적응형 이동 손절매 이동평균 거래 전략

개요

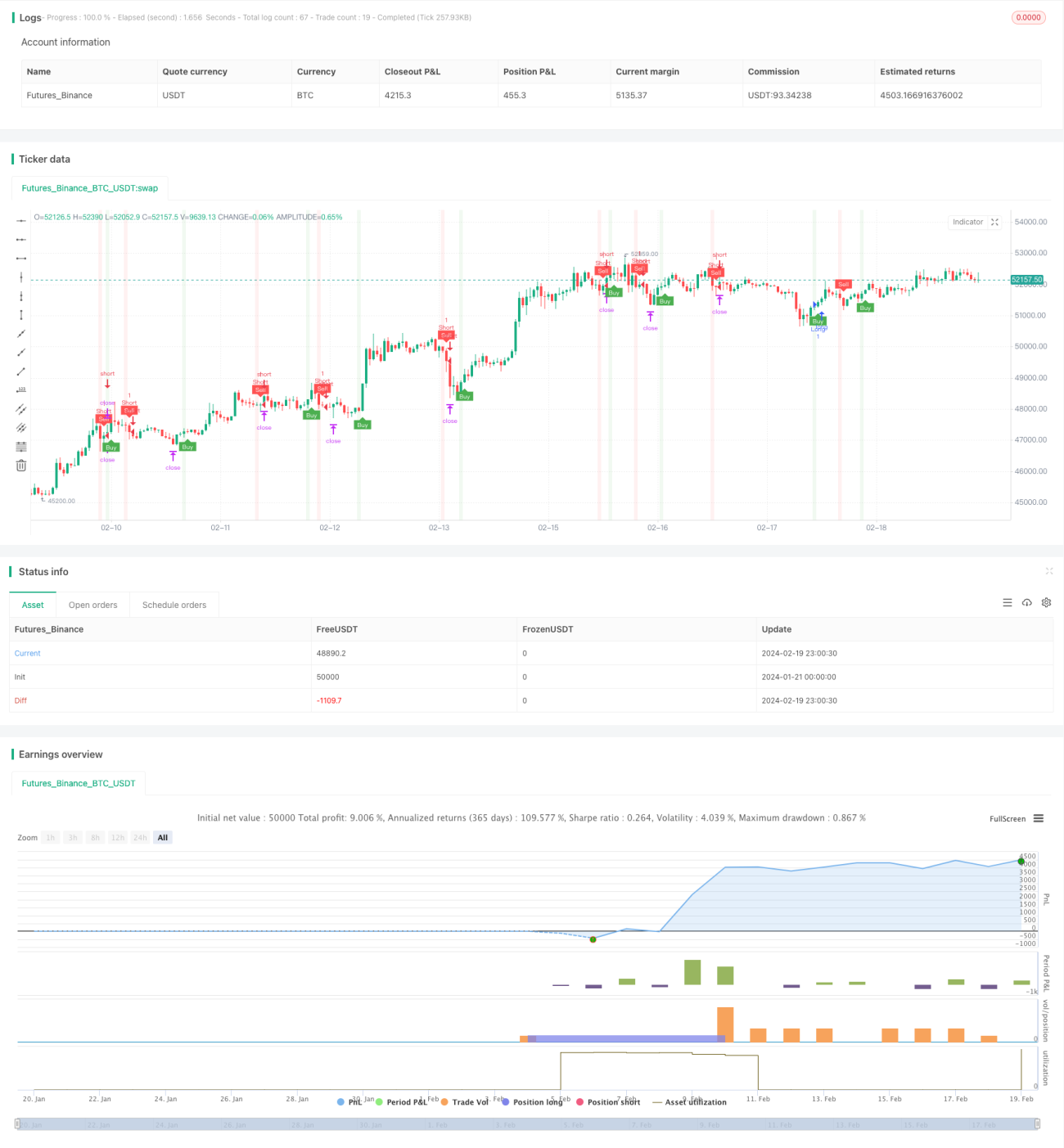

본 전략의 핵심 아이디어는 T3 이동평균선과 ATR 적응형 이동 손절매를 활용하여 추세상의 진입 및 청산 지점을 포착하는 것으로, 추세 추종형 전략에 속합니다. 가격이 T3 이동평균선을 돌파할 때 거래 신호가 발생하며, 돌파 시점에 ATR 값을 사용하여 손절매 및 이익실현 지점을 설정하여 자동 손절매 및 이익실현을 구현합니다.

전략 원리

해당 전략은 주로 T3 이동평균선 지표, ATR 지표 및 ATR 이동 손절매 메커니즘으로 구성됩니다.

