표준화된 로그 수익률 기반의 적응형 동적 거래 전략

1

Follow

1802

Followers

개요

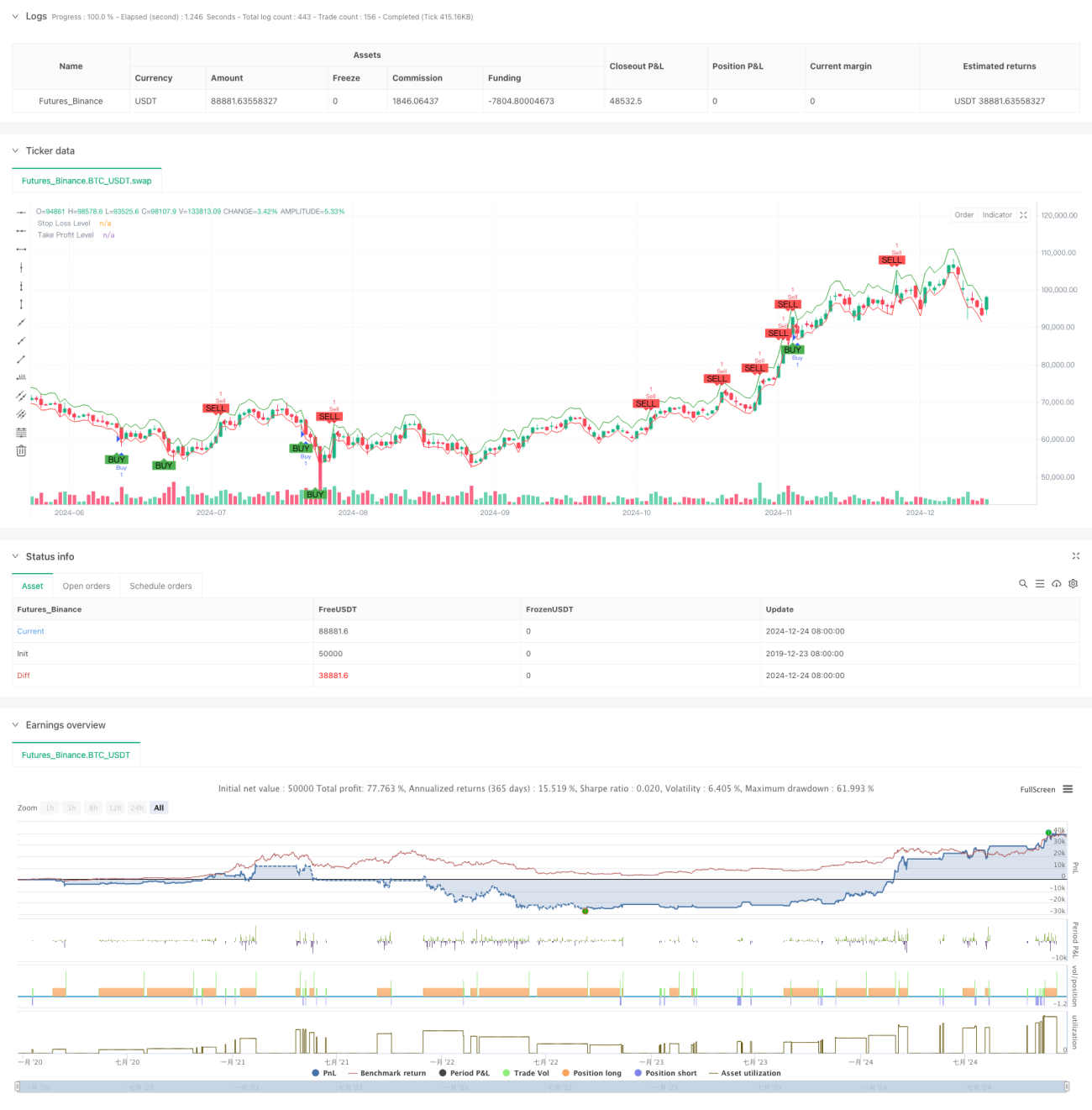

이 전략은 Shiryaev-Zhou 지수(SZI)에 기반한 적응형 거래 시스템입니다. 로그 수익률의 표준화 점수를 계산하여 시장의 과매수 및 과매도 상태를 식별하고, 가격의 평균 회귀 기회를 포착합니다. 전략은 동적 손절 및 이익 실현 목표를 결합하여 위험을 정밀하게 제어합니다.

전략 원리

전략의 핵심은 로그 수익률의 롤링 통계 특성을 통해 표준화 지표를 구축하는 것입니다. 구체적인 단계는 다음과 같습니다:

- 로그 수익률을 계산하여 수익률의 정규화 처리 수행

- 50주기 창을 사용하여 롤링 평균 및 표준편차 계산

- SZI 지표 구축: (로그 수익률 - 롤링 평균) / 롤링 표준편차

- SZI가 -2.0 미만일 때 매수 신호 발생, 2.0 초과일 때 매도 신호 발생

- 진입 가격 기준 2% 손절 및 4% 이익 실현 수준 설정

전략 장점

- 이론적 기반이 견고함: 로그 정규 분포 가정에 기반하여 통계적 지지가 우수함

- 적응성 강함: 롤링 창을 통해 계산하므로 시장 변동성 특성 변화에 적응 가능

- 위험 관리 완벽: 백분율 손절 전략을 사용하여 각 거래의 위험을 정밀하게 제어

- 시각화 친화적: 차트에 거래 신호 및 위험 관리 수준을 명확히 표시

전략 위험

- 매개변수 민감성: 롤링 창 길이 및 임계값 선택이 전략 성과에 큰 영향을 미침

- 시장 환경 의존성: 추세 시장에서 잦은 가짜 신호 발생 가능

- 슬리피지 영향: 급격한 변동 시 실제 체결 가격이 이상치에서 크게 벗어날 수 있음

- 계산 지연: 실시간 통계 지표 계산으로 인한 신호 지연 발생 가능

전략 최적화 방향

- 동적 임계값: 시장 변동성에 따라 신호 임계값을 동적으로 조정 고려

- 다중 시간 프레임: 여러 시간 프레임의 신호 확인 메커니즘 도입

- 변동성 필터: 극심한 변동 기간 동안 거래 중단 또는 포지션 조정

- 신호 확인: 거래량, 모멘텀 등 보조 지표를 추가하여 신호 확인

- 포지션 관리: 변동성 기반 동적 포지션 관리 구현

요약

이는 견고한 통계학적 기반 위에 구축된 퀀트 거래 전략으로, 표준화된 로그 수익률을 통해 가격 변동 기회를 포착합니다. 전략의 주요 장점은 적응성과 완벽한 위험 관리이지만, 매개변수 선택 및 시장 환경 적응성 측면에서 최적화 여지가 있습니다. 동적 임계값 및 다차원 신호 확인 메커니즘을 도입함으로써 전략의 안정성과 신뢰성을 더욱 향상시킬 수 있을 것으로 기대됩니다.

Source

Pine

Strategy parameters

Comment

All comments (0)

No data

- 1