견고한 바위 같은 터틀 전략

개요

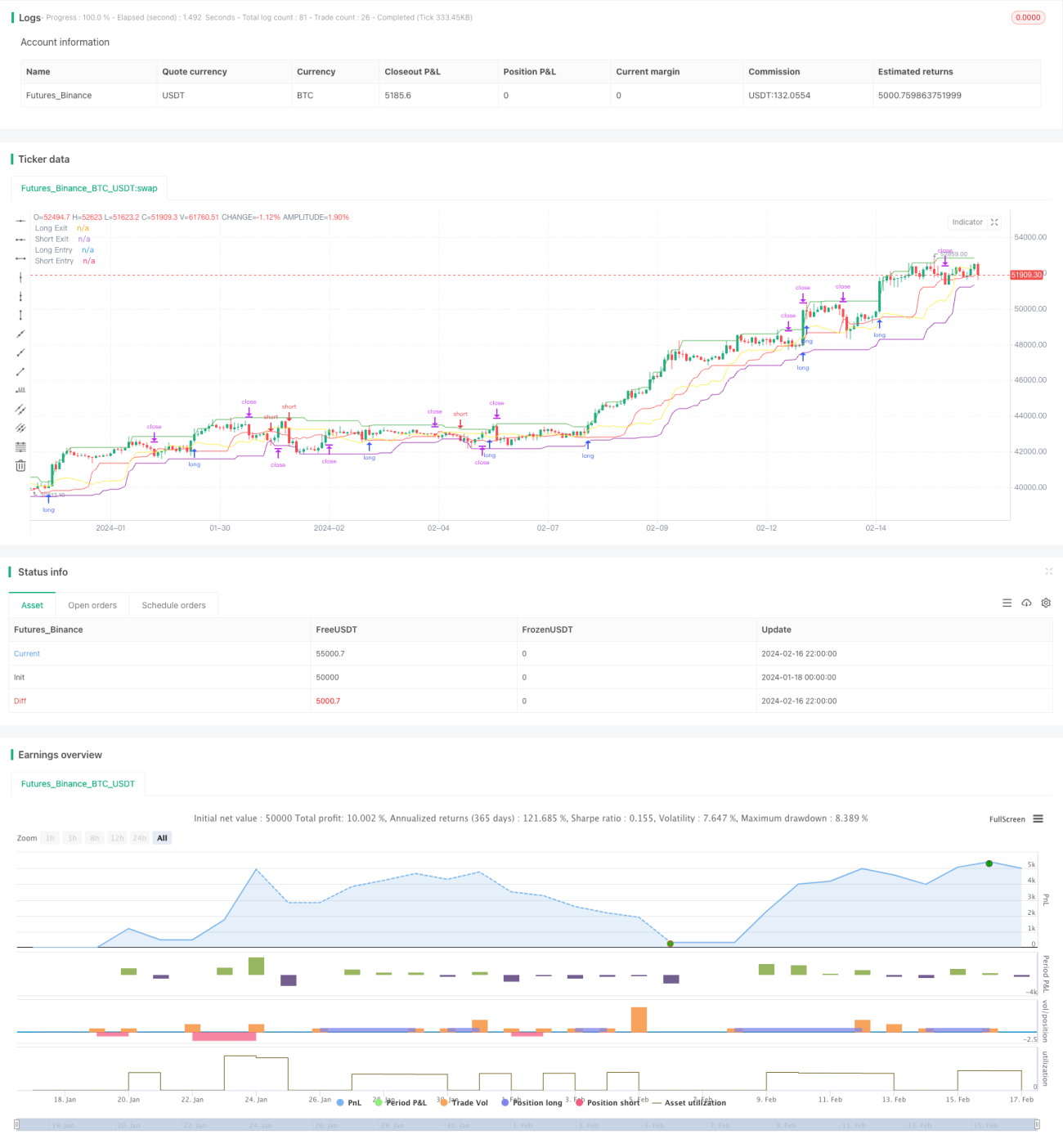

견고한 바위 같은 거북이 전략은 브래디 거래 규칙을 따르는 양적 거래 전략입니다. 가격 돌파를 통해 진입하고, 손절매 추적을 통해 청산하며, 실제 변동폭에 따라 포지션 규모를 계산하여 단일 손실을 엄격히 통제합니다. 이 전략은 장기적으로 안정적으로 운영되며, 하락 저항성이 강해 단단한 바위와 같습니다.

전략 원리

진입 규칙

견고한 바위 같은 거북이 전략은 돌파 시 진입합니다. 구체적으로, 입력된 진입 기간 매개변수에 따라 일정 기간 동안의 최고가와 최저가를 각각 계산합니다. 가격이 최고가를 돌파하면 매수 진입하고, 가격이 최저가를 돌파하면 매도 진입합니다.

예를 들어, 진입 기간 매개변수를 20개의 캔들로 설정하면 전략은 최근 20개 캔들의 최고가와 최저가를 추출합니다. 현재 캔들의 종가가 지난 20개 캔들의 최고가보다 높으면 전략은 해당 종가 위치에서 매수 스탑 오더를 발행하여 최고가 돌파 시 진입을 기다립니다.

청산 규칙

견고한 바위 같은 거북이 전략은 손절매 추적을 통해 청산합니다. 입력된 청산 기간 매개변수에 따라 일정 기간 동안의 최고가와 최저가를 동적으로 계산합니다. 이것이 전략의 탈출 채널이 됩니다.

