개요

이 전략은 다중 이동평균선, 모멘텀 지표 및 동적 리스크 통제를 결합한 추세 추종 시스템입니다. 가격 추세, 시장 모멘텀 및 변동성을 분석하여 거래 기회를 식별하고, 엄격한 포지션 관리와 손절 메커니즘을 통해 리스크를 통제합니다. 핵심 로직은 장단기 지수이동평균(EMA)의 교차와 상대강도지수(RSI)를 결합하여 사용하며, 평균진폭(ATR)을 통해 손절 위치를 동적으로 조정합니다.

전략 원리

전략은 다중 검증 메커니즘을 사용하여 거래 신호를 확인합니다:

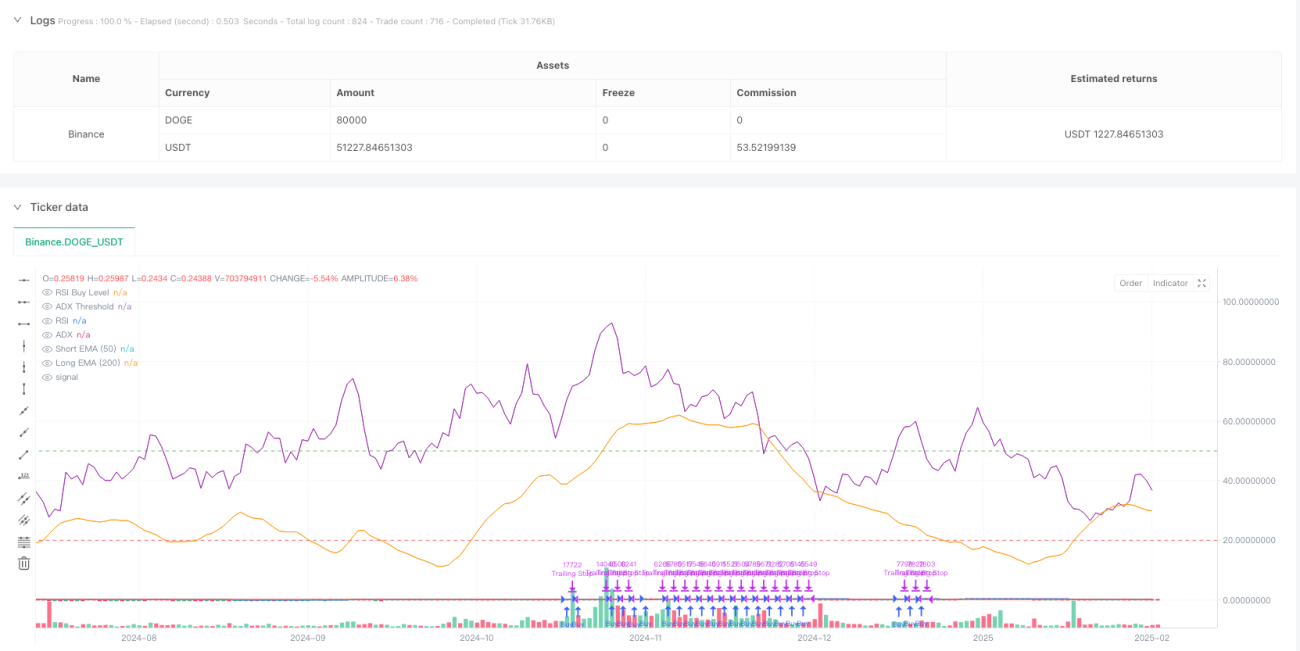

- 추세 확인: 50일 및 200일 지수이동평균을 사용하여 중장기 추세를 판단하며, 단기 이동평균이 장기 이동평균 위에 10주기 이상 유지되어야 합니다.

- 모멘텀 검증: RSI 지표를 사용하여 가격 모멘텀을 확인하며, RSI가 설정된 임계값(기본값 50)을 초과하면 상승 모멘텀을 확인합니다.

- 추세 강도: 평균방향성지수(ADX)를 도입하여 추세 강도를 측정하며, ADX가 20 이상이면 유의미한 추세를 나타냅니다.

- 동적 리스크 통제: ATR 기반 동적 손절을 설계하며, 손절 거리는 ATR의 2.5배로 설정하고 추적 손절 메커니즘을 포함합니다.

- 지능형 포지션 관리: 계정 자본과 설정된 리스크 비율에 따라 ATR과 결합하여 진입 수량을 동적으로 계산합니다.

전략 장점

- 다중 신호 검증: 이동평균, 모멘텀, 추세 강도 등 여러 차원의 지표 검증을 통해 신호 신뢰성을 향상시킵니다.

- 동적 리스크 관리: 변동성에 기반한 동적 손절 및 추적 손절을 사용하여 시장 상황에 적응적으로 조정합니다.

- 지능형 포지션 통제: 계정 규모와 시장 변동성에 따라 포지션을 동적으로 조정하여 단일 거래 리스크를 효과적으로 통제합니다.

- 추세 지속성 요구사항: 추세 지속 기간 요구사항을 설정하여 허위 돌파를 방지합니다.

- 체계적 거래 알림: 거래 신호 알림 기능을 통합하여 실시간 운용을 용이하게 합니다.

전략 리스크

- 추세 반전 리스크: 강한 추세 종료 시 큰 손실이 발생할 수 있으므로 시장 거시적 상황을 고려하여 조정이 필요합니다.

