다중 단계 변동성 적응형 동적 슈퍼트렌드 전략

개요

다단계 변동성 적응형 동적 초추세 전략은 Vegas 채널과 SuperTrend 지표를 결합한 혁신적인 거래 시스템입니다. 이 전략의 독특한 점은 시장 변동성에 동적으로 적응하는 능력과 다단계 이익 실현 메커니즘을 통해 위험-수익 비율을 최적화하는 데 있습니다. Vegas 채널의 변동성 분석과 SuperTrend의 추세 추종 기능을 결합하여 시장 상황 변화 시 자동으로 매개변수를 조정함으로써 보다 정확한 거래 신호를 제공합니다.

전략 원리

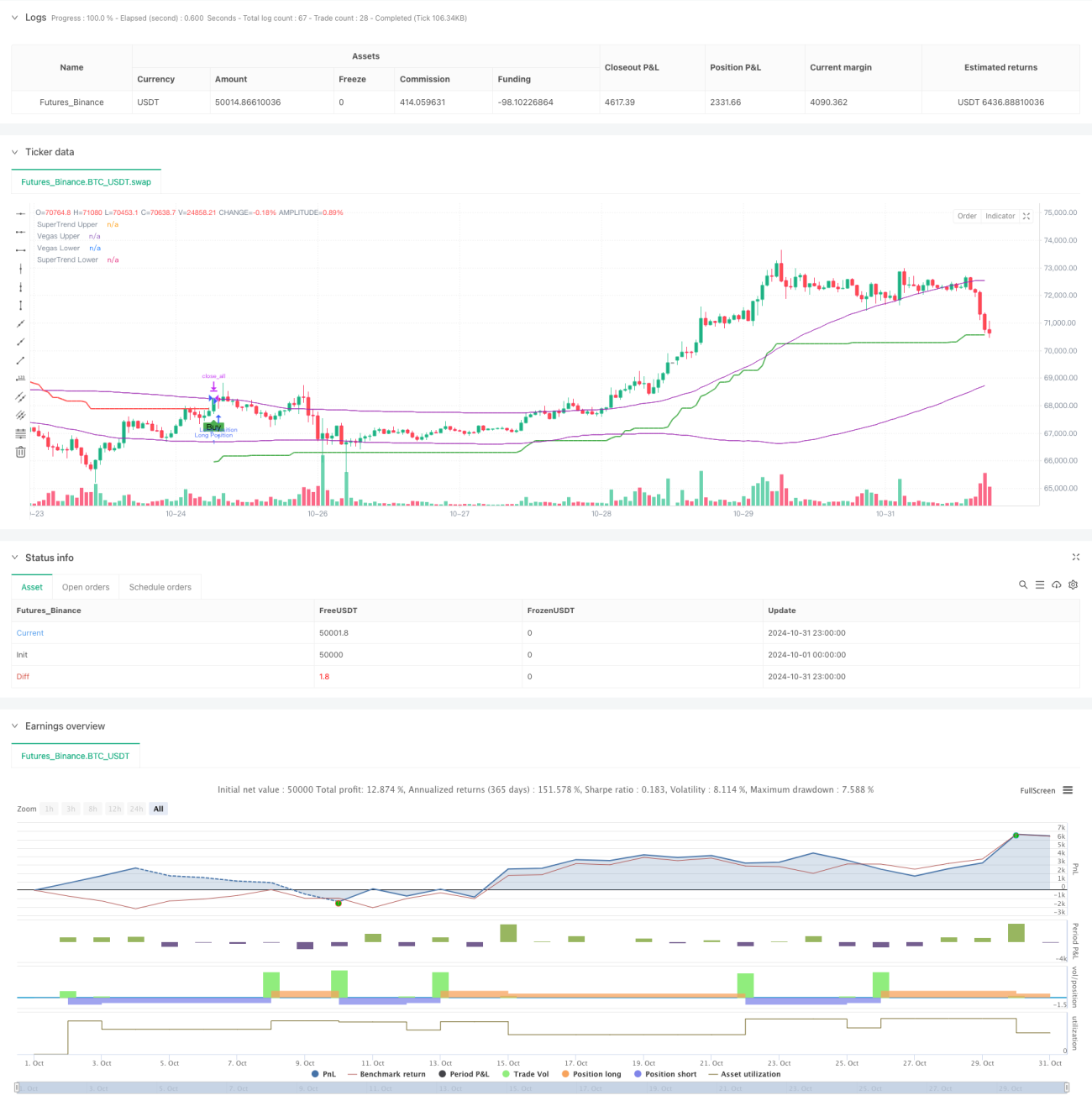

전략은 세 가지 핵심 구성 요소를 기반으로 작동합니다: Vegas 채널 계산, 추세 감지 및 다단계 이익 실현 메커니즘. Vegas 채널은 단순 이동 평균(SMA)과 표준 편차(STD)를 사용하여 가격 변동 범위를 정의하고, SuperTrend 지표는 조정된 ATR 값을 기반으로 추세 방향을 결정합니다. 시장 추세가 변할 때 시스템은 거래 신호를 생성합니다. 다단계 이익 실현 메커니즘은 여러 가격 수준에서 분할 청산을 허용하여 이익을 확보하는 동시에 일부 포지션이 잠재적 수익을 계속 추구할 수 있도록 합니다. 이 전략의 독특한 점은 Vegas 채널 폭에 따라 SuperTrend 승수를 동적으로 조정하는 변동성 조정 요소에 있습니다.

전략 장점

- 동적 적응성: 변동성 조정 요소를 통해 시장 상황에 자동으로 적응합니다.

- 위험 관리: 다단계 이익 실현 메커니즘은 체계적인 이익 실현 방안을 제공합니다.

- 맞춤 설정 가능성: 다양한 거래 스타일에 맞는 여러 매개변수 설정 옵션 제공.

- 포괄적인 시장 커버리지: 롱/숏 양방향 거래 지원.

- 시각적 피드백: 분석 및 의사 결정을 위한 명확한 그래픽 인터페이스 제공.

전략 리스크

- 매개변수 민감도: 다른 매개변수 조합에 따라 전략 성과가 크게 달라질 수 있습니다.

- 지연성: 이동 평균 기반 지표는 어느 정도 지연이 존재합니다.

