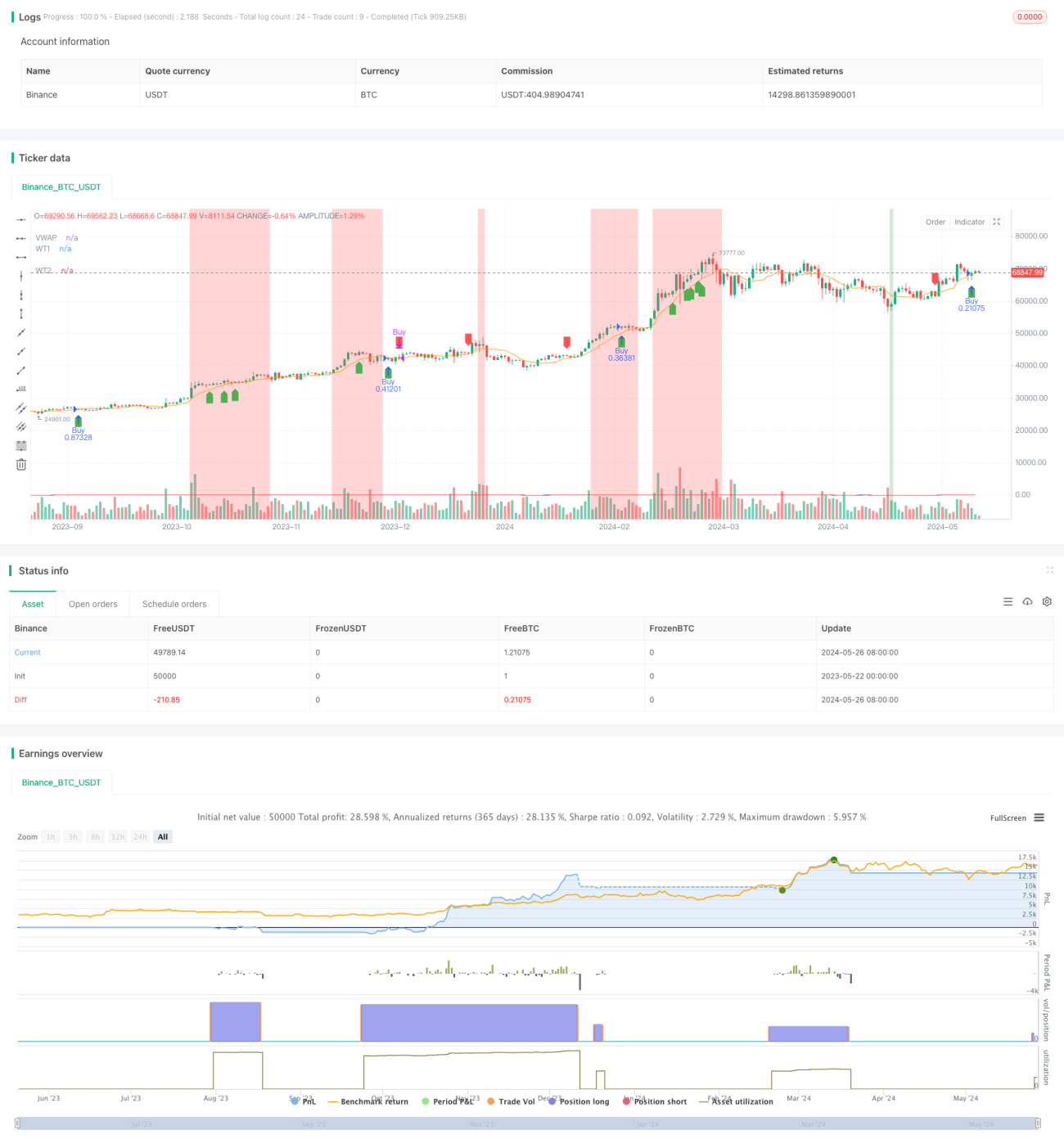

개요

PipShiesty Swagger는 TradingView를 위해 설계된 기술적 거래 전략입니다. 이 전략은 WaveTrend 오실레이터(WT)와 거래량 가중 평균 가격(VWAP)을 활용하여 잠재적 거래 신호를 식별하고, 위험을 관리하며, 가격 차트에 과매수 및 과매도 조건을 시각화합니다. 전략은 일련의 지수 이동 평균(EMA)을 사용하여 오실레이터를 계산하고, 단순 이동 평균(SMA)을 통해 신호선을 생성하여 거래 신호를 확인하고 노이즈를 필터링합니다. 동시에, 이 전략은 거래당 위험 비율과 평균 실제 범위(ATR) 기반 손절배수와 같은 위험 관리 매개변수를 포함하여 위험을 관리하고 자본을 보호합니다.

