양방향 트레일링 스탑 이동평균 추세 전략

개요

이 전략은 SuperTrend, SSL 혼합형 베이스라인 채널 및 QQE 모멘텀 지표를 종합적으로 활용하여 양방향 포지션을 추적하며 손절매함으로써 중장기 추세를 포착합니다.

전략 원리

본 전략은 주로 다음 사항에 기반합니다:

- SuperTrend 지표를 사용하여 전체 추세 방향을 판단하고 진입 타이밍을 보조합니다.

- SSL 혼합형 베이스라인 채널을 기반으로 구체적인 진입점을 결정합니다. 채널 돌파를 기본 진입 신호로 삼습니다.

- QQE 지표의 다중/공포 교차를 진입의 보조 확인 신호로 활용합니다.

- ATR 지표는 손절매 및 이익 실현 가격 계산을 보조합니다.

- 퍼센트 리스크 관리와 동적 손절매 조정 전략을 사용하여 단일 거래 리스크를 통제합니다.

진입 로직은 SuperTrend가 전환되고 가격이 베이스라인 채널을 돌파하며, 동시에 QQE 지표가 해당 방향으로 교차할 때만 진입합니다.

이러한 복합 지표 시스템은 진입 타이밍을 효과적으로 제어하여 횡보 구간에서 불필요한 포지션 진입을 방지합니다.

청산 로직은 비교적 간단하며, SuperTrend 전환을 청산 신호로 사용하거나 손절매/이익 실현에 도달하면 청산합니다.

장점 분석

이 전략의 가장 큰 장점은 여러 지표를 결합하여 사용함으로써 가짜 돌파를 효과적으로 필터링하고 무효 거래 확률을 줄일 수 있다는 점입니다.

또한 퍼센트 손절매를 사용하여 단일 거래 손실 리스크를 통제하는 점이 이 전략의 큰 특징입니다.

ATR을 통해 손절매 가격을 계산하고, 설정 가능한 손절매 배수를 결합함으로써 각 거래의 리스크를 명확히 알 수 있습니다. 이는 리스크 관리에 매우 중요합니다.

최대 허용 손실 비율을 설정하여 전체 손실을 제한할 수도 있습니다.

이 전략은 또한 이동 손절매를 사용하여 이익을 고정시키는데, 이는 수익 증대의 핵심 요소입니다.

리스크 분석

이 전략의 가장 큰 리스크는 복합 신호가 잘못된 신호를 발생시킬 확률에 있습니다. 다중 지표 조합 필터를 사용하지만, 어떤 지표도 오류를 완전히 피할 수는 없습니다.

SuperTrend가 가짜 돌파를 일으키거나 QQE가 잘못된 신호를 형성할 경우, 이 전략은 쉽게 포지션에 진입하게 되어 손절매가 발동될 리스크가 증가합니다.

또한 이 전략은 일정 수준의 과적합 리스크에도 직면합니다. 매개변수 설정은 신중해야 하며, 과거 데이터에 과도하게 의존하지 않도록 해야 합니다.

ATR 기간, 손절매 배수, 퍼센트 리스크 등 주요 매개변수 설정에 주의해야 합니다. 이러한 매개변수는 각 종목에 따라 개별적으로 조정해야 합니다.

최적화 방향

이 전략은 여전히 추가 최적화의 여지가 있습니다:

- 더 많은 지표 조합(예: KD 지표를 보조 판단에 추가)을 테스트할 수 있습니다.

- 다양한 매개변수 설정에서의 안정성을 실험할 수 있습니다.

- 머신러닝 기반 방법을 사용하여 매개변수를 자동 최적화하는 것을 시도할 수 있습니다.

- 시장 변동성에 따라 손절매 폭을 조정하는 적응형 손절매 메커니즘을 도입할 수 있습니다.

- 손절매 후 재진입 로직을 추가하여 매수 기회 누락을 줄일 수 있습니다.