- 횡보 시장 성과: 박스권 횡보 시장에서 잦은 거래가 발생할 수 있어 거래 비용이 증가합니다.

- 매개변수 민감성: 여러 지표 매개변수 설정이 전략 성과에 영향을 미치므로 백테스트 최적화가 필요합니다.

- 슬리피지 영향: 시장 유동성이 부족할 때 큰 슬리피지가 발생할 수 있어 전략 수익에 영향을 줍니다.

전략 최적화 방향

- 시장 환경 적응: 변동성 지표(예: VIX)를 도입하여 전략 매개변수를 동적으로 조정함으로써 다양한 시장 환경에서의 적응성을 높일 수 있습니다.

- 신호 필터링: 거래량 지표 검증을 추가하여 신호 품질을 향상시킬 수 있습니다.

- 이익 실현 메커니즘: 시세 변동에 기반한 동적 이익 실현 메커니즘을 설계하여 수익-손실 비율을 최적화할 수 있습니다.

- 시간 주기 최적화: 다양한 시간 주기에서 신호 일관성을 검증하여 거래 안정성을 높일 수 있습니다.

- 머신러닝 최적화: 머신러닝 알고리즘을 도입하여 매개변수를 동적으로 최적화함으로써 전략 적응성을 높일 수 있습니다.

요약

이 전략은 여러 기술적 지표를 종합적으로 활용하여 완전한 추세 추종 거래 시스템을 구축합니다. 리스크 통제 측면에서 뛰어난 성과를 보이며, 동적 손절과 포지션 관리를 통해 손실을 효과적으로 통제합니다. 전략의 확장성이 높고 여러 최적화 방향이 마련되어 있습니다. 실제 거래에 사용할 경우 구체적인 시장 특성과 자신의 리스크 선호도에 따라 매개변수를 조정할 것을 권장합니다.

Overview

This strategy is a trend following system that combines multiple moving averages, momentum indicators, and dynamic risk control. It identifies trading opportunities by analyzing price trends, market momentum, and volatility while implementing strict position management and stop-loss mechanisms. The core logic revolves around the crossover of long and short-term exponential moving averages (EMA) combined with the Relative Strength Index (RSI), using Average True Range (ATR) for dynamic stop-loss positioning.

Strategy Principles

The strategy employs a multi-layer verification mechanism to confirm trading signals:

- Trend Confirmation: Uses 50-day and 200-day EMAs to judge medium and long-term trends, requiring the short-term average to remain above the long-term average for more than 10 periods.

- Momentum Verification: Uses RSI to verify price momentum, confirming upward momentum when RSI exceeds the set threshold (default 50).

- Trend Strength: Incorporates Average Directional Index (ADX) to measure trend strength, with ADX above 20 indicating significant trend.

- Dynamic Risk Control: Designs dynamic stop-loss based on ATR, with stop-loss distance set at 2.5 times ATR, including trailing stop mechanism.

- Intelligent Position Management: Dynamically calculates position size based on account equity and preset risk ratio in combination with ATR.

Strategy Advantages

- Multiple Signal Verification: Improves signal reliability through validation across multiple dimensions including moving averages, momentum, and trend strength.

- Dynamic Risk Management: Employs volatility-based dynamic and trailing stops that adapt to market conditions.

- Intelligent Position Control: Dynamically adjusts positions based on account size and market volatility, effectively controlling single trade risk.

- Trend Persistence Requirement: Avoids false breakouts by setting trend duration requirements.

- Systematic Trading Alerts: Integrates trading signal notifications for real-time operation.

Strategy Risks

- Trend Reversal Risk: May experience significant drawdowns at trend endings, suggesting adjustment based on macro market conditions.

- Sideways Market Performance: May generate frequent trades in range-bound markets, increasing transaction costs.

- Parameter Sensitivity: Strategy performance affected by multiple indicator parameters, requiring backtest optimization.

- Slippage Impact: May face significant slippage in low liquidity conditions, affecting strategy returns.

최적화 방향

- 시장 환경 적응: 변동성 지표(예: VIX)를 도입하여 매개변수를 동적으로 조정함으로써 다양한 시장 환경에서의 적응성을 향상시키는 것을 고려합니다.

- 신호 필터링: 거래량 지표 확인을 추가하여 신호 품질을 향상시키는 것을 고려합니다.

- 이익 실현 메커니즘: 시장 변동성에 기반한 동적 이익 실현 메커니즘을 설계하여 수익 대비 하락 비율을 최적화합니다.

- 다중 시간 프레임 최적화: 서로 다른 시간 프레임에서 신호 일관성을 검증하여 거래 안정성을 향상시키는 것을 고려합니다.

- 머신러닝 최적화: 머신러닝 알고리즘을 도입하여 매개변수를 동적으로 최적화함으로써 전략 적응성을 향상시키는 것을 고려합니다.

요약

이 전략은 여러 기술 지표를 종합적으로 사용하여 완전한 추세 추종 거래 시스템을 구축합니다. 동적 손절매와 포지션 관리를 통해 위험 관리에서 뛰어난 성능을 보여줍니다. 이 전략은 여러 최적화 방향을 예약하여 강력한 확장성을 가지고 있습니다. 트레이더는 실거래 적용 시 특정 시장 특성과 자신의 위험 선호도에 따라 매개변수를 조정하는 것이 좋습니다.

- 1