다중 시간대 추세 추종 전략

개요

다중 시간축 추세 추종 전략은 다양한 이동평균선과 회귀선을 결합한 추세 추종 전략입니다. 이 전략은 20종 이상의 다양한 추세 지표 중에서 선택하여 자동 매수 및 매도를 실행할 수 있습니다.

전략 원리

해당 전략의 핵심은 사용자가 선택한 추세 지표를 기반으로 가격이 상승 또는 하락 추세에 있는지 판단하는 것입니다. 전략은 먼저 20종 이상의 이동평균선과 회귀선을 계산합니다. 이러한 지표에는 일반 이동평균선, 가중 이동평균선, 지수 이동평균선 등 Pine 프로그래밍 언어 표준 라이브러리의 지표와 Pine 커뮤니티에서 작성된 사용자 정의 지표가 포함됩니다. 그런 다음 전략은 이러한 지표를 조회하여 현재 특정 지표의 값을 얻고 이전 주기의 값과 비교합니다. 현재 값이 이전 값보다 크면 추세는 상승, 반대로 현재 값이 이전 값보다 작으면 추세는 하락으로 판단합니다. 마지막으로 전략은 추세 방향에 따라 롱 포지션을 설정할지 여부를 결정합니다. 상승 추세에서 롱 포지션을 설정하고 하락 추세에서 청산합니다.

장점 분석

이 전략은 20종 이상의 지표를 결합하여 추세를 판단하므로 단일 지표의 판단 오류 가능성을 줄입니다. 또한 이러한 지표는 커뮤니티 개발자에 의해 검증되었습니다. 다양한 매개변수로 조정할 수 있어 여러 시장 환경에 적용 가능합니다.

단순한 이중 이동평균선 전략과 비교했을 때, 이 전략은 단일 지표만으로 추세 방향을 판단하므로 추세를 더 잘 표현할 수 있으며, 지표가 정반대의 가짜 신호를 생성하지 않습니다.

위험 분석

이 전략은 지표에 의존하여 추세를 판단하므로 추세가 이미 전환되었는지 여부를 판단할 수 없습니다. 따라서 어느 정도의 지연이 발생합니다. 이는 손실이나 기회 상실로 이어질 수 있습니다. 지표 매개변수를 조정하여 이 문제를 완화할 수 있습니다.

돌발 사건 발생 후 모든 추세형 전략은 큰 손실을 입습니다. 손절매를 설정하여 위험을 통제해야 합니다.

최적화 방향

추세 전환을 예측하기 위해 다른 지표 판단을 결합하는 것을 고려할 수 있습니다. 예를 들어 볼린저 밴드 지표를 결합하여 가격이 과도하게 확장되었는지 여부를 판단할 수 있습니다.

돌발 사건에 대비한 비상 손절매 메커니즘을 설계할 수 있습니다. 예를 들어 하루에 5% 이상의 손실이 발생하면 강제 손절매를 시작합니다.

요약

다중 시간축 추세 추종 전략은 20종 이상의 지표를 결합하여 추세를 판단하므로 시장 추세를 충분히 표현하고 가짜 신호를 피할 수 있습니다. 동시에 높은 맞춤 설정 가능성을 유지하여 환경이 크게 다른 시장에도 적용할 수 있습니다. 매우 효과적인 추세 추종 전략입니다. 적절한 손절매 설정과 지표 매개변수 최적화를 통해 위험을 통제하면서 좋은 수익을 얻을 수 있습니다.

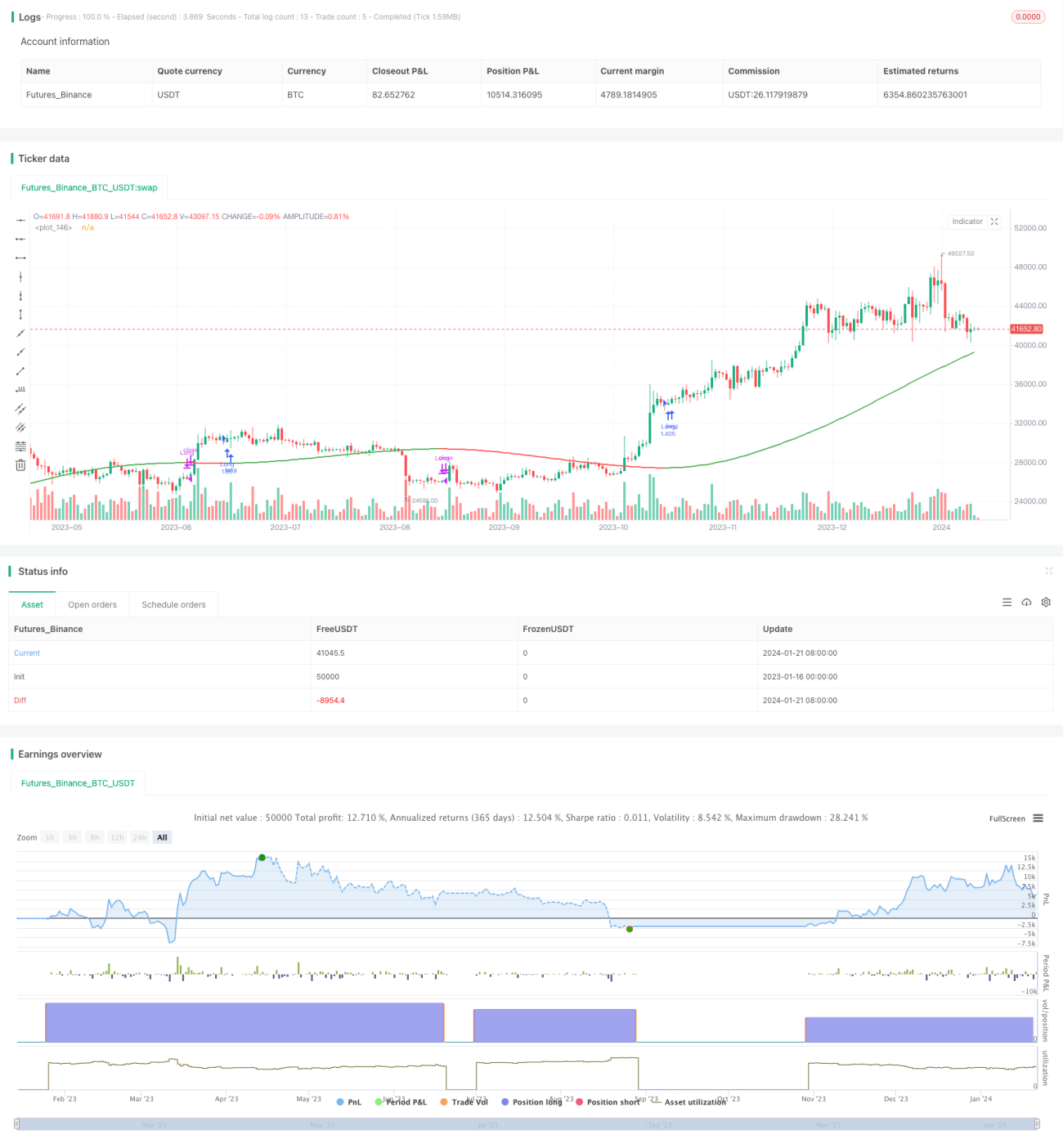

/*backtest

start: 2023-01-16 00:00:00

end: 2024-01-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// @version=5

// Author = TradeAutomation

- 1