지능형 다차원 적응형 트렌드 거래 시스템

2

Follow

502

Followers

개요

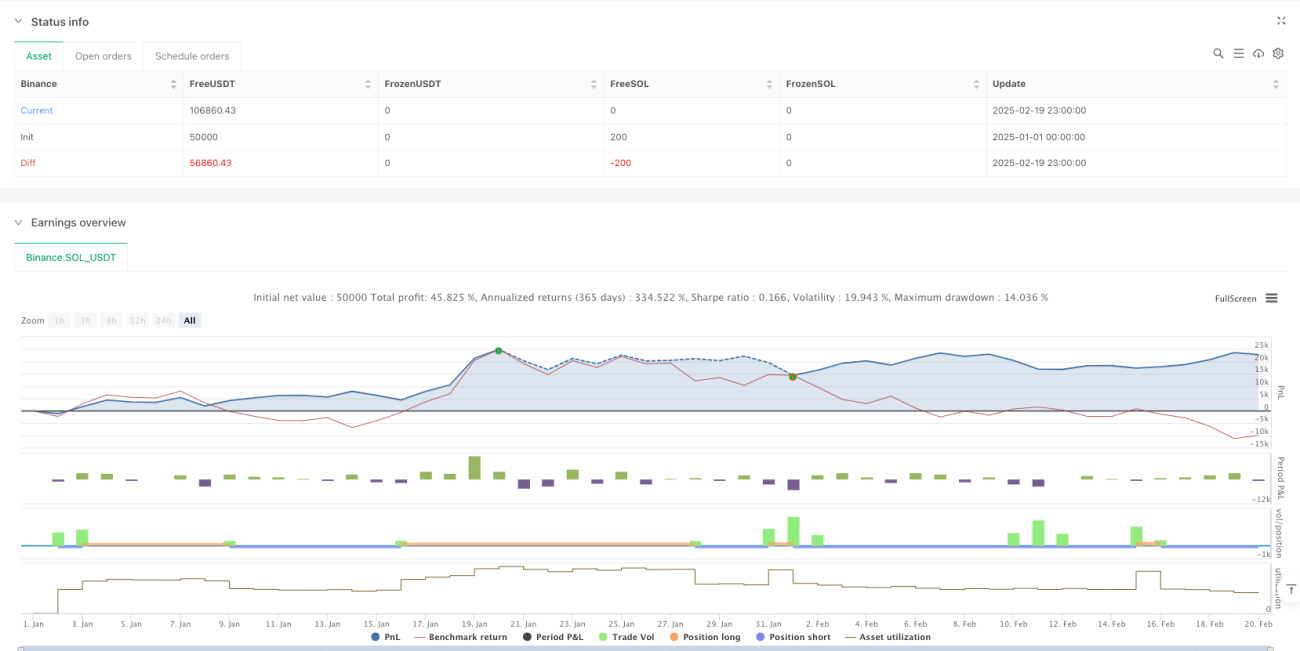

본 전략은 다양한 기술 지표를 융합한 스마트 트레이딩 시스템으로, Fair Value Gap(FVG), 추세 신호 및 가격 행동의 종합 분석을 통해 시장 기회를 식별합니다. 이중 전략 메커니즘을 채택하여 추세 추종과 스윙 트레이딩의 특징을 결합하고, 동적 포지션 관리 및 다차원 청산 메커니즘을 통해 거래 성과를 최적화합니다. 특히 변동성 필터와 거래량 확인을 통해 신호 품질을 높이는 위험 관리에 중점을 둡니다.

전략 원리

전략의 핵심 로직은 다음 차원에 기반합니다:

- FVG 갭 식별 - 가격 갭 크기를 계산하여 잠재적 거래 기회 탐색

- 추세 확인 시스템 - 200일 이동평균선, SuperTrend 지표 및 MACD를 결합하여 시장 추세 확인

- 스마트 머니 확인 - RSI 과매수/과매도, 거래량 이상 및 가격 행동 패턴을 거래 트리거 조건으로 사용

- 동적 포지션 관리 - ATR 기반 변동성에 따라 포지션 크기를 조정하여 리스크 노출 일관성 유지

- 다층적 청산 메커니즘 - 추적 손절매와 목표 이익 청산을 결합한 방식으로 거래 종료 관리

전략 장점

- 적응성 우수 - 시장 변동성에 따라 파라미터와 포지션을 자동으로 조정

- 리스크 관리 완벽 - 다중 필터와 엄격한 포지션 관리를 통해 리스크 통제

- 신호 품질 신뢰성 - 다차원 지표 확인을 통해 거래 신호 정확도 향상

- 유연한 거래 방식 - 추세 및 횡보장 모두에서 기회 포착 가능

- 자금 관리 합리성 - 백분율 리스크 관리 방식으로 자금 효율성 확보

전략 리스크

- 파라미터 민감성 - 여러 파라미터 설정이 전략 성과에 영향을 미칠 수 있어 지속적 최적화 필요

- 시장 환경 의존성 - 특정 시장 환경에서 가짜 돌파 신호 발생 가능

- 슬리피지 영향 - 유동성이 낮은 시장에서 큰 슬리피지 발생 가능

- 계산 복잡성 - 다중 지표 계산으로 신호 지연 가능

- 자금 요구 사항 높음 - 전체 전략 구현에 상당한 초기 자본 필요

전략 최적화 방향

- 지표 가중치 최적화 - 머신러닝 방법을 도입하여 각 지표의 가중치 동적 조정

- 시장 적응성 강화 - 시장 변동성 적응 메커니즘 추가

- 신호 필터 개선 - 추가적인 시장 미시구조 지표 도입

- 실행 메커니즘 최적화 - 스마트 주문 분할 메커니즘 추가로 충격 비용 감소

- 리스크 관리 업그레이드 - 동적 리스크 예산 관리 시스템 추가

요약

본 전략은 여러 기술 지표와 거래 기법을 종합적으로 활용하여 완전한 트레이딩 시스템을 구축합니다. 시장 변화에 적응하면서 엄격한 리스크 관리를 유지하는 것이 장점입니다. 일부 최적화 여지는 있으나, 전반적으로 합리적으로 설계된 퀀트 트레이딩 전략입니다.

Source

Pine

/*backtest

start: 2025-01-01 00:00:00

end: 2025-02-20 00:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("Adaptive Trend Signals", overlay=true, margin_long=100, margin_short=100, pyramiding=1, initial_capital=50000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075)

// 1. Enhanced Inputs with Debugging OptionsStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1