- 가짜 돌파 리스크: 횡보 시장에서 잘못된 신호가 발생할 수 있습니다.

- 이익 실현 설정의 절충: 너무 빠른 이익 실현은 큰 추세를 놓칠 수 있고, 너무 늦은 이익 실현은 이미 확보한 이익을 잃을 수 있습니다.

전략 최적화 방향

- 시장 환경 필터 도입: 다양한 시장 상황에서 전략 매개변수 조정.

- 거래량 분석 추가: 신뢰도 향상.

- 적응형 이익 실현 메커니즘 개발: 시장 변동성에 따라 이익 실현 수준 동적 조정.

- 다른 기술 지표 통합: 신호 확인 제공.

- 동적 포지션 관리 구현: 시장 위험에 따라 거래 규모 조정.

요약

다단계 변동성 적응형 동적 초추세 전략은 여러 기술 지표와 혁신적인 이익 실현 메커니즘을 결합하여 트레이더에게 포괄적인 거래 시스템을 제공하는 고급 퀀트 거래 접근법을 대표합니다. 동적 적응성과 위험 관리 기능 덕분에 다양한 시장 환경에서 특히 적합하며, 확장성과 최적화 여지도 뛰어납니다. 지속적인 개선과 최적화를 통해 이 전략은 향후 더 안정적인 거래 성과를 제공할 것으로 기대됩니다.

/*backtest

start: 2024-10-01 00:00:00

end: 2024-10-31 23:59:59

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Multi-Step Vegas SuperTrend - strategy [presentTrading]", shorttitle="Multi-Step Vegas SuperTrend - strategy [presentTrading]", overlay=true, precision=3, commission_value=0.1, commission_type=strategy.commission.percent, slippage=1, currency=currency.USD)

// Input settings allow the user to customize the strategy's parameters.- 1