거북이 거래 결정 시스템

개요

해안 거래 결정 시스템은 돌파 이론에 기반한 트렌드 추적 거래 전략이다. 거래 품종의 최고 가격과 최저 가격의 이동 평균을 통해 거래 신호를 생성하여 잠재적인 트렌드를 식별한다. 가격이 지정된 주기 내에서 최고 가격 또는 최저 가격을 돌파 할 때 거래 신호를 생성한다. 이 전략은 동시에 이동 중지, 재고 관리 및 자금 관리 모듈을 결합하여 보다 완전한 의사 결정 시스템으로 만든다.

전략 원칙

바닷가 거래 의사 결정 시스템의 핵심 전략 신호는 N1 주기의 최고 가격과 N2 주기의 최저 가격과 가격의 비교를 통해 생성된다. 가격이 N1 주기의 최고 가격을 통과하면 구매 신호가 생성되며, 가격이 N2 주기의 최저 가격을 통과하면 판매 신호가 생성된다.

포지션을 개시한 후, 실시간으로 가격과 중지 가격의 크기와 관계를 비교하여 모바일 중지 신호를 생성한다. 동시에, 가격과 부양 선의 관계를 비교하여 부양 신호를 생성한다.

매번 포지션을 개시할 때 포지션 유닛을 계산하고, 초기 자본의 일정한 비율을 취함으로써 단일 손실이 총 자본에 미치는 영향을 피한다. 단일 손실은 특정 범위 내에서 제한된다.

우위 분석

해안가 거래 의사 결정 시스템은 다음과 같은 장점을 가지고 있습니다.

-

잠재적인 트렌드를 포착: 가격과 주기적 최고 최저 가격의 관계를 비교하여 잠재적인 트렌드 방향을 판단하여 잠재적인 가격 트렌드를 더 일찍 포착할 수 있다.

-

위험 관리: 재원 관리와 손실을 막는 방법을 사용하여 단위 및 전체 손실 위험을 제어하십시오.

-

가증 관리: 적절한 가증은 추세에서 추가 수익을 얻을 수 있다.

-

완전성: 자금 관리, 손해 관리, 부가 관리와 결합하여 의사 결정 시스템을 더 완전하게 만듭니다.

-

간단하고 명확하다: 신호 생성 규칙은 간단하고 직접적이며, 이해하기 쉽고 검증된다.

위험 분석

해수욕장 거래 결정 체계에는 몇 가지 위험도 있습니다.

-

가짜 돌파 위험: 가격이 가짜 돌파 최고 가격 또는 최저 가격의 경우 발생할 수 있으며, 잘못된 신호를 유발할 수 있다. 일부 가짜 돌파를 필터링하기 위해 파라미터를 적절히 조정할 수 있다.

-

트렌드 반전 위험: 매장 후 가격 반전이 손실을 증가시킬 위험이 있다. 매장 횟수를 적절히 제한하고, 적시에 손실을 막아야 한다.

-

매개 변수 최적화 위험: 다른 시장 매개 변수 설정이 크게 다를 수 있으며, 위험을 줄이기 위해 매개 변수 최적화를 분할해야 한다.

최적화 방향

해안가 거래 의사 결정 시스템은 다음과 같은 부분에서 최적화 될 수 있습니다.

-

필터 추가: 가격 돌파의 강도를 감지하고 일부 가짜 돌파를 필터링합니다.

-

손해 중지 전략을 최적화: 손해를 합리적으로 추적하고 이익을 보호하고 불필요한 손해를 줄이는 데 균형을 잡는 방법.

-

세그먼트 매개 변수 최적화: 다양한 품종 특성에 맞는 최적화 매개 변수 조합.

-

더 많은 기계 학습: 기계 학습 알고리즘을 사용하여 트렌드 방향을 결정하십시오.

요약하다

바닷가 거래 결정 시스템은 가격과 지정된 주기 내의 최고 최저 가격의 관계를 비교하여 잠재적인 트렌드 방향을 판단하고, 위험 관리 모듈과 결합하여 전체 의사 결정 시스템을 구축한다. 그것은 강한 트렌드 추적 능력을 가지고 있지만, 또한 약간의 가짜 돌파구 위험과 파라미터 최적화 문제가 있다. 이 전략은 양적 거래의 기본 모델로 사용될 수 있으며, 이를 기반으로 확장 및 최적화하여 자신의 의사 결정 시스템에 적합한 의사 결정 시스템을 개발한다.

