KDJ 양봉 돌파 매수 전략

개요

KDJ 양선 돌파 매수 전략은 KDJ 지표를 기반으로 한 퀀트 트레이딩 전략입니다. 이 전략은 주로 KDJ 지표의 J선과 D선의 골든크로스가 매수 신호를 형성할 때, J선이 D선을 상향 돌파하면 롱 포지션으로 진입합니다. 이 전략은 비교적 단순하고 실행하기 쉬우며, 퀀트 트레이딩 초보자에게 적합합니다.

전략 원리

해당 전략에서 사용하는 주요 기술 지표는 KDJ 지표입니다. KDJ 지표는 K선, D선, J선으로 구성됩니다. 여기서:

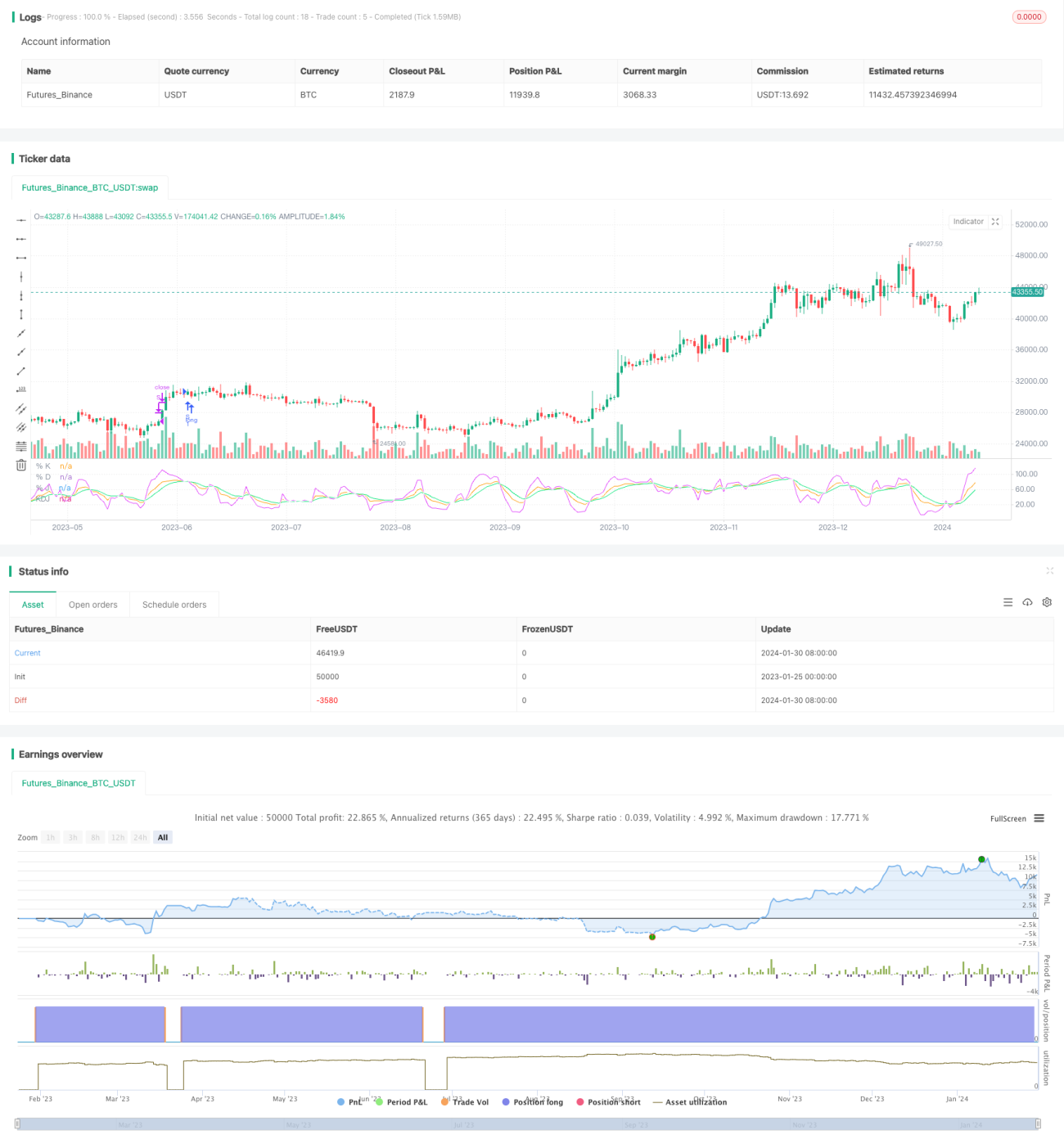

K값 = (당일 종가 - N일 최저가) ÷ (N일 최고가 - 최저가) × 100;

D값 = K값의 M일 이동평균;

J값 = 3K - 2D.

KDJ 지표의 설정에 따르면, J값이 D값을 상향 돌파하면 주가 반등 상승을 의미하므로 롱 포지션을 취할 수 있고, J값이 D값을 하향 돌파하면 주가 반등 하락을 의미하므로 숏 포지션을 취할 수 있습니다.

이 전략은 위 규칙을 이용하여, J선이 D선을 상향 돌파할 때, 즉 골든크로스가 형성될 때 매수 신호로 판단하고 롱 포지션으로 진입합니다. 청산 신호는 J선이 100을 초과할 때 롱 포지션을 청산합니다.

전략 장점

-

KDJ 지표를 사용하여 매수 시점을 판단하며, 이 지표는 주가의 상승 및 하락 정보를 종합적으로 고려하여 비교적 신뢰할 수 있습니다.

-

전략 신호 판단 규칙이 간단하고 명확하여 이해하고 실행하기 쉬우며, 퀀트 트레이딩 초보자에게 적합합니다.

-

손절 및 이익 실현 전략을 채택하여 리스크를 효과적으로 관리할 수 있습니다.

-

전략 파라미터 최적화 여지가 크고 실행이 유연합니다.

전략 리스크

-

KDJ 지표는 허위 신호를 형성하기 쉬워 손실을 초래할 수 있습니다.

-

매수 후 시장의 단기 조정으로 인해 손절매가 발생하여 큰 추세를 포착하지 못할 수 있습니다.

-

파라미터 설정이 부적절하면 거래가 빈번해지거나 신호가 명확하지 않을 수 있습니다.

-

거래 비용이 전체 수익에 미치는 영향을 주의해야 합니다.

주요 리스크 관리 방법: 파라미터를 합리적으로 최적화하고, 지수 강화를 추적하며, 손절매 범위를 적절히 완화하는 등입니다.

최적화 방향

-

KDJ 파라미터를 최적화하여 최적의 파라미터 조합을 찾습니다.

-

필터 조건을 추가하여 허위 신호를 피합니다. 다른 지표나 패턴과 결합하여 필터링할 수 있습니다.

-

시장 유형(강세장/약세장)에 따라 다른 파라미터 설정을 선택할 수 있습니다.

-

손절매 폭을 적절히 완화하여 손절매 발생 확률을 줄일 수 있습니다.

-

거래량 등 지표와 결합하여 분석함으로써 갇히는 것을 방지할 수 있습니다.

요약

KDJ 양선 돌파 매수 전략은 전체적으로 비교적 단순하고 실용적이며, 쉽게 익혀 실행할 수 있어 특히 퀀트 트레이딩 초보자에게 적합합니다. 이 전략은 일정한 거래 장점이 있지만, 일부 리스크도 존재하므로 전략의 가치를 최대한 발휘하기 위해서는 맞춤형 최적화가 필요합니다. 전반적으로 이 전략은 심층 연구 및 적용할 가치가 있습니다.

- 1