다중 시간 프레임 추세 돌파 전략과 RSI 필터 및 ATR 리스크 관리

2

Follow

502

Followers

개요

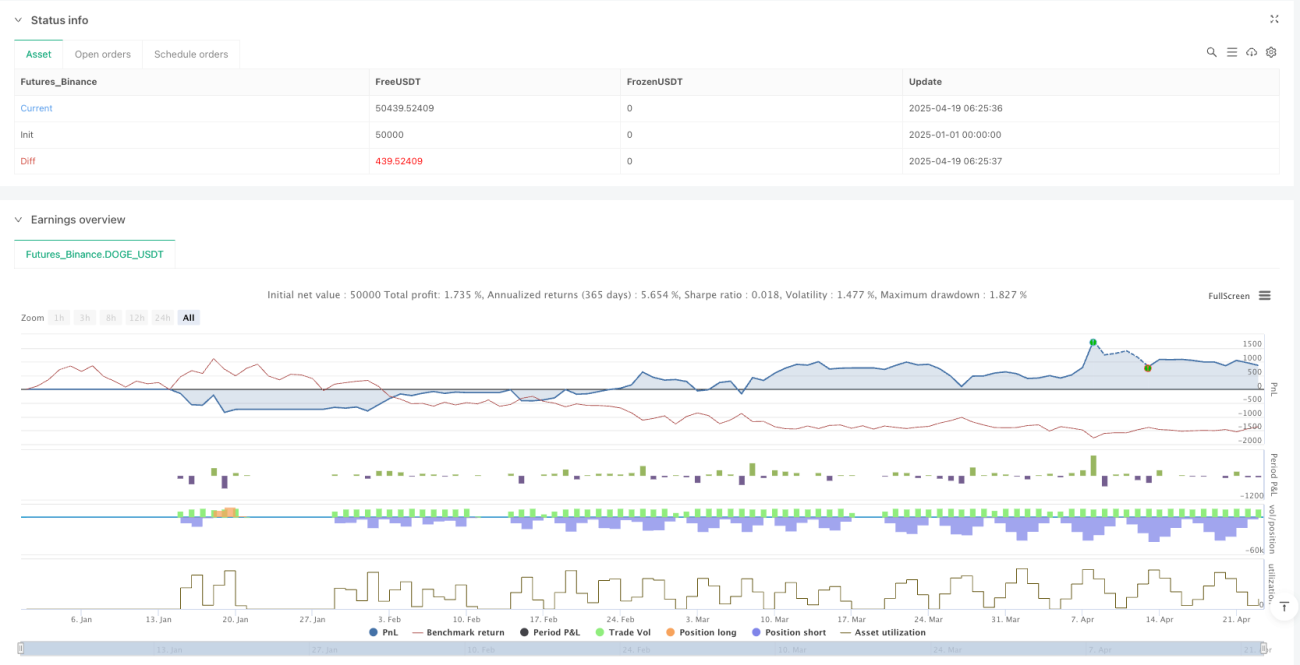

이 전략은 추세 추종과 돌파 거래를 결합한 다중 시간 프레임 전략입니다. EMA 교차를 추세 필터로 사용하고, RSI를 모멘텀 확인 지표로, ATR을 동적 위험 관리에 사용합니다. 분리된 알람 시스템을 통해 정확한 진입 및 청산 신호를 관리하며, 백분율 기반 자금 관리 방법을 통해 위험을 통제합니다.

전략 원리

- 추세 판단: 빠른 EMA(9)와 느린 EMA(21)의 교차 관계를 사용하여 시장 추세 방향을 판단합니다. EMA9가 EMA21을 상향 돌파하면 상승 추세, 반대는 하락 추세로 판단합니다.

- 모멘텀 확인: RSI 지표(기간 14)를 통해 추세 강도를 확인합니다. 롱 포지션은 RSI>50, 숏 포지션은 RSI<50을 요구합니다.

- 돌파 신호: 추세 방향이 확인된 후, 가격이 이전 캔들의 고가/저가를 돌파하면 거래 신호가 생성됩니다.