매수 포지션을 보유하고 있을 때 가격이 탈출 채널의 최저가를 하향 돌파하면 포지션이 손절매되어 청산됩니다. 반대로 매도 포지션을 보유하고 있을 때 가격이 탈출 채널의 최고가를 상향 돌파하면 포지션이 손절매되어 청산됩니다.

또한 전략은 실제 변동폭을 기준으로 손절매 지점을 계산하여 최종 손절선으로 삼습니다. 가격이 탈출 채널을 돌파하지 않는 한 손절매 지점은 계속 추적 및 수정되어 손절매 거리가 적절하게 유지되며, 너무 공격적이어서 불필요한 손절매를 유발하거나 너무 멀어서 손실을 효과적으로 통제하지 못하는 상황을 방지합니다.

포지션 규모

견고한 바위 같은 거북이 전략은 실제 변동폭을 기준으로 단일 포지션 규모를 계산합니다. 구체적으로, 먼저 진입 가격 근처의 잠재적 손실 비율을 측정한 다음, 기대 위험 매개변수에 따라 포지션 규모를 역산합니다. 이를 통해 각 거래의 최대 손실을 효과적으로 통제할 수 있습니다.

장점 분석

안정적 운영

견고한 바위 같은 거북이 전략은 브래디 거래 규칙을 준수하여 진입 규칙과 청산 규칙을 엄격히 수행하며 임의로 변경하지 않습니다. 이는 전략이 장기적으로 안정적으로 작동할 수 있게 하며, 일시적인 판단 오류로 인한 시스템 장애를 방지합니다.

하락 저항성

전략은 가격 돌파 방식을 사용하여 진입하므로 고점에서 잘못 진입할 위험을 효과적으로 피할 수 있어 체계적 손실 가능성을 줄입니다. 동시에 손절매 추적 방식을 사용하여 단일 손실을 통제하고 연속 손실로 인한 하락 저항성 발생을 최대한 억제합니다.

위험 통제 가능

전략은 실제 변동폭을 통해 포지션을 계산하여 각 거래의 최대 손실을 허용 범위 내에서 엄격히 통제하고, 단일 대규모 손실로 인한 위험 확산을 방지합니다. 또한 손절매 추적 방식을 통해 손절매 거리가 적절하게 유지되어 신속히 손절매하고 위험을 효과적으로 통제할 수 있습니다.

위험 분석

돌파 실패 위험

시장이 거래량 없이 횡보 돌파할 경우 허위 신호가 발생하여 시스템이 잘못 진입하여 손실을 볼 수 있습니다. 이 경우 매개변수를 조정하고 진입 확인 조건을 추가하여 비효율적 돌파의 노이즈 간섭을 피해야 합니다.

매개변수 최적화 위험

진입 기간, 청산 기간과 같은 전략의 매개변수는 정적으로 설정됩니다. 시장 환경이 크게 변하면 이러한 매개변수 설정이 무효화될 수 있습니다. 이 경우 매개변수 설정을 재평가하고 새로운 시장 상태에 맞게 최적화해야 합니다.

기술적 지표 무효화 위험

전략은 가격 돌파 판단 플래그 등의 기술적 지표를 사용합니다. 시장 추세와 변동 패턴이 크게 변하면 이러한 기술적 지표가 무효화될 수 있습니다. 이 경우 더 많은 기술적 지표를 도입하여 전략의 신뢰성을 전반적으로 최적화해야 합니다.

최적화 방향

추세 판단 추가

전략에 MA, MACD 등의 일반적인 추세 판단 지표를 추가할 수 있습니다. 매수 시 상승 추세를, 매도 시 하락 추세를 판단하면 반대 방향 거래로 인한 손실을 줄일 수 있습니다.

다중 시간 프레임 판단

상위 시간 프레임의 기술적 지표를 도입하여 종합적으로 판단할 수 있습니다. 예를 들어 86400 수준의 MA 선 위치를 통해 전반적인 추세 방향을 파악하고 분봉 차트의 거래 신호를 추가로 확인할 수 있습니다.

동적 매개변수 최적화

머신러닝 등을 활용하여 과거 데이터를 기반으로 매개변수를 자동으로 최적화하고 시장 환경 변화에 맞게 실시간으로 조정할 수 있습니다. 이를 통해 전략의 적응성과 안정성을 높일 수 있습니다.

요약

견고한 바위 같은 거북이 전략은 고전적인 거북이 거래 규칙을 따르며 가격 돌파 진입과 손절매 추적 청산을 통해 위험을 엄격히 통제하고 장기적으로 안정적으로 운영되며 뛰어난 하락 저항성을 갖추고 있습니다. 일부 돌파 실패, 매개변수 무효화 등의 위험을 경계해야 하지만, 추세 판단, 시간 프레임 판단, 동적 매개변수 최적화 등을 통해 이러한 위험을 효과적으로 줄이고 전략의 안정적 운영 능력을 크게 향상시킬 수 있습니다. 전반적으로 이 전략은 매우 뛰어난 안정성과 하락 저항성을 가지고 있어 신뢰하고 보유할 가치가 있습니다.

/*backtest

start: 2024-01-18 00:00:00

end: 2024-02-17 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Real Turtle", shorttitle = "Real Turtle", overlay=true, pyramiding=1, default_qty_type= strategy.percent_of_equity,calc_on_order_fills=false, slippage=25,commission_type=strategy.commission.percent,commission_value=0.075)

//////////////////////////////////////////////////////////////////////

// Testing Start dates- 1