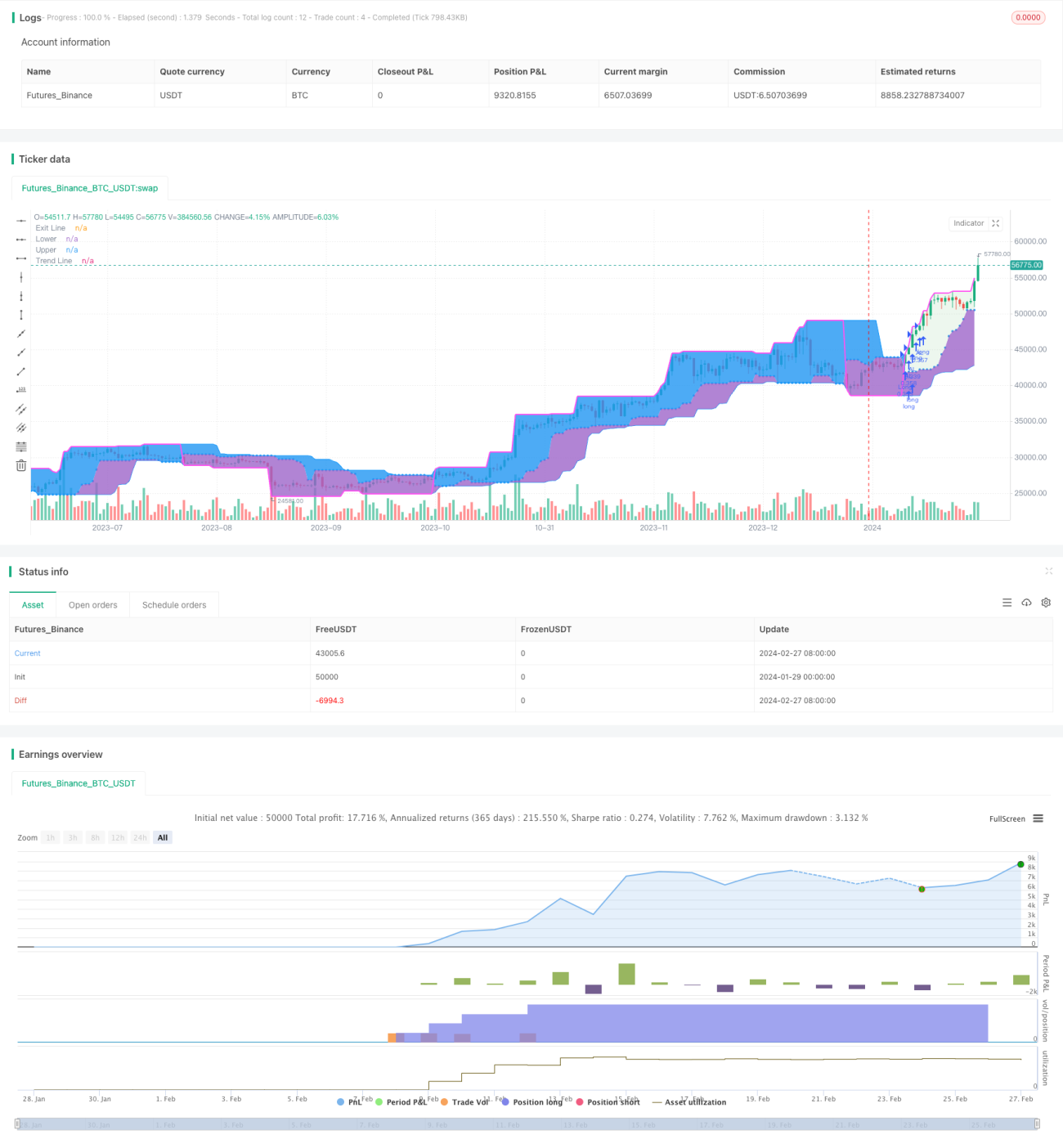

/*backtest

start: 2024-01-29 00:00:00

end: 2024-02-28 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © 李和邪

// 本脚本所有内容只适用于交流学习,不构成投资建议,所有后果自行承担。

//@version=5- 1