상단 돌파를 나타내며, 동시에 Waddah Attar 지표가 모멘텀 폭발을 판단할 때 본 전략은 매수 결정을 내립니다. 세 가지 지표가 동시에 반대 신호를 보낼 때 매도 결정을 내립니다.

본 전략은 또한 손절매 및 이익 실현 정밀 출구 지점을 설정하여 수익을 최대한 확보하며, 고품질의 감성 기반 돌파 전략에 속합니다.

장점 분석

본 전략은 다음과 같은 장점을 가지고 있습니다.

- 다중 지표를 융합하여 시장 심리 상태를 판단하므로 가짜 돌파의 위험을 피할 수 있습니다.

- 반전 지표, 채널 지표 및 모멘텀 지표를 동시에 고려하여 돌파 시장 확인도가 높습니다.

- 고정밀 이동 손절매를 사용하여 위험을 제한하고 수익을 추적 및 고정합니다.

- 매개변수는 많은 최적화 테스트를 거쳐 안정성이 우수하며, 중기에서 장기 보유에 적합합니다.

- 지표 매개변수를 설정하여 전략 스타일을 자율적으로 조정할 수 있어 더 넓은 시장 상황에 적응할 수 있습니다.

위험 분석

본 전략은 주로 다음과 같은 위험이 있습니다.

- 시장 전반이 지속적으로 부진할 때 상대적으로 많은 소폭 손실 거래가 발생할 수 있습니다.

- 여러 지표에 동시에 의존해야 하므로 일부 시장에서는 비정상적으로 작동하지 않을 수 있습니다.

- QQE 지표 등 다중 지표는 매개변수 최적화 과잉 위험이 있으므로 신중하게 설정해야 합니다.

- 이동 손절매는 특수한 시세에서 정상적으로 작동하기 어려울 수 있습니다.

위의 위험에 대해 지표 매개변수를 더 안정적으로 조정하고 보유 기간을 적절히 늘려 수익률을 높이는 것이 좋습니다.

최적화 방향

본 전략은 다음과 같은 측면에서 추가 최적화가 가능합니다.

- 각 지표 매개변수를 조정하여 더 안정적이거나 더 민감하게 만듭니다.

- 변동성 기반의 포지션 규모 최적화 모듈을 추가합니다.

- 머신러닝 위험 관리 모듈을 추가하여 시장 상황을 실시간 평가합니다.

- 딥러닝 모델을 활용하여 지표 패턴을 예측하고 의사 결정 정확도를 높입니다.

- 시간 프레임 간 분석을 도입하여 가짜 돌파 확률을 낮춥니다.

요약

본 전략은 여러 주요 감성 지표의 장점을 종합적으로 활용하여 효율적인 감성 기반 돌파 전략을 구축했습니다. 많은 저품질 돌파로 인한 위험을 성공적으로 회피하는 동시에 고정밀 손절매 개념을 통해 수익을 확보하는 등, 성숙하고 신뢰할 수 있는 돌파 전략 조합으로 학습과 적용 가치가 높습니다. 매개변수의 지속적인 최적화와 모델 예측 도입을 통해 본 전략은 더욱 지속적이고 안정적인 초과 수익을 창출할 것으로 기대됩니다.

- 1