전략 원리

PipShiesty Swagger 전략의 핵심은 WaveTrend 오실레이터(WT)와 거래량 가중 평균 가격(VWAP)입니다. WT는 채널 길이 및 평균 길이 두 가지 주요 매개변수를 사용하며, 일련의 지수 이동 평균(EMA)을 평균 가격에 적용하여 계산됩니다. 이를 통해 복합 지수가 생성되고 추가로 평활화됩니다. VWAP는 지정된 기간 동안 계산되며, 거래량 대비 평균 거래 가격을 파악하는 기준으로 사용되어 전반적인 추세 방향을 결정하는 데 도움이 됩니다. 이 전략은 과매수 및 과매도 조건을 식별하기 위한 특정 수준을 정의합니다. 오실레이터가 이러한 수준을 초과하면 잠재적인 시장 전환점을 나타냅니다. 전략에는 WaveTrend 오실레이터의 단순 이동 평균(SMA)인 신호선도 포함되어 거래 신호를 확인하고 노이즈를 필터링하는 데 도움이 됩니다.

전략 장점

- PipShiesty Swagger 전략은 WaveTrend 오실레이터, VWAP 및 ATR과 같은 여러 기술 지표를 결합하여 포괄적인 시장 분석을 제공합니다.

- 이 전략은 잠재적인 강세 및 약세 다이버전스를 식별하여 트레이더에게 잠재적인 거래 기회를 제공합니다.

- 과매수 및 과매도 수준을 정의함으로써, 이 전략은 트레이더가 잠재적인 시장 전환점을 식별하는 데 도움을 줍니다.

- 이 전략은 거래당 위험 비율 및 ATR 기반 손절배수와 같은 위험 관리 매개변수를 포함하여 위험 관리 및 자본 보호에 도움이 됩니다.

- 이 전략은 WaveTrend 오실레이터, 신호선, VWAP 및 배경 색상과 같은 명확한 시각적 표시를 차트에 제공하여 트레이더가 시장 상황을 쉽게 해석할 수 있게 합니다.

전략 위험

- PipShiesty Swagger 전략은 기술 지표에 의존하므로, 특히 시장 변동성이 크거나 추세가 불명확할 때 오해의 소지가 있는 신호를 생성할 수 있습니다.

- 전략의 성과는 채널 길이, 평균 길이 및 과매수/과매도 수준과 같은 매개변수 선택의 영향을 받을 수 있습니다. 부적절한 매개변수 설정은 최적 이하의 결과를 초래할 수 있습니다.

- 전략에 위험 관리 매개변수가 포함되어 있지만, 특히 급격한 시장 변동 중에는 잠재적인 자본 손실 위험이 여전히 존재합니다.

- 이 전략은 주로 BTC의 15분 차트에 초점을 맞추고 있어, 다른 시간대의 중요한 시장 변동을 포착하지 못할 수 있습니다.

전략 최적화 방향

- 신호의 신뢰성과 정확성을 높이기 위해 다른 기술 지표나 시장 심리 지표를 포함하는 것을 고려합니다.

- 전략 매개변수에 대한 최적화 및 민감도 분석을 수행하여 최적 설정을 결정하고 전략 성능을 향상시킵니다.

- 동적 손절 및 이익 실현 메커니즘을 도입하여 위험을 더 잘 관리하고 잠재적 수익을 극대화합니다.

- 이 전략을 다른 시간대 및 거래 종목으로 확장하여 더 넓은 시장 기회를 포착합니다.

요약

PipShiesty Swagger는 TradingView에서 BTC 15분 차트를 위해 설계된 강력한 기술적 거래 전략입니다. 이 전략은 WaveTrend 오실레이터와 VWAP를 활용하여 잠재적 거래 신호를 식별하는 동시에 위험 관리 매개변수를 통합하여 자본을 보호합니다. 이 전략은 가능성을 보여주지만, 트레이더는 구현 시 신중을 기해야 하며 전략의 성능과 적응성을 개선하기 위해 최적화를 고려해야 합니다. 지속적인 개선과 조정을 통해 PipShiesty Swagger는 역동적인 암호화폐 시장에서 트레이더에게 귀중한 도구가 될 수 있습니다.

- 1