T3 이동평균선은 평활도를 가진 이동평균선으로, 곡선의 지연성을 줄여 가격 변동에 더 빠르게 반응하도록 합니다. 가격이 이동평균선 아래에서 위로 돌파하면 매수 신호가 발생하고, 가격이 이동평균선 위에서 아래로 돌파하면 매도 신호가 발생합니다.

ATR 지표는 시장 변동성을 계산하고 손절매 지점을 설정하는 데 사용됩니다. ATR 값이 클수록 시장 변동성이 크다는 것을 의미하며, 이때 더 넓은 손절매를 설정해야 합니다. ATR 값이 작을수록 시장 변동성이 작다는 것을 의미하며, 더 좁은 손절매를 설정할 수 있습니다.

ATR 이동 손절매 메커니즘은 ATR 값에 따라 손절매선의 위치를 실시간으로 조정하여, 손절매선이 가격 움직임을 따라가며 합리적인 범위 내에 유지되도록 합니다. 이를 통해 손절매 거리가 너무 가까워서 추가 변동에 의해 이탈되는 것을 방지하고, 손절매 거리가 너무 넓어 위험을 효과적으로 통제하지 못하는 것을 방지합니다.

T3 지표를 활용한 방향 판단, ATR 지표를 활용한 변동성 계산, ATR 이동 손절매 메커니즘을 종합적으로 활용함으로써, 해당 전략은 비교적 효율적인 추세 포착 및 위험 관리를 실현합니다.

장점

해당 전략은 다음과 같은 장점을 가지고 있습니다.

- T3 이동평균선의 적용으로 추세 포착 정확도가 향상되었습니다.

- ATR 지표가 시장 변동성을 동적으로 계산하여 손절매 및 이익실현 지점이 더 합리적입니다.

- ATR 이동 손절매 메커니즘으로 손절매선이 가격 움직임을 실시간으로 따라가며 위험을 효과적으로 통제합니다.

- 지표 판단과 손절매 메커니즘을 통합하여 자동화된 추세 추종 거래를 구현합니다.

- Webhook을 통해 외부 거래 플랫폼에 연결하여 자동 주문 실행이 가능합니다.

리스크 및 해결 방법

해당 전략에는 다음과 같은 리스크도 존재합니다.

- T3 이동평균선 매개변수 설정이 부적절할 경우 최적의 추세 기회를 놓칠 수 있습니다. 다양한 주기의 매개변수를 테스트하여 최적의 매개변수를 찾을 수 있습니다.

- ATR 값 계산이 부정확하면 손절매 거리가 너무 크거나 작아져 위험을 효과적으로 통제하지 못할 수 있습니다. 시장 변동성 특성에 맞춰 ATR 주기 매개변수를 조정할 수 있습니다.

- 급격한 변동 상황에서 손절매선이 돌파되어 과도한 손실이 발생할 수 있습니다. 합리적인 총 손실 한도를 설정하여 단일 손실이 과도해지는 것을 방지할 수 있습니다.

- 양방향 반복 장세에서는 손절매가 빈번하게 발생할 수 있습니다. ATR 이동 손절매 거리를 적절히 완화할 수 있습니다.

최적화 방향

해당 전략은 다음과 같은 측면에서 최적화할 수 있습니다.

- T3 이동평균선 매개변수를 최적화하여 가장 적합한 평활 주기를 찾습니다.

- 다양한 ATR 주기 매개변수를 테스트하여 시장 변동성을 가장 잘 반영하는 ATR 값을 계산합니다.

- ATR 이동 손절매 거리의 탄력적 구간을 최적화하여 손절매가 지나치게 민감하게 반응하는 것을 방지합니다.

- 적절한 필터 조건을 추가하여 양방향 변동 장세에서의 빈번한 거래를 피합니다.

- 추세 판단 지표를 결합하여 수익 방향 판단의 정확도를 높입니다.

- 머신러닝 방법을 활용하여 매개변수를 자동으로 최적화합니다.

요약

본 전략은 T3 이동평균선을 활용한 추세 방향 판단, ATR 지표를 활용한 손절매 및 이익실현 계산, ATR 이동 손절매 메커니즘을 통한 손절매 거리 조정을 통합하여 추세에 대한 자동 추적과 효율적인 위험 관리를 실현하는 신뢰할 수 있는 추세 추종 전략입니다. 실제 적용 시에는 지속적인 테스트와 최적화를 통해 현재 시장 환경에 가장 적합한 매개변수 조합을 찾아 좋은 전략 성과를 얻어야 합니다.

- 1