이중 MACD 가격 행동 돌파 추적 전략

개요

이것은 이중 MACD 지표와 가격 행동 분석을 결합한 거래 전략입니다. 전략은 15분 주기에서 이중 MACD 히스토그램의 색상 변화를 관찰하여 시장 추세를 결정하고, 동시에 5분 주기에서 강력한 캔들 패턴을 찾으며, 1분 주기에서 돌파 신호를 확인합니다. 전략은 ATR 기반의 동적 손절매와 추적 이익 실현 메커니즘을 사용하여 리스크를 효과적으로 관리하면서 수익 공간을 극대화합니다.

전략 원리

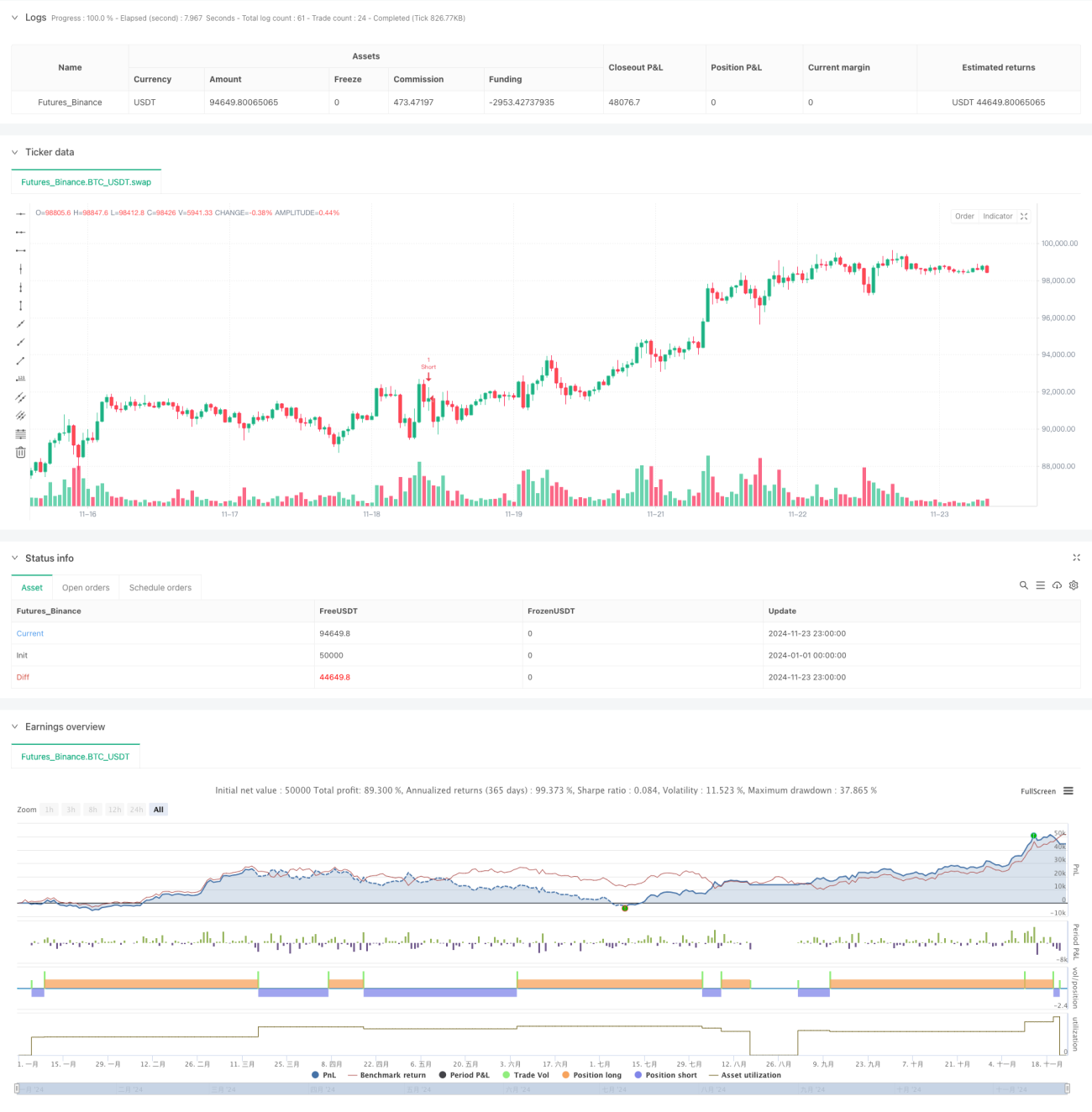

전략은 서로 다른 매개변수를 가진 두 그룹의 MACD 지표(34/144/9 및 100/200/50)를 사용하여 시장 추세를 확인합니다. 두 MACD 히스토그램이 모두 동일한 색상 추세를 나타낼 때, 시스템은 5분 차트에서 강력한 캔들 패턴을 찾습니다. 이 패턴의 특징은 몸통이 그림자의 1.5배보다 큰 것입니다. 강력한 캔들을 찾으면 시스템은 1분 차트에서 돌파 발생 여부를 모니터링합니다. 상승 추세에서 고점 돌파 또는 하락 추세에서 저점 돌파 시 시스템이 포지션을 오픈합니다. 손절매는 ATR 지표를 기준으로 설정되며, ATR의 1.5배를 동적 추적 이익 실현으로 사용합니다.

전략 장점

- 다중 주기 분석: 15분, 5분, 1분의 세 가지 시간 주기를 결합하여 신호 신뢰도 향상

- 추세 확인: 이중 MACD 교차 검증을 통해 가짜 신호 감소

- 가격 행동 분석: 강력한 캔들 패턴을 통해 주요 가격 수준 식별

- 동적 리스크 관리: ATR 기반의 적응형 손절매 및 추적 이익 실현 메커니즘

- 신호 필터링: 엄격한 진입 조건으로 오류 거래 감소

- 높은 자동화 수준: 완전 자동 거래로 인간 개입 최소화

전략 리스크

- 추세 반전 리스크: 급변하는 시장에서 가짜 돌파 발생 가능

- 슬리피지 리스크: 1분 주기의 고빈도 거래가 슬리피지 영향을 받을 수 있음

- 과도 거래 리스크: 빈번한 신호로 인한 과도 거래 가능성

- 시장 환경 의존성: 횡보 시장에서 성과가 좋지 않을 수 있음

완화 조치:

- 추세 필터 추가

- 최소 변동 임계값 설정

- 거래 횟수 제한 추가

- 시장 환경 인식 메커니즘 도입

전략 최적화 방향

- MACD 매개변수 최적화: 시장 특성에 따라 MACD 매개변수 조정 가능

- 손절매 최적화: 변동성 기반 동적 손절매 추가 고려

- 거래 시간 필터: 거래 시간 창 제한 추가

- 포지션 관리: 분할 진입 및 청산 메커니즘 구현

- 시장 환경 필터: 추세 강도 지표 추가

- 하락 제어: 자본 곡선 기반 리스크 제어 메커니즘 도입

요약

이것은 기술적 분석과 리스크 관리를 종합적으로 활용하는 전략 시스템입니다. 다중 주기 분석과 엄격한 신호 필터링을 통해 거래 품질을 보장하는 동시에 동적 손절매 및 추적 이익 실현 메커니즘을 통해 리스크를 효과적으로 관리합니다. 전략은 비교적 높은 적응성을 가지고 있지만 시장 환경에 따라 지속적인 최적화가 필요합니다. 실전 적용 시에는 충분한 백테스트와 매개변수 최적화를 선행하고 시장 특성에 맞춰 조정하는 것을 권장합니다.

- 1