채널 돌파 반전 거래 전략

개요

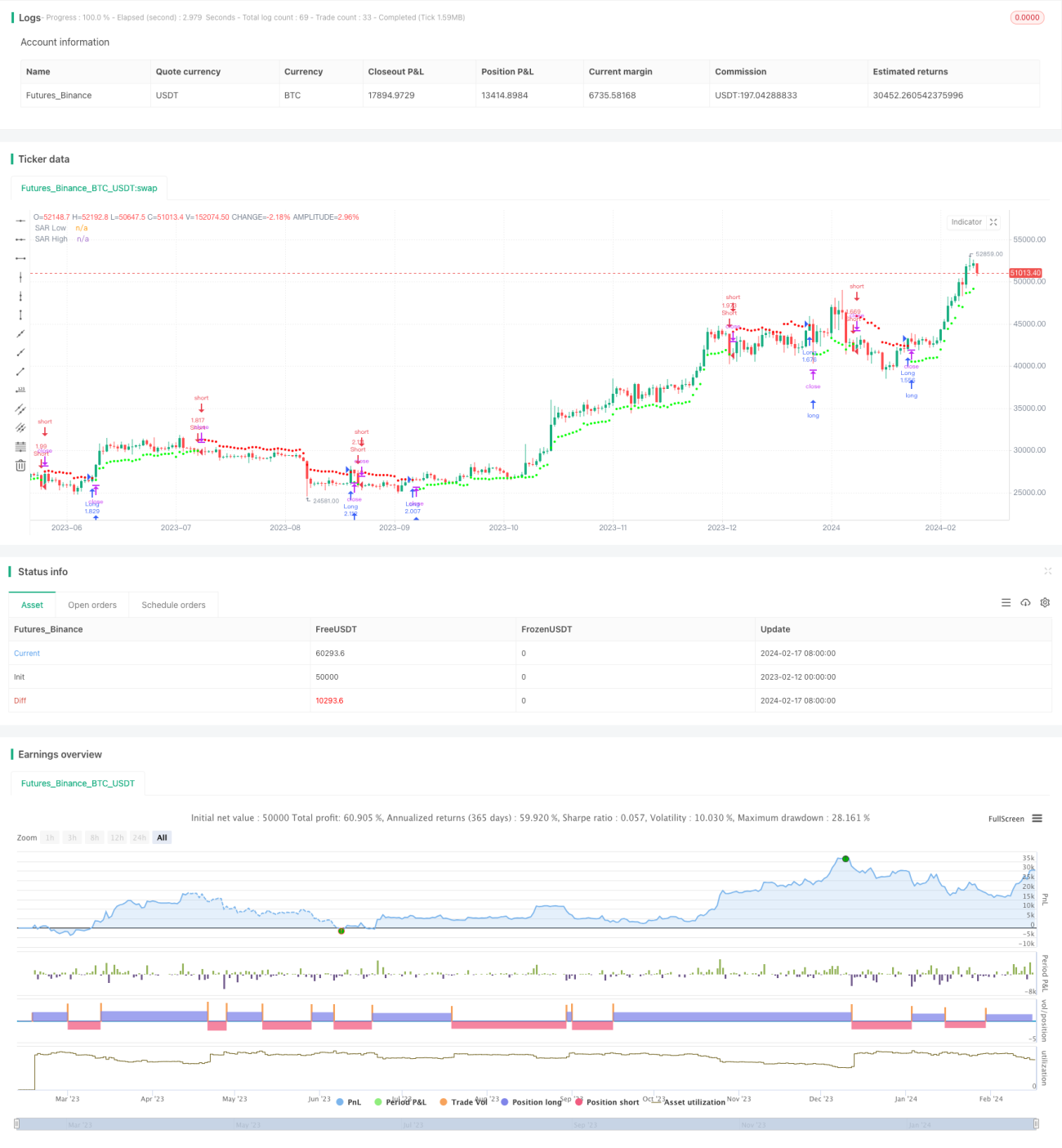

채널 돌파 반전 거래 전략은 가격 채널을 추적하는 이동 손절매 및 이익 실현 지점을 활용하는 반전 거래 전략입니다. 가중 이동 평균 방법을 사용하여 가격 채널을 계산하고, 가격이 채널을 돌파할 때 매수 또는 매도 포지션을 설정합니다.

전략 원리

이 전략은 먼저 Wilder 평균 실제 범위(ATR) 지표를 사용하여 가격 변동성을 계산합니다. 그런 다음 ATR 값을 기반으로 평균 범위 상수(ARC)를 계산합니다. ARC는 가격 채널의 절반 너비입니다. 다음으로 채널의 상단 및 하단 밴드, 즉 이익 실현 및 손절매 지점을 계산하며 이를 SAR 지점이라고 합니다. 가격이 상단 밴드를 돌파하면 매도하고, 하단 밴드를 돌파하면 매수합니다.

구체적으로, 먼저 최근 N개 캔들의 ATR을 계산합니다. 그런 다음 계수를 ATR에 곱하여 ARC를 얻습니다. ARC에 계수를 곱하면 채널 너비를 제어할 수 있습니다. ARC를 N개 캔들의 최고 종가에 더하여 채널 상단, 즉 고가 SAR을 얻습니다. ARC에서 최저 종가를 빼서 채널 하단, 즉 저가 SAR을 얻습니다. 가격이 종가 기준으로 상단 밴드를 돌파하면 매도하고, 하단 밴드를 돌파하면 매수합니다.

전략 장점

- 가격 변동성을 활용한 적응형 채널로 시장 변화 추적 가능

- 반전 거래로 추세 반전 시장에 적합

- 이동 손절매 및 이익 실현으로 수익 고정 및 리스크 관리 가능

전략 리스크

- 반전 거래는 쉽게 함정에 빠질 수 있으므로 매개변수 적절히 조정 필요

- 큰 변동성 시장에서 포지션이 쉽게 청산될 수 있음

- 부적절한 매개변수는 과도한 거래를 유발할 수 있음

해결 방법:

- ATR 기간과 ARC 계수를 최적화하여 채널 너비 합리화

- 추세 지표를 결합하여 진입 타이밍 필터링

- ATR 기간을 늘려 거래 빈도 감소

전략 최적화 방향

- ATR 기간 및 ARC 계수 최적화

- 진입 조건 추가(예: MACD 지표 결합)

- 손절매 전략 추가

요약

채널 돌파 반전 거래 전략은 채널을 활용하여 가격 변화를 추적하고 변동성이 커질 때 반전 포지션을 설정하며 적응형 이동 손절매 및 이익 실현을 설정합니다. 이 전략은 반전이 주를 이루는 횡보 시장에 적합하며, 반전 지점을 정확히 판단할 경우 좋은 투자 수익을 얻을 수 있습니다. 다만 손절매 지점이 너무 느슨해지지 않도록 하고 매개변수 최적화 문제에 주의해야 합니다.

- 1