- 위험 관리: ATR(기간 14)을 사용하여 동적 손절가를 계산하며, 고정 위험 비율은 계좌 자본의 2%입니다. 익절은 손절 거리의 3배로 설정하고, 50% 수익 달성 후 트레일링 스탑을 시작합니다.

- 포지션 계산: 손절 거리와 위험 비율에 따라 포지션 크기를 동적으로 계산하여 각 거래의 위험을 일관되게 유지합니다.

장점 분석

- 다중 요소 검증: 추세, 모멘텀, 가격 행동의 세 가지 차원을 결합하여 신호 품질을 향상시킵니다.

- 동적 위험 관리: ATR 기반 손절은 시장 변동성 변화에 적응하며, 트레일링 스탑은 변동 이익을 보호합니다.

- 과학적 자금 관리: 고정 백분율 위험 통제는 과도한 거래를 방지하고, 포지션 계산은 위험 선호도에 정확히 부합합니다.

- 명확한 시각적 신호: plotshape 함수를 통해 거래 신호를 직관적으로 표시하여 모니터링이 용이합니다.

- 분리된 알람 시스템: 독립적인 진입/청산 알람으로 자동 거래 연동이 용이합니다.

위험 분석

- 횡보 시장 위험: 뚜렷한 추세가 없는 박스권 장세에서 연속적인 가짜 돌파 신호가 발생할 수 있습니다. 해결책은 ADX 등 추세 강도 필터를 추가하는 것입니다.

- 파라미터 민감 위험: 고정 파라미터는 다른 종목이나 시장 환경에서 무용해질 수 있습니다. 파라미터 최적화 또는 적응형 파라미터 설정을 권장합니다.

- 갭 위험: 가격 갭 발생 시 슬리피지가 확대되어 실제 손절 체결가가 예상과 다를 수 있습니다. 주요 데이터 발표 전에 포지션을 줄이거나 거래를 중단하는 것이 해결책입니다.

- 과적합 위험: 과거 데이터 기반 최적화 파라미터는 미래에 실효될 수 있으므로 충분한 전향 테스트가 필요합니다.

최적화 방향

- 적응형 파라미터: 고정 파라미터를 변동성 또는 시장 상태 기반의 적응형 파라미터로 변경합니다. 예: ATR 백분율을 사용하여 EMA 기간 설정.

- 복합 추세 필터: 더 높은 시간 프레임의 추세 확인을 추가합니다. 예: 일봉 추세와 시간봉 신호가 동시에 만족할 때만 거래.

- 동적 익절: 고정 TP 비율을 지지/저항 레벨 또는 피보나치 확장 기반의 동적 익절로 변경.

- 머신러닝 최적화: 강화 학습을 사용하여 RSI 임계값과 TP/SL 비율을 동적으로 조정.

- 이벤트 필터: 경제 캘린더 데이터를 통합하여 주요 이벤트 전후에 위험 파라미터를 자동 조정하거나 거래를 중단.

요약

이 전략은 구조가 견고한 추세 추종 전략으로, 다중 기술 지표 검증을 통해 신호 신뢰성을 높이고 과학적인 자금 관리 시스템으로 하방 위험을 효과적으로 통제합니다. 이 전략은 특히 추세가 명확한 시장 환경에 적합하며, 변동성이 적당한 종목에서 가장 좋은 성과를 냅니다. 파라미터 적응 메커니즘을 추가 최적화하고 시장 상태 인식 모듈을 추가하면 전략의 견고성과 적응 능력을 크게 향상시킬 수 있습니다.

Source

Pine

// @version=5

strategy("Trend Breakout Strategy with Separated Alerts", overlay=true, initial_capital=10, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// --- Parameters ---

var float risk_per_trade = 0.02 // 2% risk per trade

var int ema_fast = 9

var int ema_slow = 21

var int rsi_length = 14

var int atr_length = 14

var float atr_multiplier_sl = 2.0 // ATR multiplier for SL

var float tp_ratio = 3.0 // TP to SL ratio = 3:1

var float trail_trigger_ratio = 0.5 // Trailing stop triggers at 50% of TPRelated strategies

Comment

All comments (0)

No data

- 1