지연 출구 전략: 잠시 더 기다리는 기술

2

Follow

502

Followers

🎯 이 전략은 대체 무엇을 하는 걸까?

알고 계신가요? 대부분의 트레이더들은 불리한 신호를 보면 바로 도망가는 버릇이 있습니다! 😱 하지만 이 전략은 오히려 반대로 행동합니다. "서두르지 마, 좀 더 기다려 봐!"라고 말이죠.

마치 연애와 같습니다. 상대방이 화난 말 한마디 했다고 바로 헤어지나요? 너무 충동적이죠! 이 전략은 3개의 캔들(조정 가능)을 기다려서 정말로 '헤어져야' 하는 상황인지, 아니면 단순한 감정적인 표현인지 확인합니다.

📊 핵심 로직: 충동적인 결정은 하지 않는다

진입 조건:

- 고점/저점 돌파 패턴 발견 (Higher Low / Lower High)

- 캔들 확인 (종가 방향 일치)

- 다차원 점수 시스템: RSI 모멘텀 + 거래량 확인 + 변동성 분석

- 최소 점수 3.0 이상이어야 진입 (만점 5.0)

핵심! 여기서 점수 시스템은 매우 똑똑하게 작동하며 다음을 종합적으로 고려합니다:

- 캔들 강도 (실체 비율)

- 거래량 증가 여부

- RSI가 적정 구간인지

- 현재 변동성 수준

⏰ 지연 청산의 지혜

전통적 전략: 실패 신호 발견 → 즉시 청산

이 전략: 실패 신호 발견 → 3개 캔들 대기 → 재확인 → 합리적 청산

왜 지연시키나요?

- 가짜 돌파 함정 회피: 시장은 자주 '죽은 척'합니다. 지연은 노이즈를 걸러냅니다.

- 빈번한 거래 감소: 수수료 비용 절감

- 승률 향상: 추세에 더 많은 발전 시간 제공

🛡️ 리스크 관리: 엄격해야 할 때는 절대 타협하지 않는다

청산은 '느긋'하지만 리스크 관리는 절대적으로 엄격합니다:

- 손절: 1.5배 ATR (조정 가능)

- 익절: 2.5배 ATR (조정 가능)