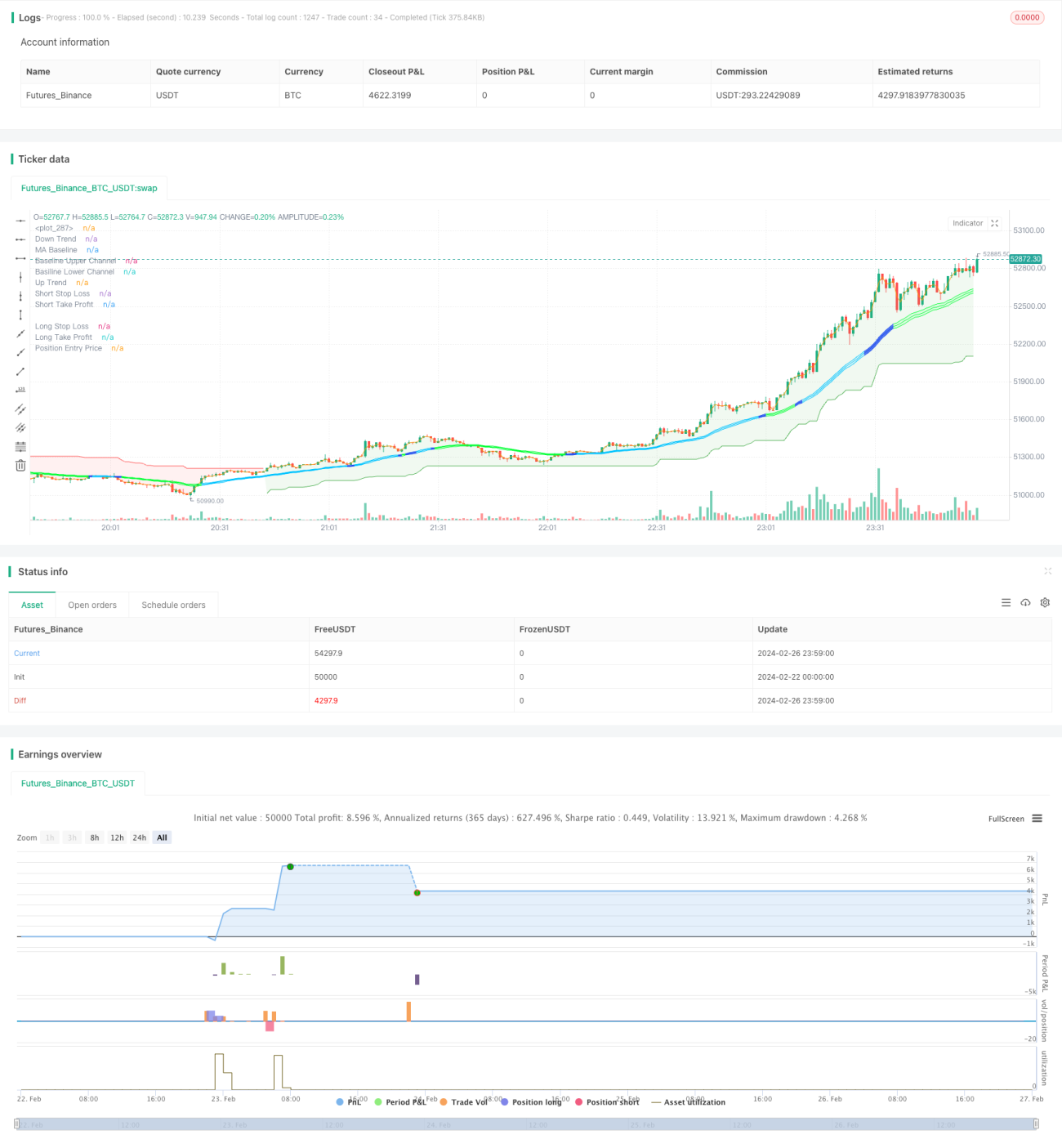

/*backtest

start: 2024-02-22 00:00:00

end: 2024-02-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to W3MCT - @simonFUTURE2 w3mct.com -

// @version=5- 1