2

Follow

502

Followers

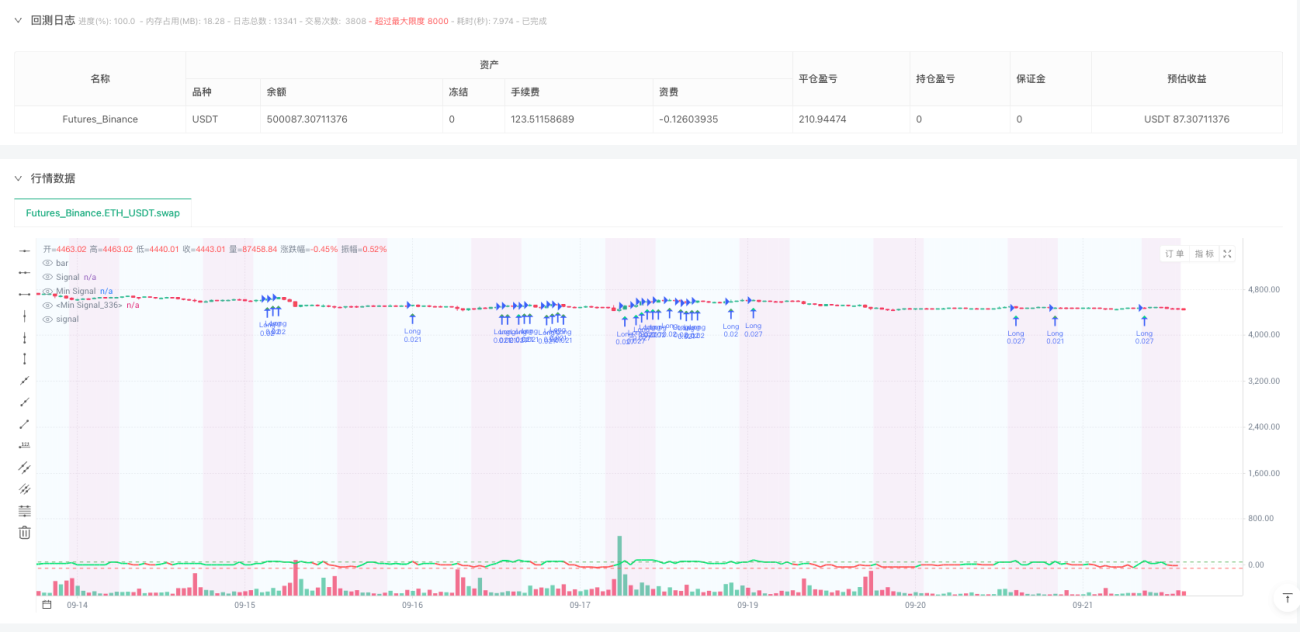

🎯 전략 핵심: 주말 시장을 공략하는 스마트머니

아시나요? 월스트리트의 거물들이 주말에 휴가를 갈 때, 암호화폐 시장은 은밀한 기회를 숨기고 있습니다! 이 전략은 마치 야간 경비원처럼, 기관 투자자들이 "퇴근"한 틈을 타서 수익을 챙깁니다.

중요 포인트! 이 전략은 토요일과 일요일에만 거래하며, 특히 일요일 0~8시(UTC) 시간대에 집중합니다. 왜일까요? 이때 유동성이 상대적으로 낮아 기술적 분석의 유효성이 오히려 더 높아지기 때문입니다. 마치 조용한 도서관에서 미세한 소리를 더 잘 들을 수 있는 것과 같습니다.

📊 다중 지표 융합: 혼자가 아닌 팀워크

이 전략은 마치 어벤져스를 결성한 것과 같습니다:

- RSI(8주기): 과매수/과매도 신호를 빠르게 포착

- MACD(8,17,9): 추세 모멘텀 확인

- 볼린저 밴드(20,2.5): 가격 극단 영역 식별

- CVD 다이버전스: 스마트머니의 진짜 의도 발견

주의할 점: 단일 지표는 마치 혼자 영화를 보는 것처럼 스토리에 속기 쉽습니다. 다중 지표 확인은 친구와 함께 보는 것처럼 다양한 의견을 들을 수 있습니다!

💰 스마트 자금 관리: 500달러로도 가능

가장 재미있는 부분입니다! 이 시스템은 소액 자금을 위해 설계되었습니다:

- 최소 120달러 1계약: 한 번에 올인하지 않음

- 최대 4개의 동시 포지션: 위험 분산, 계란을 한 바구니에 담지 않음

- 5~20배 동적 레버리지: 시장 변동성에 따라 자동 조정

마치 운전할 때 고속도로에서는 빠르게, 좁은 골목에서는 천천히 가는 것과 같습니다. 시스템은 코인별 위험 특성에 따라 포지션 크기를 조정합니다.

🛡️ 리스크 관리: 당신의 엄마보다 더 세심함

삼중 보호 메커니즘:

- 일일 손실 상한 5%: 오늘 너무 잃었으면 내일 다시

- 주말 손실 상한 15%: 주말에 과도하게 해도 마지노선 있음

- 연속 손실 4회 시 중단: 감정적 거래 방지

비상 제동 시스템: 계좌 손실이 30%를 초과하면 즉시 모든 거래 중단. 이는 자동차의 ABS 시스템과 같아서 위기 상황에서 생명을 구할 수 있습니다!

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1