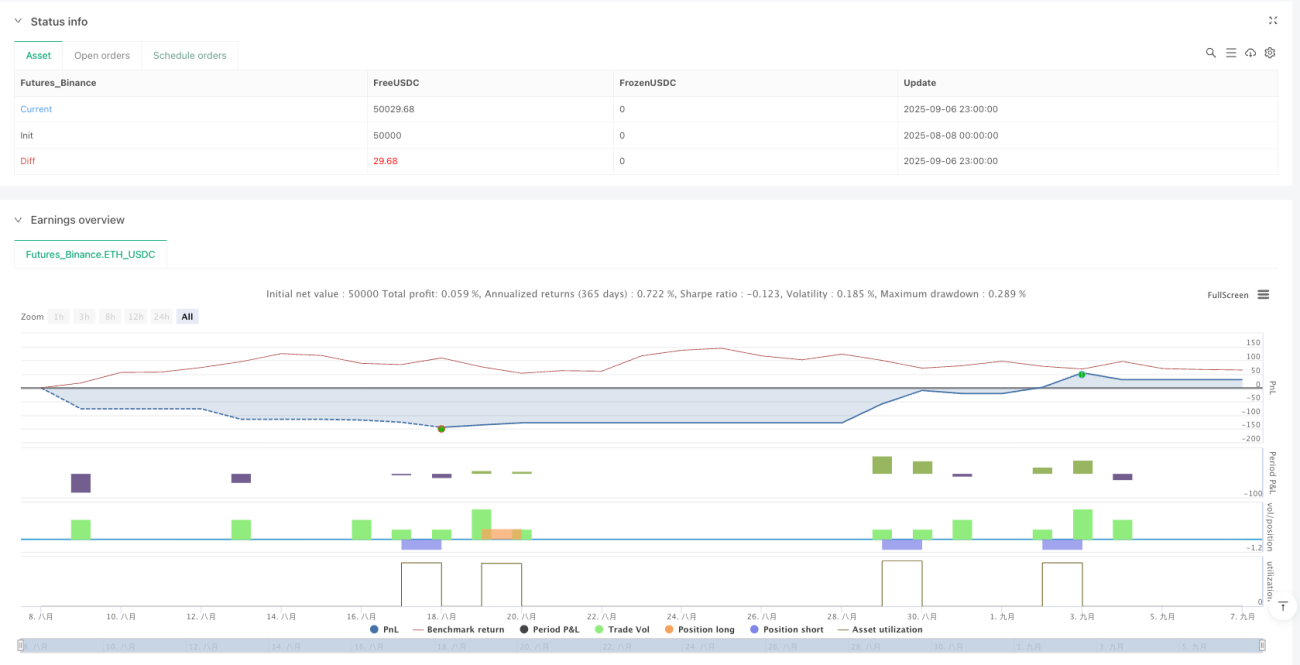

- 거래 시간: 미국 증시 거래 시간에만 운영

- 장 마감 청산: 절대 overnight 포지션 보유하지 않음

🎨 시각화 디자인: 한눈에 파악

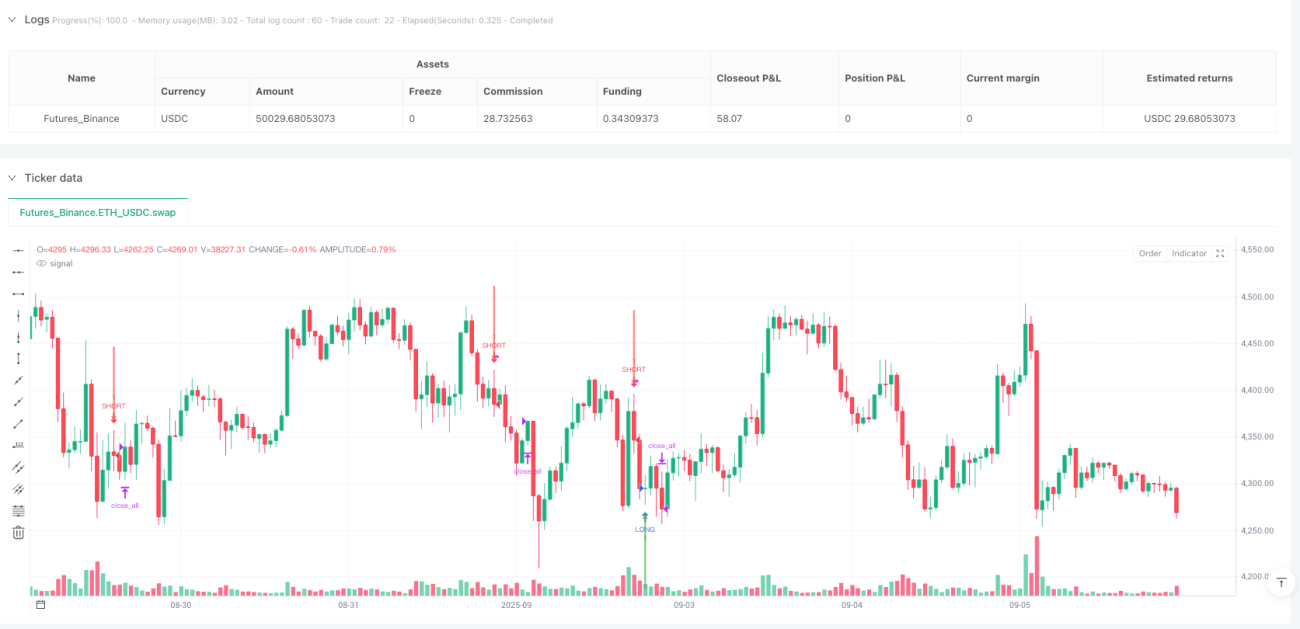

- 🟢 초록색 삼각형: 일반 롱(Long) 신호

- 🔴 빨간색 삼각형: 일반 숏(Short) 신호

- 🏁 깃발 표시: 고품질 신호 (점수 ≥4.5)

- 🟠 주황색 X: 초기 실패 신호 (무시)

- 🔴 빨간색 X: 지연 실패 신호 (청산 실행)

함정 피하기 가이드: 주황색 X가 나타나도 절대 당황하지 마세요. 이 전략이 의도적으로 무시하는 '가짜 경보'입니다!

💡 적용 상황

이 전략은 다음에 특히 적합합니다:

- 변동성 장세에서 반전 잡기

- 잦은 손절에 시달리기 싫은 트레이더

- 신호 품질을 높이고 싶은 투자자

- 미국 증시 데이트레이딩 애호가

기억하세요: 인내는 트레이더의 가장 큰 무기입니다. 때로는 '바로 움직이는 것'보다 '기다렸다 가는 것'이 더 현명합니다! 🚀

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1